Coming in for landing in a heavy cross wind

Insight

Trading volumes have been lower ahead of President Trump’s State of Union address.

https://soundcloud.com/user-291029717/waiting-on-the-address-before-deciding-direction

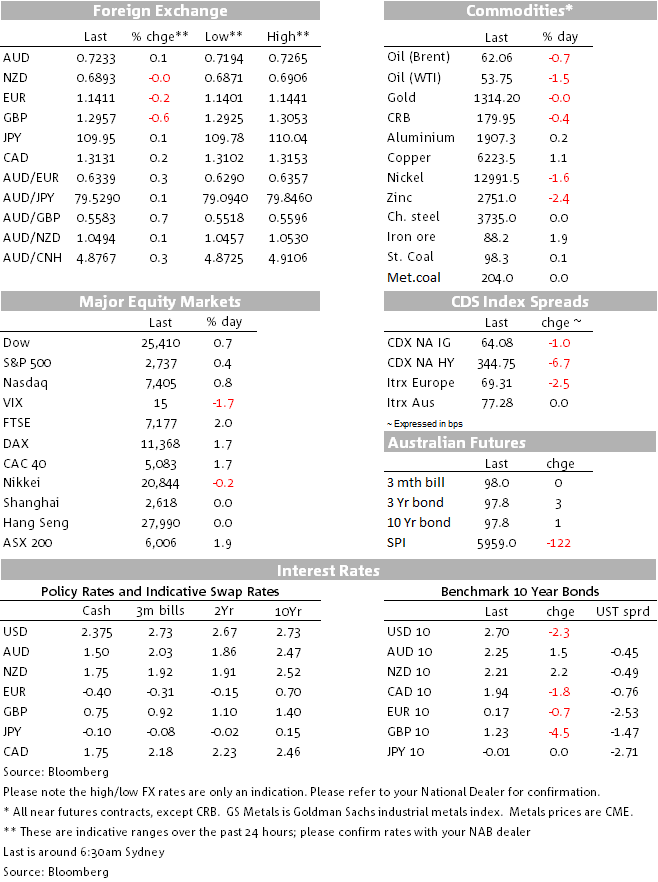

After and up and down session, US equities look set to end the day higher marking a fifth consecutive day of gains. A light trading environment however hints at market cautiousness ahead of President Trump’s state of the Union speech. Meanwhile European equities closed smartly higher boosted by solid BP earnings. The USD has retained its nascent upward trend, in spite of a broad decline in UST yields. GBP has been the big G10 underperformer following a much weaker than expected UK Services PMI and AUD has given back most of its post RBA gains. Focus now turns to RBA Lowe speech ahead President Trump state of the Union address.

US equities were unable to keep up with the solid risk positive momentum delivered by the broadly based gains recorded by major European equity indices. All major European indices closed above 1% with the UK FTSE100 leading the charge, up 2.04%. A softer pound amid disappointing UK data (more on that below) helped the FTSE, but the main driver was the 5% jump in BP shares after reporting better than expected earnings numbers aided by a rise in output. Amid a low trading environment (15%below the 30-day average according to Bloomberg) US equities have had an up, down and then up again session with sentiment not helped by a softer than expected non-manufacturing ISM. US cautiousness is also justified by uncertainty over President Trump’s state of the Union address.

The US president will address his nation at 1pm Sydney time and expectations are for the President to make comments on North Korea, the US economy, China trade talks and border security. The latter of course is the main focus for markets given that Trump has hinted at the possibility of declaring a national emergency (which would allow him to circumvent Congress) in order to fund his much desired wall along the Mexican border. The political ramifications from such an announcement (setting a precedent of governing through presidential decree) could rattle markets as it would further deteriorate an already tense relationship with a Democrat led Congress.

Against this backdrop the USD has managed to eke out some gains in index terms against both EM and Major currencies ( DXY +0.22%, BBDXY +0.12% and EMCI +0.08%).TRY (-0.46%) and ZAR (-0.34%) are the underperformers within EM while GBP (-0.62%) is the notable underperformer within G10.

The Brexit deadline is approaching, the lack of new news is making the market nervous. Meanwhile the domestic backdrop is suggesting Brexit uncertainty is starting to weigh across all sections of the economy, the services sector was the focus overnight with the UK January Services PMI printed much weaker than expected at 50.1 against 51 expected and 51.2 previous. New Business volumes declined for the first time in two and a half years in January. Markit notes “Brexit-related concerns had dampened client demand and resulted in delayed decision making on new projects. The pound now trades at 1.2954 and the break below its 200DMA suggest the recent upward momentum has run out of steam.

The decline in GBP dragged other European currencies lower with the EUR down 0.25% over the past 24hrs. The pair now trades at 1.1409, unable to sustain the small gains post better than expected EU final PMIs for January (for details see below).

AUD is the only G10 currency that has managed to keep up with the USD, but a closer look at the intraday charts shows the pair on a steady decline throughout the overnight session largely reflecting an unwind of the position driven jump in the AUD post yesterday’s RBA statement. Ahead of the announcement the market was looking for a dovish statement with the possibility of a rate cuts bias. Although the Statement could be deemed as dovish via the nod to increased downside risks globally and domestically, at this stage it sounds like the RBA is on a wait and see mode before making any decisions regarding policy guidance changes. In spite of downward revisions to GDP growth (3% instead of 3.5% for this year and next), the outlook still sees the economy growing above trend ( ~2.5%) while the unemployment rate forecast was left unchanged with unemployment expected to decline to 4.75% over the next couple of years. Moreover, inflation is still expected to head back towards target, although the Board thinks it will “to take a little bit longer than expected”.

Focus now turns to Governor Lowe speech at 12.30 Sydney time entitled “The Year Ahead”. Our economist note that on the basis of the forecasts revealed today, the Bank could keep to its mantra of “the next move in cash rates is more likely to be up”, not any time soon and presumably even further away given the trim to growth and inflation. However, the increased downside risks noted both globally and domestically will likely mean the Governor and Bank will be less confident of this statement than was the case a few months ago.

UST yields drifted lower across the board with 10y US yields currently trading at 2.7019% (-1.8bps). The move lower in yields was evident ahead of the disappointing non-manufacturing ISM. The survey for January was weaker than expected at 56.7 against expectations of 57.1 (58.0 previously). Driving the decline was a fall in New Orders (-5.0 to 57.7; which looks mostly due to a sharp fall in New Export Orders), while the government shutdown also likely weighed. Despite today’s softer print, the ISM overall remains at very solid levels with the Employment Index still pointing to +250k payrolls a month

Playing into the lower yield environment, Fed’s Kaplan repeated his recent commentary of arguing the Fed should be on hold in the first half of 2019 until the outlook becomes clearer. His cautious view is due to the global slowing, stating “It is my view that slowing economic growth outside the U.S. has the potential to ultimately spill over into economic growth in the U.S. I am particularly mindful of the fact that approximately 45 percent of S&P 500 company revenues come from outside the United States and that a variety of U.S. industries rely heavily on exports to China, Europe and other regions of the world. ”

Commodities have had a mixed to softer night with oil prices down between 0.7% and 1.5%. According to Bloomberg, Russia curbed output by 47k barrels a day in January from its October baseline level, in line with the country’s pledge to OPEC. Meanwhile, U.S. government data due Wednesday is forecast to show American crude inventories rose a third week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.