Confidence and Conditions Lift

Insight

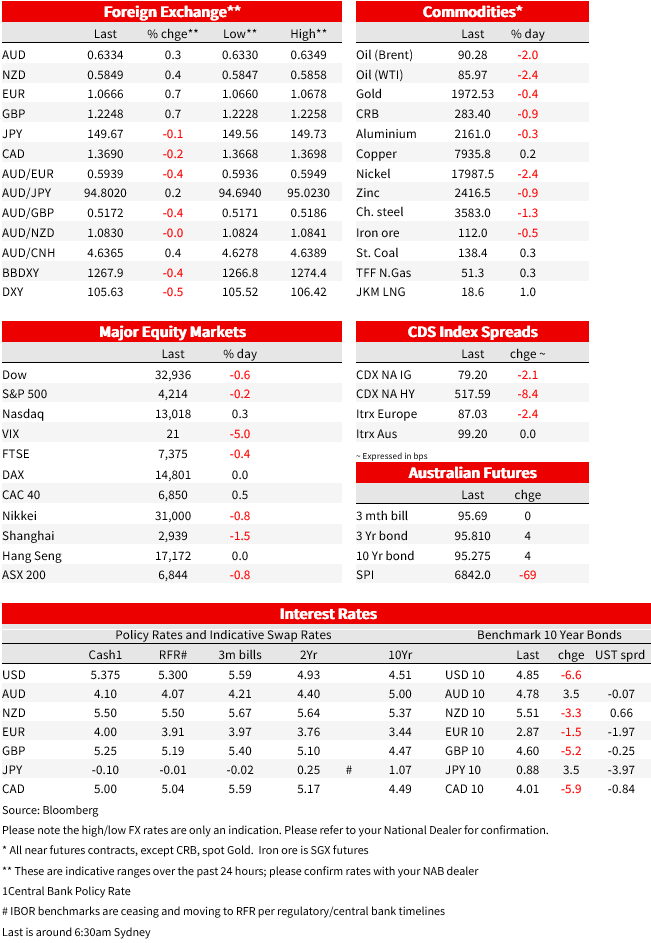

A quiet night for data, but a big night for bonds.

BBG: Ackman, Gross Abandon Bearish Bond View as Yields Bounce Off 5%

A quiet night for data, but a big night for bonds. The US 10yr yield hit an intra-day high of 5.0187%, but not soon after fell back to finish at 4.85% (low 4.83%) and is down -6.5bps over the past 24 hours. Why the big moves? Unclear. It could be 5% is now proving attractive with the real yield as given by the 10yr TIP yield trading recently as high as 2.54%. There were also two comments by investors that captured headlines. Former bond king Bill Gross tweeted “regional bank carnage and record rise in auto delinquencies to long-term historical highs indicate US economy slowing significantly. Recession in 4th quarter…’higher for longer’ is yesterday’s mantra ”. Bill Ackman also tweeted that he covered his bond short, noting “there is too much risk in the world to remain short bonds at current long-term rates. The economy is lowing faster than recent data suggests”. The notion the US economy is slowing against resilient official data was first advocated by the Fed’s Barkin last week.

US fed funds pricing is little changed with the Fed universally expected to be on hold in November and there is only a cumulative 9.4bps worth of hikes priced by January 2024. Pricing of cuts though has expanded slightly with -82bps priced for 2024, from -80bps on Friday and -76bps this time last week. Equity markets moved alongside the volatility in Treasury yields. The S&P500 fell -0.2% today, but at one point it was down -0.8%. The NASDAQ though did close up 0.3%. Key earnings come after the close today with Alphabet and Microsoft reporting, though there is also plenty of non-tech names too (see Coming up for details). One interesting move not usually covered in our dailies is Bitcoin which is up some 4.5% over the past 24 hours to $31,212; a US court has cleared the way for a crypto ETF, perhaps by year’s end.

In FX, the USD broadly reflected the moves in yields. At one point the DXY was up +0.2%, but reversed and is now -0.5% with most major pairs reflective of that: EUR +0.7%, GBP +0.7%. Both the AUD (+0.3%) and NZD (+0.4%) underperformed and the NZD did fall to a fresh year-to-date low of 0.5808, before the reversal in the USD and the NZD currently trades at 0.5849. For the AUD, the lows seen earlier this month held and, after dipping below 0.63, the currency trades at 0.6335. JPY has been remarkably contained despite the volatility in yields. The market reaction to Sunday’s Nikkei report saw another push higher in Japan’s 10-year rate, to a fresh 10-year high of 0.86%, while the yen was largely unperturbed. USD/JPY briefly traded above 150 in early Sydney, before settling just below that figure (USD/JPY -0.2%).

In developments on the Israel-Hamas war, Israel continues to hold off on its planned ground assault on Gaza , against a backdrop of further diplomatic efforts to prevent the conflict from spreading. Bloomberg reports insiders suggest growing calls inside Israel for a rethink of the planned ground invasion, due to the uncertainty about the fate of over 200 hostages being held in Gaza, fear of Hezbollah in Lebanon invading Israel from the north, and the risk of heavy Israeli military casualties. Meanwhile, Israel continues with its aerial bombardment of Gaza and with strikes at Hezbollah forces in Lebanon. The oil market continues to trade as if the conflict won’t spread to involve large oil producers like Iran. Brent crude -2.1% to $90.19. Gold more steady at -0.3% to $1,974.79.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.