Total spending grew 0.9% in June.

The Renminbi rose today and, demonstrating its dependency, the Australian dollar followed suit.

https://soundcloud.com/user-291029717/whats-happening-with-the-yuan

Heaven, heaven is a place, a place where nothing, nothing ever happens – Talking Heads

On July 20th having clocked off for two week break AUD/USD stood at a shade over 74 cents. When I clocked back on yesterday, it was at virtually the same level. For those of us at the pointy end of foreign exchange market and who write daily missives as part of their job description this is very far from nirvana. But those who thrive on a lack of volatility in markets, it must surely feel like heaven.

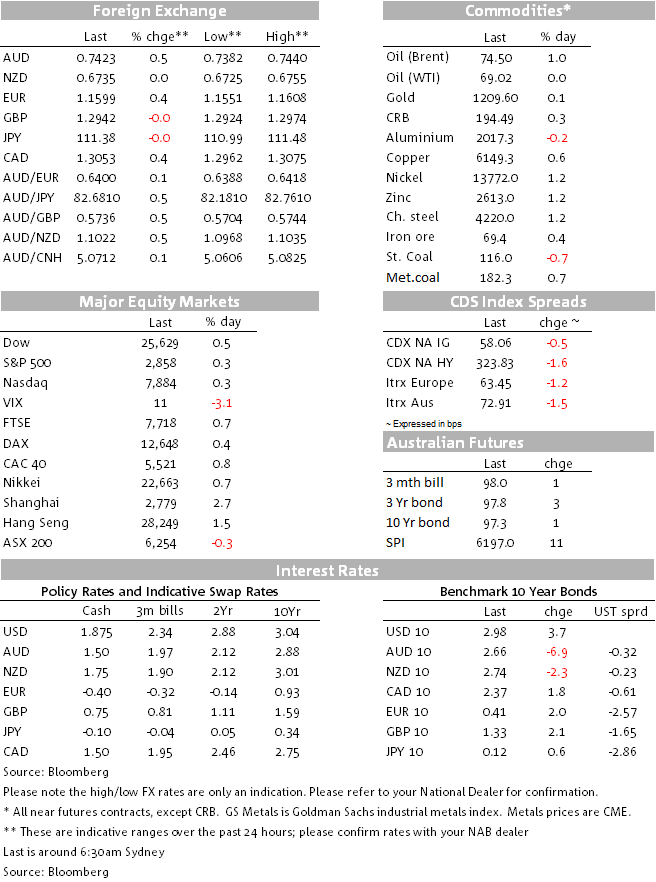

In fact, AUD is the best performing G10 currency in the past 24 hours, up around 0.5% to 0.74525. It is not a coincidence here that across the entire currency spectrum, the Chinese Yuan is the world’s best performing currency, up around 0.7%. This, not yesterday’s RBA statement, is the reason. Elsewhere US bond yields are higher seemingly on the coattails of a good day for US stocks and where an oil-price driven 0.8% rise in energy shares has led a 0.3% rise in the S&P 500 to within about 0.5% of its early January record highs. Seeing is believing, it appears, with respect to the looming threat of a sharp escalation in trade tariff wars.

The big mover in equities during out rime zone yesterday was in China with the Shanghai composite posting a 2.7% gain. Signs that the PBoC is getting concerned at the ongoing pace and extent of CNY depreciation, look to be relevant. Following Friday’s announcement of the reimposition of reserve requirements on FX forward transactions and which helped the CNH higher late Friday and the CNY yesterday, overnight Bloomberg has reported that the PBoC has met with banks to warn against ‘herd behaviour’ and also indicated it is prepared to re-introduced the so called ‘counter-cyclical factor’ into CNY determination. This was first introduced in early 2017 – but suspended at the start of 2018 – to lean against market-driven moves deemed to be too far or too fast (in either direction). The bottom line appeared to be that, for now at least, 7 Yuan to the dollar is a line not to be crossed. Though as NAB’s Christy Tan notes, if Trump decides to embark on a full scale trade tariff war in coming months, 7 is soon likely to be seen as ‘just a number’.

