Spending more subdued in January & February 2025

Insight

The ECB’S new strategy has driven the Euro higher in a market which has generally been driven down by COVID concerns. NAB’s David de Garis explains what’s changed in the ECB’s 2% inflation target.

https://soundcloud.com/user-291029717/2-percent-or-not-2-percent-that-is-the-question?in=user-291029717/sets/the-morning-call

Not quite in the spirit of Scorpion’s song which was inspired by the fall of the Soviet Union, but then became the unofficial anthem for the German Reunification in 1989, there is certainly a wind of change in markets at the moments, a few weeks ago the major concern was about inflation with the Fed signalling the potential for tapering discussion amid high US inflation and the prospect for a fast labour market recovery. Now, the concern is that growth may prove temporary instead of inflation! Risk aversion is in the air with US and EU equities sharply lower alongside a decline in core global yields. Safe haven currencies have outperformed while pro-growth pairs like the AUD and NZD have been sold.

There has not been a single catalyst triggering a turn in sentiment, instead it seems that an accumulation of events has culminated in a big u turn towards cautiousness. The flattening of the UST curve following the Fed signalling the potential for a QE tapering, has moved from a perception the Fed will rein in inflation to potentially choking the recovery, central bank tightening expectations has not just been a Fed story, rate hike expectations for other central banks have also been brought forward including the BoE, BoC, RBNZ and RBA. Meanwhile the rapid spread of the Covid Delta variant has also raise concerns the global growth recovery could be derailed, countries with high vaccination rates like the UK remain committed to their reopening strategy, but we don’t know yet if this strategy will work. So far, UK hospitalisation numbers remain relatively low, even with infections rising, so markets hope that more restrictive measures will not be required. That said, its important to stress this is not just about hospitalisation rates, the consumer needs to feel comfortable with this strategy, otherwise they will stay home regardless of government policy.

Against this backdrop news over the past 48 hours of potential easing from China and more inflation leniency from the ECB have provided more fuel to the fire of concern, instead instigating more confidence on the growth recovery story.

As preluded by leaked reports yesterday, the ECB has moved up its inflation goal to 2% with symmetric approach from the previous “below, but close to, 2% over the medium term,”. The change seems to have been instigated as many within the Bank felt the previous goal was too vague and led to calls for tighter policy too soon. Importantly, as well, the ECB said that when interest rates are close to their lower limit, as they are today, the economy requires “especially forceful” monetary stimulus that could “imply a transitory period in which inflation is moderately above target.”

Stressing this point ECB president said that the new wording “removes any possible ambiguity and resolutely conveys that 2% is not a ceiling,”. Lagarde also noted that the goal was agreed unanimously while also differentiating the new strategy from the one now pursued by the Fed insisting that the ECB is not doing average targeting. The ECB also confirmed it will now include considerations on climate change in its monetary policy operations and the review also recommends the inclusion of owner-occupied housing costs in their supplementary measures of inflation. (like the US has with owners-equivalent rent). In the context of fast rising house prices in Europe, this might be one way to make it easier for the ECB to meet an inflation target which it has missed for the best part of a decade. There was little market reaction to the announcement.

The ECB indicated it would eventually tilt QE bond purchases away from carbon-heavy companies and those which don’t have credible carbon reduction plans. It also said it would take these factors into account under its wider market operations (i.e. the terms under which it accepts collateral from banks when it lends cash). The RBNZ recently said it is evaluating whether to change its own collateral framework, to take account the likes of climate change risks

Yesterday, China’s 10-year government bond yields closed at 2.98%,7.5bps lower following the reports of China’s State Council urging the PBoC to ease policy (via RRR cut). This announcement alongside the ongoing China crack down on IT companies didn’t help equities in the APAC, China’s CSI 300 eneded the day -1.02% and Hang Seng -2.89% and the Nikkei closed down 0.89%, not helped by news of a state of emergency declared for Tokyo.

Following the negative lead from Asia, US and EU equities also closed sharply lower with pro cyclical sectors leading the decline. The Stoxx Europe 600 Index fell -1.72%, the most since May 11 with Retail (-3.1%) while miners (-2.9%) among the big underperformers. Meanwhile in the US the S&P 500 ended the day -0.86%, but this was not a bad outcome bearing in mind the index had collapsed closed to 1.6% during its first hour of trading. Like in Europe, pro cyclical sectors were the underperformers, financials led the decline ( -1.96) with industrials (1.43%) and materials (-1.36%) not too far behind. Notably, bearing in mind the falls in longer dated UST yields (more below) which usually help growth IT related companies, the NASDAQ was unable to cope with the broad risk aversion ending the day down -0.72%.

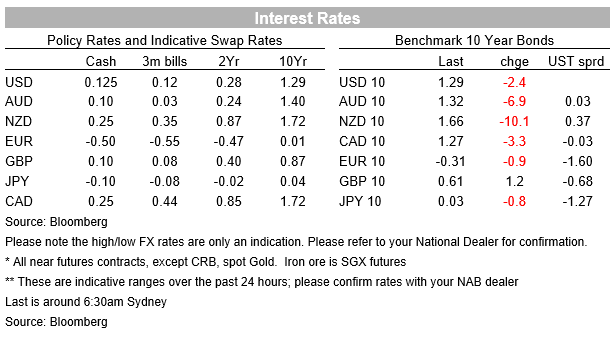

10y UST yields fell to a low of 1.2470% during the first half of the European session, a 4½ month low and some 50bps off its late March highs . Later during the US session, as equities came off their lows, UST yields also recovered somewhat with the 10y Note now trading at 1.2928%. In addition to the risk aversion in the air, lack of supply, break of technical levels have contributed to the decline in UST yields. Next week new round UST issuance will be a big test for the market.

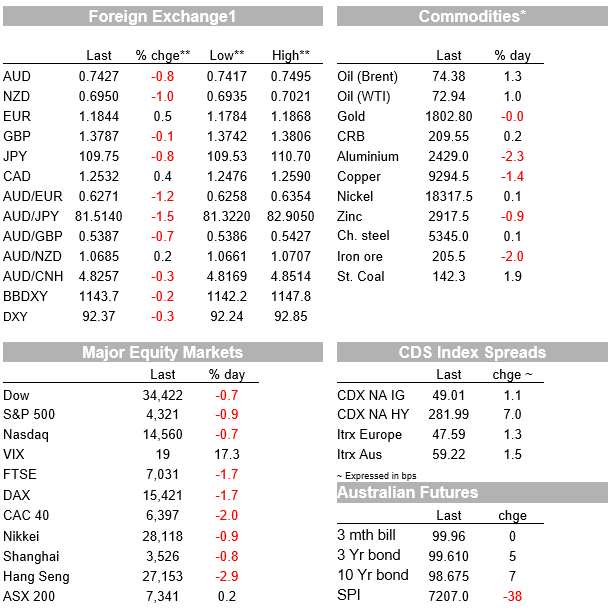

Moving onto FX, safe haven currencies have been the outperformers with CHF and JPY up 1.05% and 0,8% respectively . USD/JPY (now at ¥109.75) has broken below its recent uptrend with the technical picture suggesting it now has room to fall a bit more. The Euro has also managed to outperform the USD, up 0.44% to 1.1845.

Although the USD is down in index terms (BBDXY and DXY -0.20%), pro- growth currencies are the big underperformers with NZD leading the decline within G10 , down 1.07% and now trading at 0.6956. AUD has not done much better, down 0.80%, trading at 0.7429, after printing an overnight low of 0.7417.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Spending more subdued in January & February 2025

Insight

Business confidence falls back in February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.