Economic growth likely remained soft in Q2 2019, with GDP rising by 0.5% q/q. While growth is slightly stronger than in the March quarter, boosted by a sharp lift in net exports, private sector growth likely contracted again, with consumption still soft, dwelling investment falling further and a marginal drag from business investment. A weak outcome would likely trigger a further downgrade to the RBA’s outlook, notwithstanding support from income tax refunds, cash rate cuts, a lower exchange rate and a stabilising housing market. More importantly given the RBA’s focus on the labour market, persistent weakness in private demand points to unemployment edging higher. We continue to expect the RBA will lower rates by November, but acknowledge the risk of an additional easing and/or a move to unconventional policy next year should the economy weaken further, particularly now that global risks have intensified.

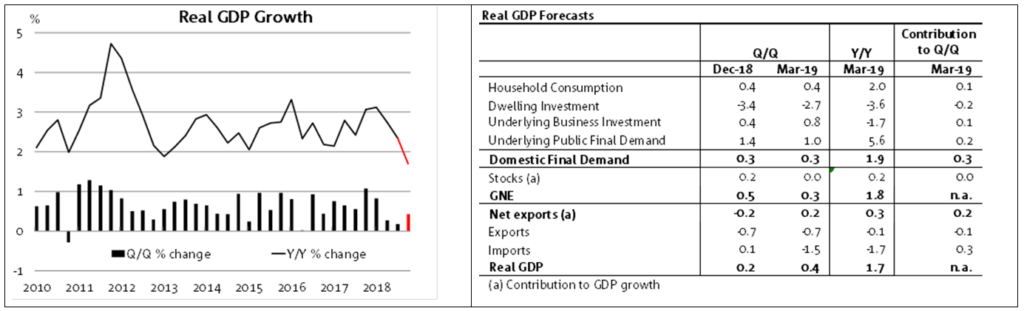

Wednesday’s GDP figures are forecast to show another weak – but slightly improved quarterly outcome – with growth printing at 0.5% q/q and annual growth slowing to 1.4% y/y. That would be the weakest annual growth since 2009, driven by a contraction in private demand. Household consumption growth looks to have remained weak, on the back of sluggish retail sales and a slowing in the growth in services consumption. Residential construction is also expected to decline, with work done data suggesting another large fall of around 5% q/q. Business investment looks to have declined slightly in the quarter but will make little overall contribution. Offsetting the weakness in domestic private demand in the quarter will be a sizeable contribution from net exports on the back of a surge in iron ore exports, while the public sector is expected to again grow strongly.

Looking forward, we expect a small improvement in growth, but for the overall pace to remain below trend. We expect year average growth of around 1½ in 2019, before lifting to around 2¼% in the next two years. The private sector is likely to remain weak with dwelling investment expected to decline further (falling by another 10% or so) and household consumption growth to rise to just over 2%. Exports are expected to level off after the last of the LNG mega-projects ramps up to full capacity. Supporting growth is likely to be ongoing increases in government sector spending, with the continued rollout of the NDIS, and a large infrastructure pipeline. We also expect business investment to make a solid contribution to growth, with the decline in mining investment tailing off and a rise in the non-mining sector on the back of public infrastructure spillovers.

The key uncertainty around our forecasts is the outlook for business investment. We currently forecast solid growth in the business sector over the next few years. However, the NAB Business survey points to a significant loss of momentum in the business sector over the past year or so, and globally investment has pulled back on heightened uncertainty around trade ructions and other geopolitical issues.

Monetary policy implications: Weak private sector growth is likely to force the RBA to confront its forecasts for a gradual improvement in the labour market as well as see further revisions to the growth outlook. With inflation remaining weak and a backdrop of heightened global risk, stalling private sector demand is likely to see further easing in monetary policy, where we expect a further 25bp cut to 0.75% by November. However, with risingglobal risks related to trade and downside risk to our outlook for business investment, it’s possible the RBA will further cut the cash rate and/or move to unconventional policy should the economy slow further.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.