NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There’s still no sign of an end to the US China trade dispute as the end of the cease-fire period draws closer.

https://soundcloud.com/user-291029717/delays-good-and-bad

Risk assets have been boosted in the past hour amid speculation the US is considering lifting trade tariffs on China in order to appease markets. The report suggests this is a debate between trade officials with President Trump not yet involved in the discussion, so at this stage the news is on the speculative side and as we are about to press the send button WSJ is reporting the US Treasury is denying there has been any China tariff recommendation.. More often than not where there is smoke there is also fire, but it is hard to tell at this stage.

Prior to these headlines US equities where modestly trading in positive territory with solid US data releases one positive driver while disappointing Morgan Stanley results didn’t result in negative contagion within financials. Rumours that President Trump might impose tariffs on EU auto imports were also source of cautiousness. Meanwhile in G10 GBP is the outperformer buoyed by speculation of a delay to Article 50 and support for a second referendum.

After an up and down move over the past 30 minutes, US equities look set to end the day in positive territory with the S&P 500 currently up 0.54% and looking set to record its 8th session of gains in the last ten days. Many investors are keeping a close eye on technical levels for signs on whether the index still has room for further gains or whether is best to take profit, for a instance a close above the 50 day moving average would be a positive sign, notably too all 12 sectors of the S&P 500 look like they will close in positive territory.

Elsewhere, Taiwan Semiconductor (TMSC), the world’s largest chip maker, reported a surprise drop in revenue, citing a weaker macroeconomic environment amidst a slowdown in iPhone sales and pressure on Huawei. And Alcoa forecast that aluminium demand would slow to it its lowest rate of growth in a decade at its earnings report, suggestive of slowing global growth (although better than expected earnings boosted its share price nonetheless). After a wobbly start, Netflix shares are up on the day ahead of results set for release after the market close.

Aside from the US China trade headlines mentioned above, early in the session European equities traded in a cautious mode following comments from US Senate Finance Committee Chair Chuck Grassley noting that he thought President Trump was ‘inclined’ to impose tariffs on European cars to win better terms on agriculture. Grassley news knocked the EU auto sector, while financials traded softer following disappointing Q4 results from Soc Gen.

UST yields continue to track moves in equities and are up across most of the curve with longer dated yields unchanged resulting in a slight flattening bias. The 2yrs and 10yrs are up 3bp to 2.56% and 2.74%, respectively. Early in the session UST yields were boosted by better than expected US data releases. The Philadelphia Fed business survey unexpectedly rose, going against the grain of weakness in other manufacturing surveys, but the underlying components were more mixed (there were falls in the employment and shipments components but a rise in new orders). Jobless claims declined, although there can be issues adjusting for seasonality at this time of year, compounded at present by the ongoing US government shutdown.

After some volatility following the trade headlines above, USD indices are little changed ( DXY at 96.07) and within G10 GBP is the outperformer, up 0.70% to 1.2976 following increasing speculation of a delay to Article 50 and growing support for a second referendum. The FT reported today that the UK had informed the EU before Christmas that if the talks carried on into the New Year (as they have) the UK did not have enough time to pass all the pieces of legislation that it needs to meet the 29 March deadline. The implication being that the UK will have to request an extension relatively soon, though Theresa May continues to publicly say that she wants the UK to leave as planned in March. May has met politicians from other parties (although not Jeremy Corbyn), but has refused to shift her ‘red lines’ at this stage (i.e. she won’t countenance a customs union solution). She needs to return to parliament with a “Plan B” on Monday, with voting on that to take place on 29th January. Early this morning GBP was also supported by a You Gov poll showing 56% would now vote to stay in the EU, against 44% who want to leave. YouGov noted that the 8% swing from Leave to Remain since the 2016 referendum was significant.

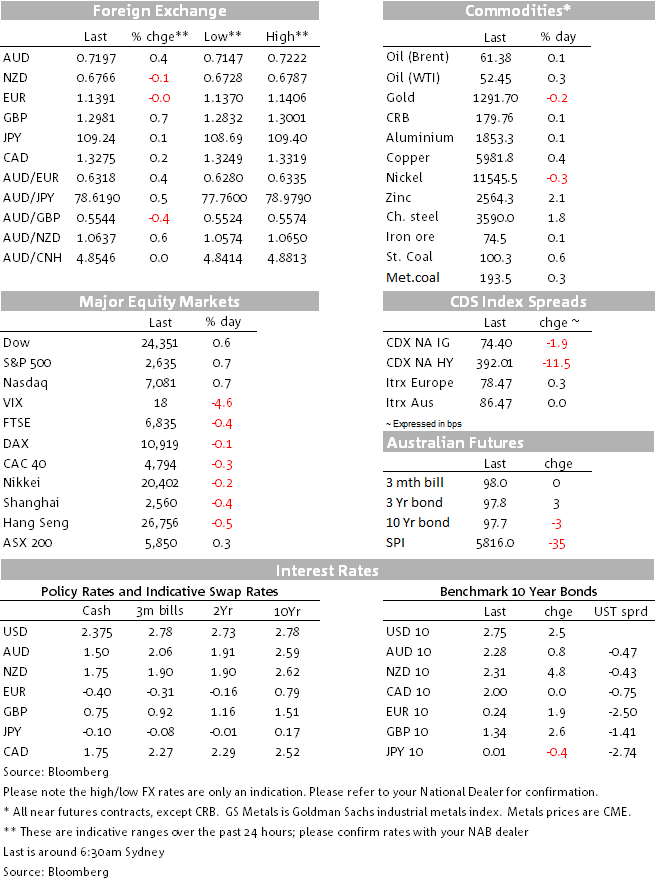

The AUD now trades just below the 72 mark. Yesterday the pair traded down to a low of 0.7147 not helped by disappointing AU loan figures and a softer equity backdrop in APAC. Overnight the AUD steadily regained lost ground and the US China headline this morning saw the pair briefly jumped to 0.7221, but the US treasury denial has seen the AUD trade back close to the figure. For now it is evident the AUD remains at the mercy of offshore events, worth noting however that the Q4 CPI figures are out on January 30th ahead of the RBA meeting on February 5th. Yesterday NAB released a CPI preview noting that preliminary forecast for Q4 CPI is for low headline and core inflation outcomes.(Q4 headline inflation of +0.3% q/q, +1.6% y/y; trimmed mean of +0.3 to 0.4% q/q, +1.7% y/y, and; weighted median of +0.4% q/q, +1.6% y/). So although for now the AUD looks to be driven by offshore events, we think before the end of the month domestic issues will become the focus and if we are right about a soft CPI, the AUD will struggle to perform in that environment

The NZD has underperformed again, and is amongst weakest of the G10 currencies over the past 24 hours. The pair now trades at 0.6766 and NZ CPI, released on Wednesday, is the key data release the market is focused on

Moves within commodities have been relatively modest. Oil prices are essentially unchanged, Gold is a tad lower and Iron ore a tiny bit higher.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.