Long-term signal vs. Short-term noise

Insight

Softer US consumer confidence and a JOLTs report suggesting ongoing rebalancing in the labour market saw the US dollar and US yields lower, while equities were higher.

GE: GfK consumer confidence, Sep: -25.5 vs. -24.5 exp.

US: JOLTS job openings (k), Jul: 8827 vs. 9450 exp.

US: Conf. Board consum. confid., Aug: 106.1 vs. 116.0 exp.

Softer US consumer confidence and a JOLTs report suggesting ongoing rebalancing in the labour market saw the US dollar reverse lower. US equities rose strongly, the S&P500 up 1.5% to notch its third straight day of gains, while US yields fall, led by a 17bp fall in the 2yr yield as Fed pricing was pared.

JOLTs data for July gave about as compelling a case as could have been hoped for from that release that the labour market continues to soften even as the unemployment rate remains low. That saw bets on near-term tightening pared and yields fall. There is now a 37% chance priced of a further hike by November, down from 46%, and 107bp of cuts priced by the end of 2024, down from 91bp. US 2yr yields were 17bp lower at 4.88%, the curve bull steepening with 2s10 spread rising to -77bp and 10yr yields falling 9bp to 4.11%. Fed Chair Powell reaffirmed at Jackson Hole that “getting inflation sustainably back down to 2 percent is expected to require … some softening in labor market conditions. ” JOLTs data for July has done its part, with attention now turning to whether August Payrolls on Friday further supports a story of ongoing rebalancing with ADP private payrolls today overnight tonight a potential source of noise ahead of the official BLS data.

Corroborating evidence came from a sharper-than-expected fall in consumer confidence from the Conference Board, which fell to 106.1 from a downwardly revised 114.0, well below expectations for 116. There were roughly equal drops in the current conditions and expectations components. The gap between the jobs “plentiful” and jobs “hard-to-get” index fell to its lowest level since early 2021.

As for the detail, JOLTs job openings declined to 8.8mn from 9.2mn (revised down from 9.6mn), well below the consensus for 9.5mn. JOLTs continues to indicate that the labour market has indeed softened, despite the sideways movement in the unemployment rate. Openings peaked at 12.2mn in March 2022 when the unemployment rate was 3.6%. Openings have fallen more than a quarter, while the unemployment rate is a tenth lower. The number of Openings per unemployed person has fallen from a peak of 2 to 1.5, but remains above its prepandemic levels of about 1.2.

The hiring rate in the JOLTS survey slowed to 3.7%, around 2019 levels, while the layoffs rate held at 1.0% for a fourth month in a row, below 2019 rates around 1.8mn. The quits rate fell to 2.3% from 2.4%, and is now below prepandemic peaks and where it was through most of 2019. All in all, an environment of slowing turnover, lower voluntary quits and cooler hiring, but without a sharp pick up in layoffs. That said, Chair Powell also said at Jackson Hole the Fed was expecting further rebalancing, and the data will need to continue to play ball for the Fed to stay on hold, “ evidence that the tightness in the labor market is no longer easing could also call for a monetary policy response”

In other news, there has been more talk of incremental policy changes in China. Bloomberg reports that China’s largest banks are preparing to cut interest rates on existing mortgages, in what would be a target push to spur consumer spending and the latest effort by the government to shore up growth. Meanwhile, Chinese media report the Finance Minister vowing to strengthen policy support and speed up government spending as the economy comes under strain, ahead of an important Politburo meeting.

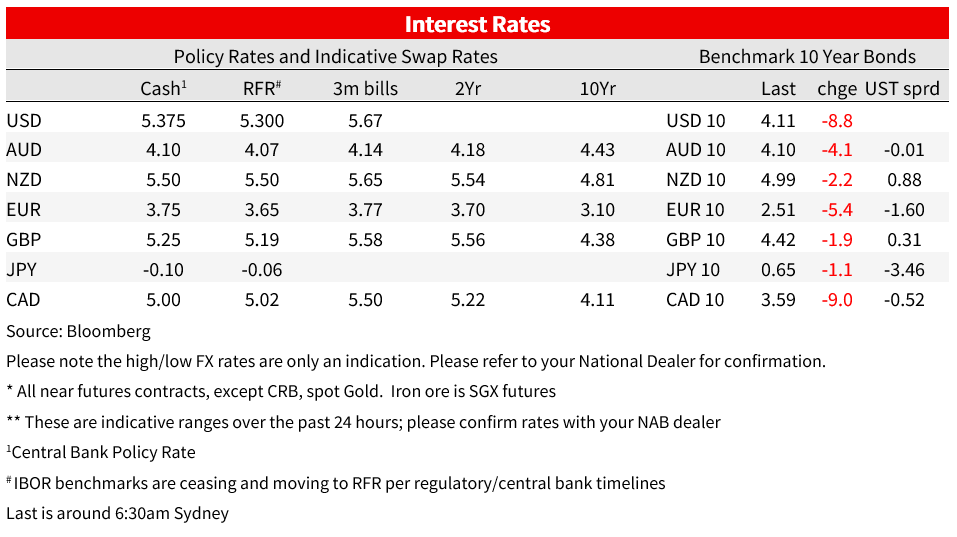

Lower US rates spilled over into other markets, with European rates lower, although more modest falls compared to the US. Germany’s 10-year rate is down 5bps on the day compared to a net 8bps fall in the US 10-year.

In currency markets, the US dollar is weaker, down 0.6% on the DXY to 103.5. All G10 currencies gained against the USD, with the Scandinavians leading the pack, followed by the AUD and NZD against the backdrop of lower US yields and positive risk sentiment. The AUD was 0.8% higher to 0.6483 and currently sits near its intraday high of 0.6487 reached late in the US session. Ahead of the US data, the US dollar was broadly stronger, with the AUD gaining from an intraday low of 0.6401 just before the JOLTs data. The Euro was 0.6% higher to 1.0884, while USDJPY lost 0.5% to 145.78.

US Equities were sharply higher. The S&P500 posted its third consecutive day of gains and its largest 3-day gain since March, up 1.5% on the day . The S&P500 is now 3.7% above its intraday low on 18 August, and just 2.4% off its recent 28 July intraday high. Gains on the day were broad-based, with all 11 sectors in the S&P500 index in the green. Gains were led by communication services, consumer discretionary, and IT. The Nasdaq was 1.7% higher. It was also a positive tone for equities elsewhere. The Euro Stoxx 50 gained 0.8%, the Nikkei was 0.2% higher, while the Hang Seng gained 1.9%.

Yesterday evening, the RBA’s current Deputy and soon-to-be Governor gave a lecture at ANU. The speech was a discussion of the implications of climate change on the economy and for monetary policy, but there were not firm conclusions of relevance to the rates outlook. (for the speech, see Climate Change and Central Banks). In the Q&A, Bullock said inflation was still too high and her “first priority is still to maintain a focus on bringing inflation back down to target.” She said they may need to raise rates again “and we’ll be taking decisions for the time being until next year at least month by month.” No surprises there. Markets price around a 2 in 5 chance of another hike by year-end.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.