On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Theresa May’s government faced a massive defeat in Parliament with a 230 vote loss on their Brexit withdrawal agreement.

https://soundcloud.com/user-291029717/brexit-vote-defeat-confidence-vote-and-a-sterling-hit

The British pound came under pressure in front of the just completed vote on the Prime Minister’s Brexit withdrawal Agreement, which she has lost by a crushing 432 to 202 votes. Sterling is bouncing on this, on the view that the Labour opposition no confidence motion just tabled will be defeated (on Wednesday) and that an extension of Article 50 and a possible second referendum are the singularly most likely ways forward from here. We’d agree.

Plenty of other significant news overnight, including:

ECB President Mario Draghi speaking to the EU parliament in Strasbourg, where he notes that:

| “The question we should ask is: Is this a sag or heading toward a recession?” Draghi told members of the European Parliament in Strasbourg. “The answer we give is: No, it’s a slowdown, which is not headed toward a recession. But it could be longer than expected.”

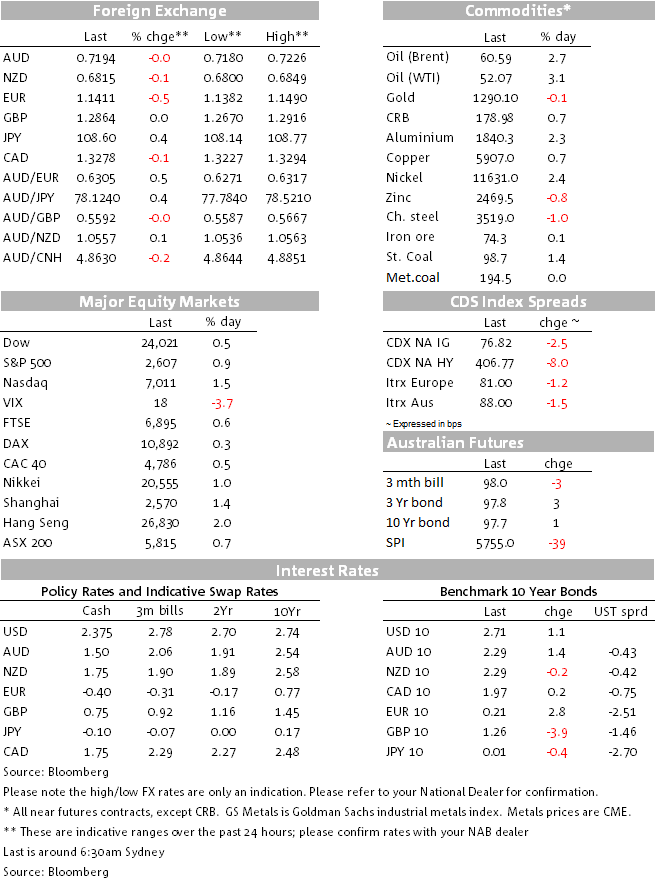

“We still see a situation where consumption is still expanding, relatively strong, investment still expanding, supported by our monetary policy, export growth is still good and the labour market keeps on being very strong,” Draghi said. “All this is happening at lower and lower growth rates.” “A significant amount of monetary-policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term,” he said. China December Loan data published just after we went home yesterday shows both new Yuan Loans and Aggregate Financing expanding by more than expected last month, New Yuan loans by ¥1.08tn against ¥825bn expected and Aggregate Financing by ¥1.589tn against ¥1.3tn expected. The credit numbers came hot on the heels of Chinas’ announcement yesterday afternoon of additional of fresh economic stimulus measures to support its economy in the form of tax cuts for small businesses and higher public spending. Officials said they would cut taxes “on a larger scale” in order to boost business activity, announced against a backdrop of disappointing industrial production figures and the first drop in car sales for almost three decades. While exact details of the stimulus package are yet to be unveiled, the Chinese finance ministry suggested the measures would include cutting value added tax for some companies, particularly in the manufacturing sector, as well as rebates for other businesses to ward off a more damaging slowdown. Some estimates we have seen this morning suggest the fiscal stimulus could be worth in the order of 1% of GDP. US January Empire Survey fell by much more than expected, to 3.9 from a revised 11.5 in December, following the earlier sharp drop in the December ISM manufacturing survey in December The US administration has just admitted to a bigger than earlier estimated economic impact from the partial government shutdown (due to private sector contractors unable to work as a result of the shutdown). It now reckons growth will be 0.1% per week lower, double the prior estimate of 0.1% per fortnight (last weekend, S&P estimate the shutdown was costing $1.2bn per week or about 0.6% of GDP, closer to the original White House estimate) FXGBP fell by as much as 1.5 cents against the USD in the hours leading up to the Brexit vote (to a low of around 1.27) but currently sits at 1.2865 following the heavy defeat for PM May’s Withdrawal agreement and which, as per above, now sees markets starting top price for an extension of Article 50 and a possible second referendum. This is despite EU official now out in force suggesting that the chances of disorderly ‘no deal’ Brexit have increased. AUD has been choppy between about 0.7220 and 0.7180 (0.7194 now) with really not much to say about overnight activity which has tended to fluctuate with swings in broader risk sentiment but where a broadly firmer US dollar has been the overriding feature, GBP volatility aside, and led by weakness in EUR/USD off the back of Draghi’s above comments and which has pushed the single currency down to its lowest levels since January 4th. EquitiesUS equities are higher, led by 6-7% gains for Netflix ahead of its Q4 results tomorrow an following new pre-market open that it was raising subscription prices (from $11 to $13) – the largest rise in its 12 year history and first time all 58 million subscribers will be affected simultaneously. In corporate earnings, JP Morgan missed its earnings estimates due to a sharp slowing in fixed income trading revenue in Q4, amidst the surge in market volatility, but its share price has recovered from earlier falls to be up marginally on the day (0.45%). JPM’s core loan book increased 6.7% on the year, above the bank’s 6% target, despite some softening in demand for mortgages amidst higher rates. Wells Fargo’s results were less well received, its 5% drop in revenue seeing its stock off 1.9%. The earnings season continues tonight with other US banks reporting (including MS, GS and BoAML). Broader indices are up by between 0.5% (DJIA) and 1.5% (NASDAQ) half an hour ahead of the close. BondsUS Treasury yields are very narrowly mixed, 2s -0.6bp to 2.529% and 10s -0.2bp at 2.709%. Nothing to see here. CommoditiesOil has staged a decent rebound after a few days of loss, both blends up $1.50 and where yesterday’s economic stimulus announcements from China is being given credit. This also looks to have supported base metals with aluminium and nickel both up more than 2% and copper by 0.7%. |

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.