Online retail sales growth slowed in May following a fairly strong April

Insight

The US stock market took another hammering overnight, with a move to safe-haven treasuries.

https://soundcloud.com/user-291029717/us-jittters-europe-soft-canada-sweden-hawkish

Too much monkey business for me to be involved in – Chuck Berry

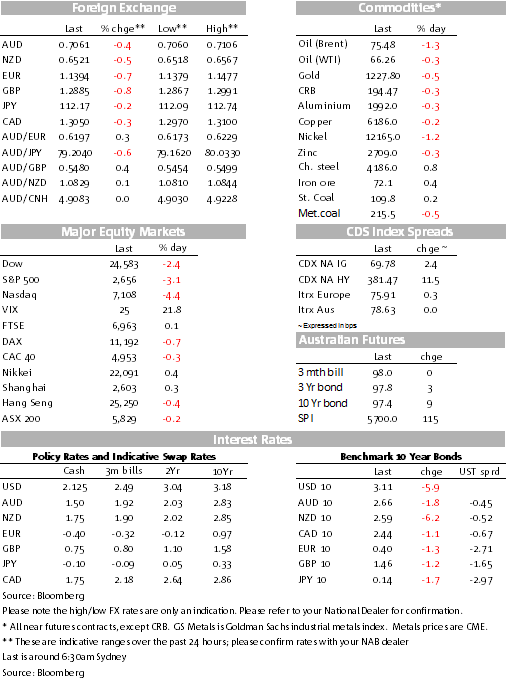

Soft economic data releases and mixed corporate earnings reports have combined to extend the losses in European and US equity markets. Safe haven demand, amid concerns over the global growth outlook and future equity earnings growth have pushed US Treasury yields lower and the big dollar is stronger against most currencies with European currencies the major under performers while CAD is the strongest G10 currency after a hawkish hike from the BoC.

Prior to last night, the FX market was mostly a bystander to the equity jitters seen in previous days. But overnight a combination of soft European PMI prints alongside additional falls in equity indices has triggered a more meaningful reaction in fx rates.

Risk aversion driven by an extension to European and US equity sell offs has boosted the USD across the board. Softer than expected European PMI prints triggered a sharp drop in the Euro and it has provided further fuel to the notion that global growth is slowing against a backdrop of rising inflationary pressures and higher borrowing rates.

Looking at USD indices, the broader Bloomberg Dollar Spot Index has made a decisive move above its previous year to date high of 1196 in mid-August and now it is toying with a break above 1200, a level not seen since mid-June last year. The narrower DXY index currently trades at 96.40, 33pips below its year to date high of 96.731.

The Euro’s sharp decline from 1.1470 to 1.1398 currently has been one big driver for the USD gains overnight. The softer than expected European PMI prints were the initial trigger for the move lower in the euro, EZ PMIs for October were weaker than expected, continuing their softening of late. Services came in at 53.3 against expectations of 54.5. Manufacturing also soft at 52.1 against expectations of 53.0. A look at the sub-indices painted a fairly bleak picture, pointing to a broadly based decline while also dismissing the notion that the slowdown could be attributed to temporary factors (impact from auto emission regulation one prominent example). The sub-indices revealed a slowdown in rates of growth across all the main measures of business performance: output, new orders and employment, so in addition to Italian budget dramas and Brexit uncertainty, Europe now also needs to absorb the prospect of a slowdown in economic growth. The next level of support for the Euro is the August low around 1.1300 and while no changes to policy guidance is expected from the ECB tonight, our sense is that at his press conference Draghi is likely to strike a caution tone emphasizing the Bank guidance is very much dependent on incoming data.

Looking at other G10 underperformers GBP is down 0.8% to 1.2887, with ongoing negative headlines on Brexit offering no support. PM May has survived another day with her speech before the backbench 1922 committee apparently well received. Meanwhile EU’s Tusk noted that there is “no guarantee hard Irish border can be avoided” and that Brexiteers were 100% responsible for the Irish-border problem. So no new news on the Brexit front.

A hawkish BoC hike has helped the CAD to outperform all G10 currencies overnight with pair briefly trading sub 1.30, before the equity rout drove a broad base bid on the USD. The Bank of Canada hiked its policy rate by 25bps for a fifth time this cycle to 1.75% and offered a hawkish outlook – dropping previously language about a “gradual approach” and indicating that rates will need to “rise to a neutral stance to achieve the inflation target”. BoC officials Poloz and Wilkins indicated the need for “flexibility” with every meeting “live” and flexibility to hike either more quickly or slowly.

AUD and NZD drifted lower during the overnight session, nevertheless both pairs remained contained within their recent ranges. AUD now trades at 0.7062 and NZD is at 0.6522. For AUD a break below the 0.7040 area could open a move sub 70c and for NZD 0.6500 looks to be the near term resistance to watch. Both currencies remain at the mercy of risk sentiment and the overnight negative lead from equities suggest the Asia open will be a big test for both antipodean currencies.

The S&P500 is down just over 3% and the big headline is that it has now erased all the gains yea to date. Disappointing earnings from AT&T and Texas Instruments drove declines in the communications and semiconductor groups, while a better than expected earnings report from Boeing was only a minor offsetting force. Earlier in the session the Stoxx Europe 600 index closed down 0.2%, its sixth consecutive daily decline.

US Treasury yields have drifted lower, in line with weaker US equities. The 10-year rate is down 4.8bps to 3.109% and the 2y10y curve is a couple of bps flatter at 26.8bps. Core European yields also declined a few bps while the Italian 10y sovereign rate climbed 1.4bps to 3.599%.

It has been a mixed night for commodities with Brent, Gold and the LMEX index down around half a percent while iron ore, steam coal and WTI oil are up between 0.20 and 0.40%.

Riksbank held rates with a continued steer towards a December or February rate hike.

EZ PMIs for October were weaker than expected, continuing their softening of late. Services came in at 53.3 against expectations of 54.5. Manufacturing also soft at 52.1 against expectations of 53.0

US new home sales fell 5.5% to 553K from a downwardly-revised 585K in August, well below the consensus, 625K. There was also a negative net revision to the previous 3 months of -55k, so whichever way you one slices it, it is not a good report. No doubt Hurricane Michael played a part, but downtrend since the start of the year reflects other factors at play, including higher borrowing rates (mortgages rates are now at a 7 year high)

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.