US equity market strength is fairly broad based but has led by energy stocks after Brent Crude added another 75 cents or 1% to $74.50, presumably on the back of the first phase of US sanctions on Iran kicking in (albeit in the oil sector these don’t start until November). Also helping has been a near 12% jump in Tesla’s shares after founder Elon Musk tweeted that he wants to take the firm private at $420 a share and said he has ‘funding secured’

The S&P has closed within about 0.5% of its early January record highs, happy, for now, to ignore the looming threat of a full-blown trade tariff war. Seeing is believing, or so it seems.

CNY the overnight leader as the PBoC’s actions and (reported) words are showing initial success in deterring short positions. Last night’s July reserve numbers, showing a $5bn rise against an expected $5bn fall, suggest that to date, the PBoC has let market forces drive the CNY lower and which also suggest that capital outflows have not been enormous (otherwise the CNY would have been weaker still). However, the WSJ notes overnight that the PBoC has been intervening the FX forward market, something which, if true, would not (yet) be showing up in FX reserves.

AUD’s gains came alongside a rally in both the Shanghai composite and a stronger CNY yesterday, proving that the Aussie remains the market’s preferred EM/China risk proxy. AUD gains were not matched by NZD and which meant AUD/USD is traded back above 1.10 for the first time since last January. We continue to regards levels near 1.10 as attractive for Australia importers to hedge future NZD payables.

Yesterday’s RBA Statement didn’t really move the dial, though AUD was a touch higher out of the announcement, perhaps in part due to the repetition of a 3%+ growth outlook but also the explicit mention of 5% unemployment rate forecast. The back end of the (May) SoMP forecasts showed 5.25%, so either this has been lowered, or the (new) end 2020 forecast to be included in Friday’s SoMP will show 5%.

Currency gains elsewhere look to be largely a product of US dollar slippage after Monday’s gains, for no obvious fundamental reason. One exception has been CAD, down 0.4% despite the aforementioned rise in (Brent) crude. The Ivey PMI index, which slipped to 61.8 from 63.1, might be of some relevance here.

A rise of 3bps in 10-year Treasury yields to 2.97% has come in conjunction with strong US stocks and hence positive risk sentiment, though perhaps aggravated by a less than stellar 3-year Note auction last night and what that might be saying about tonight’s 10-year sale.

As noted, a positive note for Brent, +1% but not WTI crude (flat) while hard commodities are mostly higher save for minor slippage in aluminium (-0.2%) and steaming coal (-0.7%). The LMEX index is up 0.5% and iron ore little changed but therefore holding it’s roughly 7.5% gain of the past week or so.

Germany June industrial production -0.9% vs. -0.5% expected

China July FX reserves +$5bn to $3,118bn vs. $3,107.0bn expected and 3,112bn in June

US June JOLTS (job openings) 6.662mn. (annual rate) vs. 6.625mn. expected and 6.659mn. previously (revised from 6.638mn)

The GDT Price Index was unchanged, as expected, from the previous mid-July auction. It arrests a four auction losing streak

RBA Governor Phil Lowe speaks on Demographic Change and Recent Monetary Policy at the Anika Foundation Luncheon, Sydney (134:05 AEST). Expect the Governor to reiterate that the next move in rates is more likely to be up than down.

China’s latest trade figures, for July, will be released sometime today (usually soon after midday AEST). In US$ terms, imports are seen having expanded by 16.1% on a year ago up from 14.1% in June and exports by 10.0% down from 11.2%.

Of particular interest in front of the pending US administration decision on whether to proceed with a fresh round of tariffs on $200bn or thereabouts of imports from China, will be the bilateral China-US balance which, recall, rose to a record China surplus of $28.9bn in June. If it falls, Trump might claim that his policies are starting to work (and that there is no reason to back off); if it rises, he will doubtless be emboldened in thinking he has to go harder.

The RBNZ’s latest policy decision will be handed down at 7:00am AEST tomorrow, which will likely reiterate the opening sentence of the June 28th OCR announcement, viz: “The Official Cash Rate (OCR) will remain at 1.75 percent for now. However, we are well positioned to manage change in either direction – up or down – as necessary”.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.