Online retail sales growth slowed in May following a fairly strong April

Insight

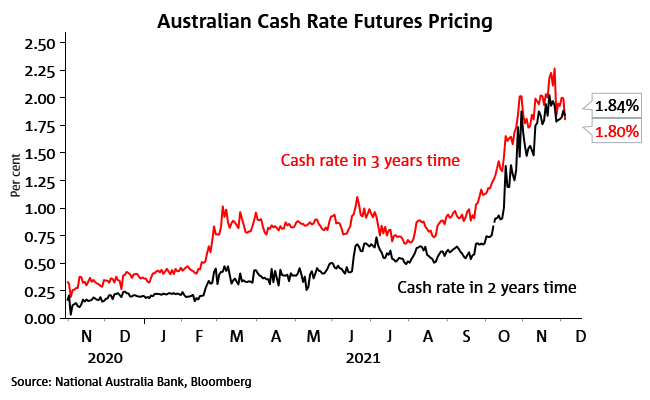

Markets might be right on the interest rate outlook.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.