AMW: Ukraine/Russia, implications for economies, central banks and Australia

History suggests Russia’s actions in the Ukraine may result in only a short-lived episode of risk aversion with contemporary macro themes eventually reasserting themselves.

Analysis: Ukraine/Russia, implications for economies, central banks and Australia

From a markets’ perspective, history suggests Russia’s actions in the Ukraine may result in only a short-lived episode of risk aversion with contemporary macro themes eventually reasserting themselves. There may also be justification for governments to consider this time as different given the scale of sanctions and military aid being supplied by EU and NATO countries.

The immediate basis for Russia’s move is reported to be to secure regime change to avoid Ukraine drifting further towards the EU and NATO, seeking a Russian Union encompassing Russia, Belarus, Ukraine, and the ethnic-Russian areas of other former Soviet Republics. It is a big challenge to the post-Cold War European geopolitical landscape.

Russia’s invasion has seen commodity prices spike (Brent oil is at US$100 a barrel), as well as sanctions being imposed, including cutting off certain Russian banks from SWIFT and limits placed on the Russian central bank’s use of its reserves. 5yr CDS on Russian sovereign debt imply a 56% chance of default. Europe’s economy is more directly exposed given its exports to Russia and Ukraine make up 0.8% of German GDP, and more so via the reliance on Russian gas (40% of gas imports).

The US economy is much less directly exposed with exports to Russia and Ukraine comprising just 0.1% of US GDP, while the US itself is a net energy exporter. Australia also has little direct trade exposure with exports to these two countries making up just 0.1% of GDP. The impact for countries outside of Europe will depend on impacts on confidence, and from higher commodity prices on inflation and activity, as well as from tighter financial conditions (including lower equity markets). There may also be second-round impacts flowing from weaker European demand.

How will central banks respond? The impact of the crisis will be to lower near-term growth and raise inflation. The growth outlook overall though remains relatively favourable, despite moderating somewhat. But an already uncomfortable inflation outlook globally will be further worsened, meaning central banks will still need to start or continue their policy normalisation moves, though for the ECB such normalisation is likely to be delayed given greater near-term growth impacts.

The potential for higher commodity prices (especially energy prices) to weigh on demand could mean central banks will act more cautiously in a hiking cycle than previously but will still be committed to achieving their inflation targets with much depending on inflation expectations.

BoE Governor Bailey noted: “If we get the second-round effects… of course we would need to react to that with higher interest rates… And the consequence of that, I have to point out, and I know I’m unpopular for saying these things, is that it would of course slow activity in the economy and it would increase unemployment.”. In such an environment markets are likely to factor in shallower tightening cycles and bring forward when the cycle may end.

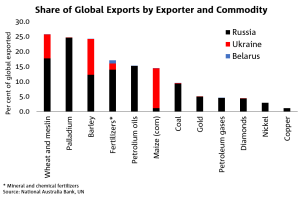

Chart 1: Russia and Ukraine are large exporters of certain commodities. Since the crisis began, prices have risen sharply for a range of commodities (see chart 4)

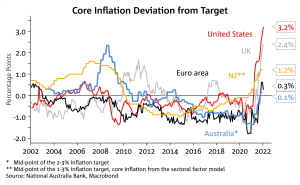

Chart 2: Central bank tolerance to higher inflation due to the Russia/Ukraine crisis will differ depending on starting points. The US, UK and NZ have less tolerance, while the ECB and RBA have more.

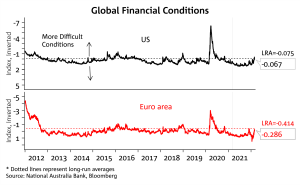

Chart 3: Financial conditions have risen on the back of the tensions, but only to average levels so far