On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

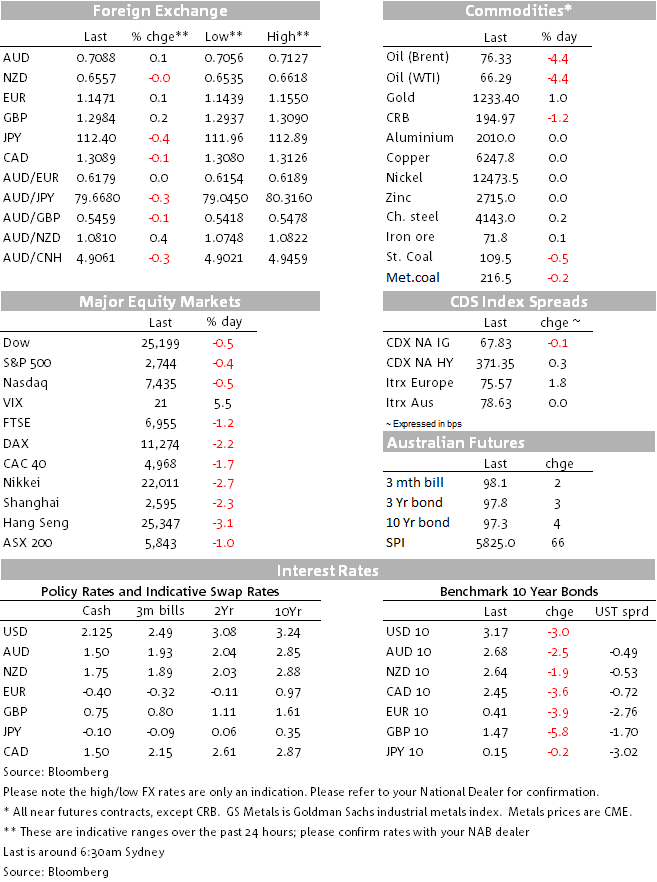

It has been another bad day at the office for equity markets, beginning in the Asian session and spreading across Europe and the US.

https://soundcloud.com/user-291029717/giving-up-on-a-good-year

“Everybody’s talking ’bout exponential growth, and the stock market crashing in their portfolios…But what do I know?” Ed Sheeran.

It has been another bad day at the office for equity markets, beginning in the Asian session and spreading across Europe and the US. There hasn’t actually been much news out there so the newswires are again making up a whole lot of stories to try to explain the move. But this feels like a risk-off move centred within equity markets because of high valuation concerns amidst a backdrop of a weaker global growth outlook. China’s open-mouth operation at the end of last week, its plan to cut personal income taxes from 2019 and offer of incremental policy changes to help support the market worked for a couple of days, but yesterday saw a 2.7% reversal in the CSI300 index. The Euro Stoxx 600 index fell by 1.6%. The S&P500 was down by 2.3% at one stage but clawed its way back up to a 0.6% fall.

The newswires are blaming some weaker earnings results as an added negative force on the market – Renault and tech companies in Europe, and bellwether stocks Caterpillar and 3M in the US. While 3M cut its earnings forecast, Caterpillar’s result wasn’t bad at all, beating analyst estimates and reaffirming guidance. The company did say that increased tariffs cost it $40m, but the full year impact will be at the lower end of previous guidance. The stock fell as much as 10% before paring its loss to 7%. We’d suggest its underperformance is more indicative of a rotation out of cyclicals into defensive stocks than its earnings result per se.

US Treasury rates have followed equity markets, tracing the move lower in S&P 500 futures during the Asian trading session and the further equity market move during US trading hours. The 10-year rate traded as low as 3.11%, and has since risen to 3.17%, still down 3bps for the day. The fall in the S&P500 from its peak late-September, now some 7%, isn’t likely large enough to impact the Fed’s monetary policy outlook, but there has been some paring of rate hikes built into the curve over the past couple of weeks. About 70bps of rate hikes are priced into the Fed Funds curve through to the end of next year, down from 78bps as of two weeks ago. The Fed’s Bostic and Kaplan spoke this morning but didn’t add much to previously held views.

In other news, the European Commission officially rejected Italy’s budget proposal, as expected, and asked the country to revise and resubmit its plans within three weeks. This is the first time such demands have been made of a member state. Ahead of that decision, Italian Prime Minister Conte said that “There isn’t any B plan” and while he suggested some tweaks were possible he could not accept any substantial change, “it will be difficult for me because I cannot accept that.” The Italian-German 10-year bond spread blew out 14bps on that, with German bunds down 4bps to 0.41% and Italian BTPs up 10bps to 3.59%.

In currency markets, movements have been well contained despite the more significant moves in equities and bonds. JPY has outperformed as one would expect, with USD/JPY falling below 112 at its nadir before recovering to 112.40, down only 0.4% for the day. All other major currency moves have been within +/-0.2% from levels of this time yesterday.

The AUD has largely traded sideways in an approximate 0.7055-0.7090 range, regaining overnight some of the small losses seen during the local trading session to currently sit at the top of that range. We expect to see the AUD remain in a bit of a holding pattern this week. NZD has followed the same path, keeping AUD/NZD hovering close to 1.08.

GBP saw a spike up to 1.3040 after Irish broadcaster RTE reported, without stating its sources, that the EU is to offer UK PM May a UK-wide customs union as a way around the Irish backstop issue, to be negotiated beyond the withdrawal agreement as a separate treaty. GBP has since nudged back below 1.30. Italy’s budget woes haven’t had much impact on EUR, with the currency flat around 1.1470.

Finally, oil prices are down over 4%, with Brent crude slipping below $76 a one point, now $76.30. Saudi Arabia’s energy minister said that OPEC and its allies are in “produce as much as you can mode”. Saudi Arabia has been pumping 9-10 million barrels per day for years and doesn’t rule out boosting that by as much as 2m.

Tonight sees the release of Markit PMI data across Europe and the US, with expectations of some broadly based slippage from September readings. Fed Presidents Mester and Bostic speak tomorrow morning, ahead of the Fed’s next Beige Book release.

Sweden’s Riksbank meets and while all and sundry expect the policy rate to be left at minus 0.5%, we’ll be on the lookout for a clearer signal on the timing of the first rate hike this cycle. December is considered “live” for this, depending on how inflation tracks through until then.

The Bank of Canada is widely expected (88% priced) to hike rates for the fifth time this cycle by 25bps, taking its overnight rate to 1.75%. The economy is running close to potential, the 5.9% jobless rate is almost back to multi-decade lows and core CPI inflation is running around target at 2%.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.