On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

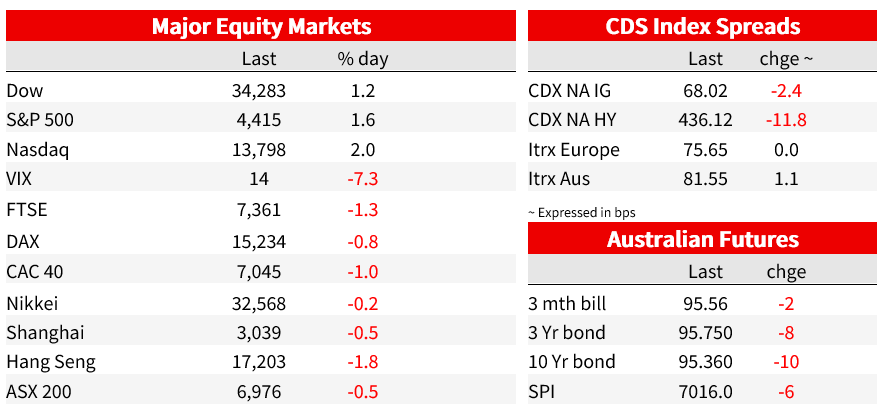

US equities recorded a solid end to the week with the S&P 500 closing above the 4400 psychological mark. Equity investors showed little reaction to news of a downbeat consumer

NZ: Manufacturing PMI, Oct: 42.5 vs. 45.3 prev.

UK: Industrial production (m/m%), Sep: 0.0 vs. 0.0 exp.

UK: GDP (q/q%), Q3: 0.0 vs. -0.1 exp.

US: U. of Mich. cons. Sentiment, Nov: 60.4 vs. 63.7 exp.

US: U. of Mich. 5-10yr inflation exp, Nov: 3.2 vs. 2.9 exp..

Hot thoughts all in my mind all of the time, yeah

Hot thoughts all in, all in my mind all of the time – Spoon

US equities recorded a solid end to the week with the S&P 500 closing above the 4400 psychological mark. Equity investors showed little reaction to news of a downbeat consumer, the University of Michigan Sentiment Survey recorded a sixth month low, but the big surprise was the jump in inflation expectations in both the 5 to 10y and 1y ahead readings. The UST curve extended its bear flattening with the 10y Note closing at 4.65%. The USD struggled on Friday but recorded its best week in two months. AUD declined for a fifth consecutive on Friday and starts the new week at 0.6361

The S&P 500 gained 1.56% on Friday driven by tech stocks while the NASDAQ climbed 2.05% . The NASDAQ’s gain was the strongest since May while the S&P 500 closed above the 4400 mark which many regard as an important resistance level, boding well for further gains ahead. Microsoft and Nvidia stole some of the headlines with the former climbing above $369 (a new record high, +2.49% on the day) while the latter extended its recent gains to an eighth consecutive day .

US equity investors showed little reaction to news of a downbeat consumer, the University of Michigan Sentiment Survey recorded a sixth month low, falling to 60.4 from 63.8 and well below the consensus, 63.7. That said, the surprise was the jump in inflation expectations, the five to ten year reading climbed to 3.2% from 3.0%, slightly above the previous cycle high, 3.1% (highest since 2011) with the one-year inflation expectations also rising, to 4.4% from 4.2%.

The director of the survey pointed to a combination of persistently high prices, high borrowing costs, and labour market weakness for the decline in sentiment which does not bode well for consumer spending ahead. Meanwhile many economists suggest that the increase in inflation expectations was likely driven by the recent rise in headline inflation fuelled by higher gasoline prices. If so, a decline in expectations looks likely given that gasoline prices have fallen by almost 13% over the past two months. This should be of some comfort but given Fed apprehensions that the recent downturn in inflation could stall, the rise in inflation expectations will do little ease these concerns.

Looking at equities’ performance month to date, tech stocks have been the big winners with the NASDAQ up an impressive 7.89% with Japan’s Nikkei outscoring the S&P 500, up 6.1% vs 5.96% for the latter. Meanwhile Chinese equities remain in struggle street with the CSI 300 0.08% on the week while the Hang Seng was -1.17%.

