Coming in for landing in a heavy cross wind

Insight

Markets have reacted swiftly to the latest ECB meeting.

https://soundcloud.com/user-291029717/more-cheap-loans-lower-forecasts-no-rate-rises-the-ecb-is-worried

Markets become growth defensive in the wake of ECB announcements

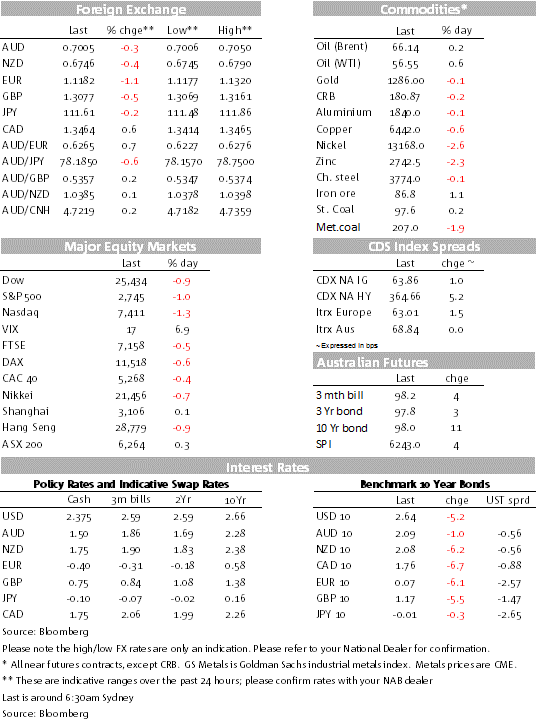

While the market was expecting something from the ECB, some combination of a possible new TLTRO (maybe that could come later), a possible change in rates forward guidance, and some revision to growth and inflation forecasts, it served up all three with gusto. The read through from markets has been a defensive one with European stocks down for the session (banks by more), as it is in the US in afternoon trade. Bond yields fell with the DXY higher and the AUD lower testing 0.70.

The German 10y bund dropped a cool 6.1bps to just 0.067%, US 10y Treasuries are 5 bps lower too, while the DXY is higher from a combination of Euro weakness, some volatility in the Pound ahead of some key parliamentary votes in the UK next week and a defensive reactionary stance in AUD and NZD trading.

ECB adjusts policy after slashing the growth outlook

While a lot of recent focus has been on the Fed and its move now to sits on their policy hands (more on that below from Lael Brainard below), overnight it’s been a refocus on the impact of the trade wars, Brexit and likely an undercurrent of concern about the domestic Eurozone economy that’s seen the ECB slash its growth outlook.

Last December, the ECB was forecasting growth of 1.9% for 2019, but it’s slashed that to just 1.1%, the same growth that was evident at the end of last year when the economy grew a meagre 0.2%/1.1%, (also confirmed last night with year to growth revised from 1.2%. The growth trajectory then doesn’t move back to its previous forecast until 2021 at 1.5% after a now expected 1.6% for 2020.

Inflation is now expected to be just 1.2% this year (down from 1.6%), the forecast for next year and the year after cut 0.2% points to 1.5% and 1.6% respectively. And so that’s still not back to the around 2% target of the central bank. Not surprising then that the ECB sees downside rise to the outlook and not a balanced outlook even though in his presser, ECB President Draghi thought that there was a good chance the trade wars and Brexit growth bugbears would be settled. Are they then worried also about the internals of the Eurozone economy? It’s also something for the RBA to ponder.

Draghi admitted that policy options for the ECB were limited and that some economic forces (external factors such as trade protectionism and Brexit) were outside of its control.

The extent of the forecast revisions had the market even more worried about the state of the economy, consensus forecasts currently pegged at 1.4% for 2019, also NAB’s forecast.

The policy response to this grimmer outlook came in two parts. First, the ECB announced a new two year bank funding package (Term Long Term Refinancing Operations, this one TLTRO3) to start on September 2019. Second, the forward guidance on when the ECB might begin on the path from negative interest rates was changed from the “after the summer of this year” to “at least until 2020”. The fresh batch of cheap long-term (2-year) loans for banks to be launched in September will overlay the previous batch of long-term loans that mature in June 2020, that from June this year will have less than 1-year to mature. By promising a new batch of loans, the ECB wards off what would have been a tightening in liquidity conditions later in the year.

There is going to have to be a swift and compelling turnaround in Eurozone activity in the second half of this year before the ECB will even consider beginning on that higher rates path. Some ECB members wanted to push out the forward guidance further (March); others worried about the longer term effects of negative interest rates.

Market reaction saw some rally in European stocks to the main headlines from the ECB, but then did an about turn after Draghi’s press conference. The Eurostoxx 600 index has closed down 0.4% and the E600 Bank index by a larger 1.88%.

Euro takes a cold bath; risk markets too

For the Euro, it’s been a sharp step down, the single currency down by over 1% since late Asia trade, losing more than a big figure from over 1.13 before the ECB to below 1.12 in early trade this morning, also dragging risk currencies lower as US stocks are down by over 1% into the last hour of trade. The AUD/EUR is trading at 0.627 this morning.

Brainard adds to the dovish sentiment

Speaking on the economy and monetary policy, the thoughtful Fed Governor Lael Brainard spoke of tame inflation as giving the economy room to run (in other words, don’t rush to hike if growth rebounds), risks to the economy favouring a softer Fed path (looks like she’s revised down her rate projections), and that navigating cautiously is the right path. Add into that the point from the influential John William that the Fed is now at neutral and it’s not surprising the market pared back Fed rate expectations further. The 2y Treasury yield eased a sizeable 4.68bps.

Brexit dates nigh

Bloomberg initially reported that European and UK officials were pessimistic about the chances of a breakthrough in Brexit talks, with Britain accusing the bloc of intransigence and European negotiators worried that whatever they offer won’t be enough to get Parliament behind PM May’s deal. It seems that the most likely scenario from here is that May’s deal is defeated next week (12 March) and then Parliament takes control of the process, which will likely include a vote to reject “no-deal” and then a vote to extend the exit day to allow negotiations to continue.

However, it is still a moving feast and as we go to press, Bloomberg has reported that the EU is said to make a new offer to the UK on the Irish backstop issue, bolstering the review system that aims to track progress towards getting rid of the backstop. The EU awaits a response from the UK.

Coming up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.