This is the final Australian Markets Weekly for 2021. We wish our readers a festive Christmas season. We will resume normal publication on Monday 17 January.

Analysis: Five themes for 2022 in charts that we should closely monitor

2022 is set to become a year of central banks removing monetary accommodation. NAB’s view is that the US Federal Reserve will hike rates three times in 2022, with the Bank of England also set to move. The RBA will lag as it waits for wages growth to pick up, though markets will continue to doubt the RBA given global inflation themes.

In this Weekly we explore five themes via charts that we will be watching closely which have the potential to shift tightening expectations significantly in 2022. In summary, uncertainty is likely to remain high in 2022:

(1) The path of inflation as supply chains recover and as consumers tilt from goods to services?The persistence of supply chain driven inflation has surprised sharply in 2021, partly due to the emergence of the delta variant in early 2021. As we enter 2022 it is likely there will be a belated tilt from goods to services which will put downward pressure on inflation. Australia meanwhile has lagged international trends, meaning punchy inflation prints are likely in Q4 and Q1 2022 with upside risks to trimmed mean inflation printing above the 2.5% y/y midpoint of the RBA’s band possible by Q1 2022.

(2)A virus mutation rendering vaccines less effective. Virus mutations were always to be expected but the widespread impact of Delta on prolonging pandemic effects on activity surprised us. Fortunately, it appears Omicron is mild and existing vaccines provide protection against severe illness (evidence so far). Booster shots though are required for greater protection according to prelim studies and the UK has tightened restrictions and accelerated its booster rollout. How others respond will be key.

(3) Border restrictions and a resumption of migration is important in the Australian context given the RBA’s de-facto tying of monetary policy to wages growth that would sustain inflation within the 2-3% inflation target. The longer border restrictions remain in place, the greater the likelihood that wages growth will respond more quickly to a tight labour market. Border restrictions are set to be relaxed from 15 December 2021.

(4) How financial conditions and activity respond to tighter monetary and fiscal policy? A key uncertainty remains how self-sustaining activity will be when policy is less accommodative and how financial conditions respond. It is likely the peak in rates is lower than pre-pandemic as markets price. The tilt from goods to services may also see some softening in key manufacturing countries in late 2022. The US mid-terms meanwhile likely means a Republican House and Senate (according to polls and bettering markets) with fiscal tightening more likely.

(5) Trajectory for China’s economy amid its zero-COVID strategy. China’s economy has slowed because of policies to rein in risks around its property sector, while its zero‑COVID strategy also hasn’t helped. President Xi seems to be tilting again to growth friendly policy (“ensuring stability is the top priority for the economy next year”).

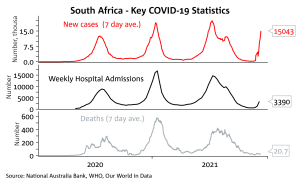

Chart 1: South Africa’s Omicron wave seeing a sharp rise in new cases, but so far not translating to the hospitalisation rates seen in prior waves and deaths remain low. Countries are taking a mixed approach with countries accelerating booster programs and tightening restrictions in the UK and Europe during the winter

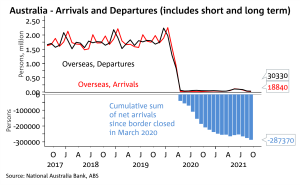

Chart 2: Australia’s closed border has seen a net outflow of 287k persons since the border was closed back in early 2020. This is putting pressure on the labour market and how quickly borders re-open and migration returns will be a key driver of whether wage pressures in certain pockets spills over to the broader labour market