Long-term signal vs. Short-term noise

Insight

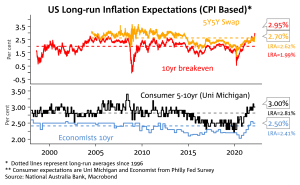

In this Weekly we explore how central banks might balance the two conflicting forces – inflation expectations key according to Fed speak.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.