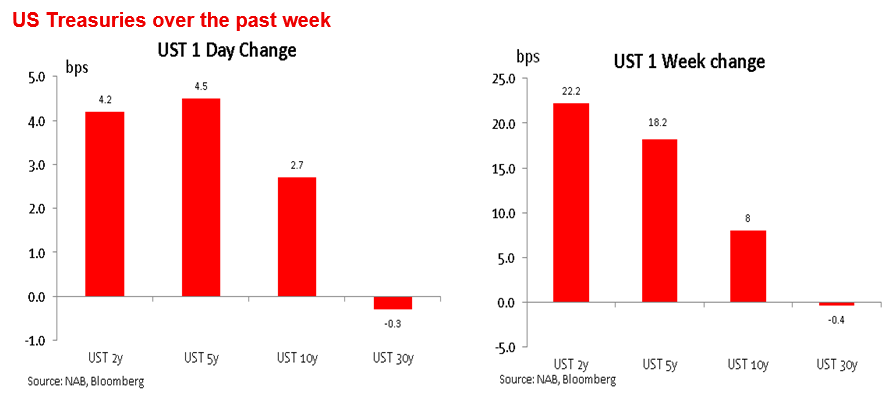

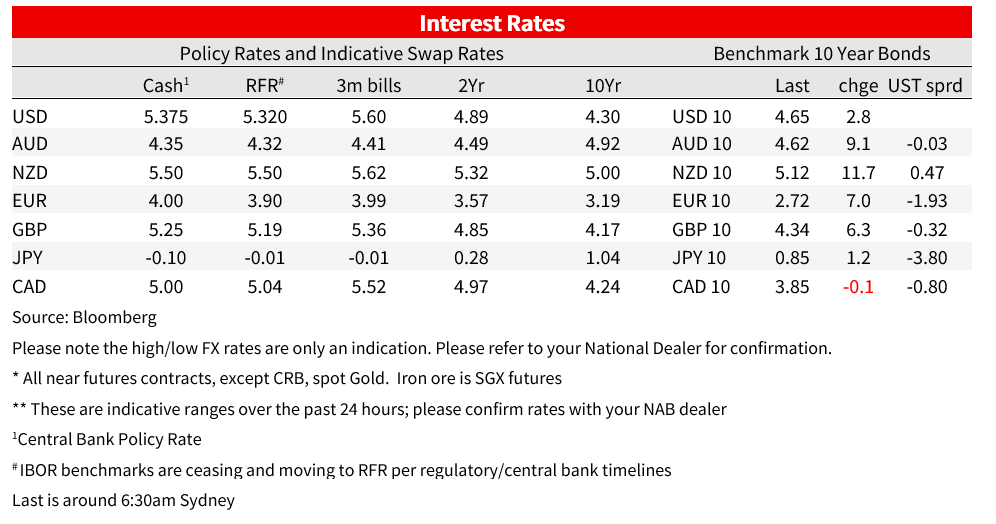

Moving onto the rates market, the US Treasury curve extended its bear flattening with the 2s10s curve flattening another 1.5bps, to -41bps , that is a 14bps decline over the past week. Front end yields drove the move on the day (2ys up 4.2bp to 5.063% on Friday) and the week (up 22bps over the past week). The 10y Note ended the week at 4.65%, up 2.5bps relative to Thursday’s close, but looking at the intraday chart volatility remains a theme with the benchmark yield recording intraday low of 4.56%, trading in a 9bps range and closing at the highs for the day. Looking ahead the market will be paying close attention to the October CPI out on Tuesday and October Retail Sales out on Wednesday.

Fed speakers on Friday supported Fed Chair Powell’s inflation concerns and bias for further tightening. Speaking to CNBC, San Francisco Fed Daly noted that although policy is restrictive, more could be warranted, if inflation goes higher or even stays sideways. Daly then added that the decrease in tighter financial conditions places more likelihood of further policy prescription. Fed Bostic (Atlanta) retain his dovish credentials saying “I think we will get to our 2% target without us having to do anything more. We are well positioned to let things happen. The words I used are patient, cautious and resolute.”

After the bell, Moody’s downgraded the US sovereign rating outlook from stable to negative, citing downside risks to the US’ fiscal strength and pointed to a sharp rise in debt servicing costs and ‘entrenched political polarisation’. Moody’s is the only major credit agency that maintains a AAA rating for the US.

Meanwhile on the US political front, the risk of an imminent US government shutdown on November 18 eased after House Speaker Mike Johnson proposed a compromise temporary funding plan without insisting on deep spending cuts that ultraconservatives have sought . Bloomberg noted that the proposal, which omits new funding for aid to Israel and Ukraine, would extend funding for some government agencies to January and others to February. While the two-step idea risks Democratic pushback, it is more likely to pass the Senate given its lack of immediate spending cuts.

European yields also moved higher on Friday with hawkish remarks from ECB Lagarde helping the move . The ECB President said the deposit rate will stay at 4% for an extended period of time, with potential for borrowing costs to rise again if necessary. Two-year Bund yields rose 6bps to 3.06% and 10-year yields climbed 7bps to 2.71%. Meanwhile UK Gilts rose 6-8bps across the curve; money-markets pared bets for BOE cuts next year to price 57bps of easing by December, down from 62bps earlier Friday. The UK Q3 GDP numbers came better than expected, at 0% vs -0.1% consensus with consumer spending, business investment and government spending all falling with net trade the offsetting force.

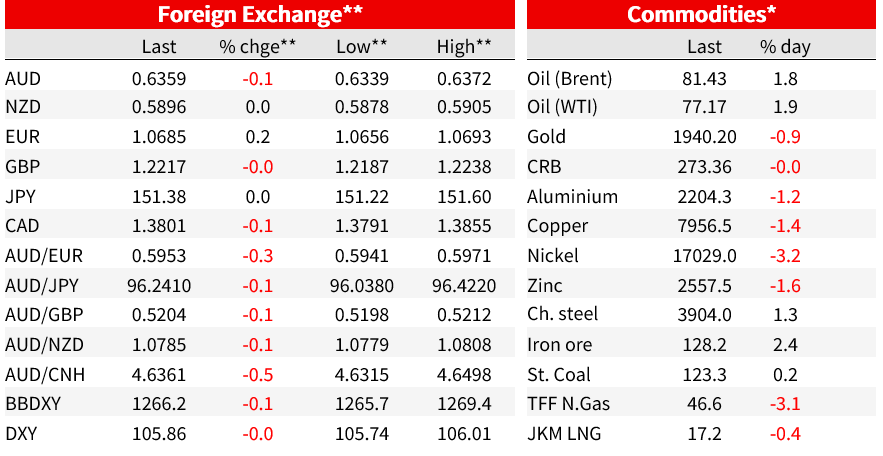

he USD had a softish end to the week with both DXY (-0.05%) and BBDXY (-0.15%) drifting lower on Friday. Nevertheless, it was a good week for the greenback, up ~0.8% on the week, its best weekly gain in close to two months .

In what was a quite session for G10 pairs, Friday’s standout performer was the Norwegian Krone following data that showed underlying inflation picked up for the first time in four months (NOK climbed ~ 1% to 11.1097/USD). The Norges Bank meets again on December 14 with the market now pricing a 73% chance for a 25bps hike (current cash rate is 4.25%).

USD/JPY rose for a fifth day on Friday, closing the week at 151.53 almost touching its vs year-to-date high of 151.68 reached on October 31. The recent move up in 10y UST yields has not helped JPY while the threat of intervention remains subdued. The euro climbed 0.2% to 1.0685 , trimming the weekly loss to 0.4%, meanwhile the pound was steady at 1.2226 after a four-day losing streak.

The AUD extended its decline on Friday, falling another 0.1% on the day to be down 2.3% on the week. The aussie was the worst G10 performing last week, not helped by the RBA which remains a reluctant hiker notwithstanding an upgrade to Australia’s inflation outlook . The Bank released its Statement on Monetary Policy (SoMP) on Friday outlining that further tightening to ensure inflation returns to target in reasonable timeframe will depend upon the data and the evolving assessment of risks. NAB retains the view that the data will force the RBA to hike again (25bps to 4.6%) in February. The kiwi was little changed on Friday, but down 1.78% over the past five trading days and now starts the new week at 0.5891, still broadly contained within a 0.58 to 0.60 range that has capture most of its price action since early October.

Looking at commodities, oil price gained on Friday (+1.8%), but on the week both WTI and Brent lost ground, down over 4% (WTI now at $77.35 while Brent is $81.70). Meanwhile, iron ore ($126.81) has continued its march higher, gaining 1.4% on Friday, up 3.15% on the week. Gold was another notable underperformer, down 1.47% on Friday and 3% on the week.

In other news, the US and China confirmed that Presidents Biden and Xi will meet this week on Wednesday in a bid to ease up the tensions between the two superpowers . The WSJ noted the Biden administration previewed a lengthy agenda including the Israel-Hamas war, North Korea and China’s backing of Russia during its war on Ukraine while China is also looking for assurances on Taiwan and an ease in American restrictions on technology transfers.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

US Fed – September cut but still see gradual easing

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.