NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

It’s just over six months since the COVID-19 pandemic was declared and we’re still unsure about how it will all end.

https://soundcloud.com/user-291029717/six-months-on-a-still-uncertain-future?in=user-291029717/sets/the-morning-call

“Lightning flash, tempers flare; ’round the horn if you dare; I just spent six months in a leaky boat; Lucky just to keep afloat”, Split Enz 1982

While the global economy feels like it has been “lucky to keep afloat” (to borrow lyrics from today’s headline act by the Split Enz), financial markets have been buoyed by a combination of unprecedented policy stimulus and high hopes of a vaccine by the end of the year.

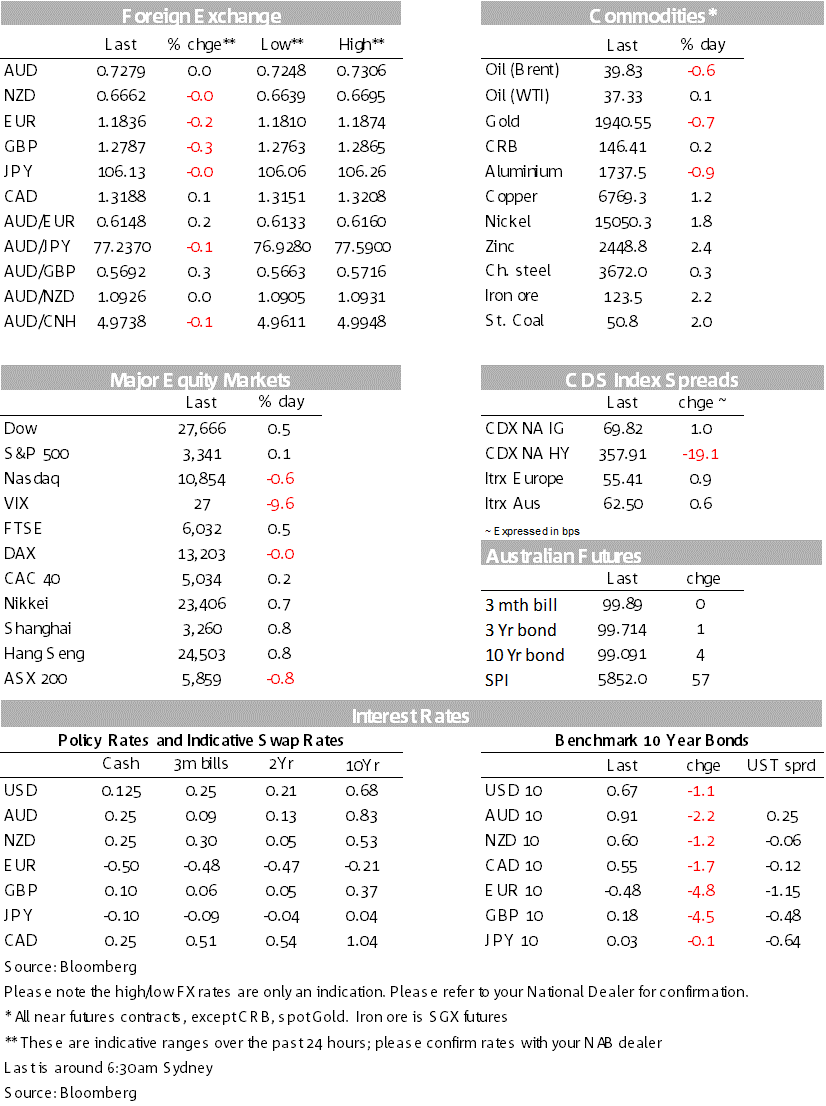

Since the pandemic announcement the S&P500 is up +21.8%, US 10yr yields are -20.4bps and the USD (DXY) is -3.3%.

Amongst commodities, iron ore is the clear outperformer up some +52%. The best performing G10 FX pair by far is the AUD at +11.9%, followed by SEK (+8.4%), NOK (+6.7%) and NZD (5.9%).

A wild ride indeed and which is likely to continue as phase 3 vaccine results starts to roll through over the coming weeks.

Equity markets were volatile, though the S&P500 closed marginally positive +0.1% to end the week still down -2.5%.

Focus remains on tech valuations with the tech-heavy NASDAQ down -0.6% and falling -4.1% over the past week. Trading strategies within the tech sector are under scrutiny with the FT and WSJ running articles on record call options trading and momentum strategies (see FT “How a retail options craze fuelled SoftBank’s ‘whale’ trade” and WSJ “The Wildly Popular Trades Behind the Market’s Swoon and Surge”).

Potential indicators of frothiness cited in these articles are that single stock and ETF option volumes are up 92% y/y, while small investors are reported to have bought call options with roughly a $500bn notional value in August, five times the previous monthly high for small investors reached back in early 2018.

Expect continued focus on tech this week, though risk sentiment overall may be boosted on weekend news that AstraZeneca would resume Phase 3 vaccine trials in the UK (see Stat for details).

FX was little moved on net the USD (DXY) slightly weaker at -0.1% at 93.33 with EUR -0.2% and USD/Yen -0.0%.

GBP was again the underperformer, -0.3% to 1.2787 as concerns over the lack of progress on a UK-EU trade deal rise and a possible “no deal Brexit” if the UK implements its internal markets bill. EU officials said the UK should amend its plans “in the shortest time possible and in any case by the end of the month”. The UK’s Michael Gove said the U “would not be withdrawing” the bill, while the EU has said it “will not be shy in using” all legal means if the UK went ahead with the bill in its current form. Note UK-EU trade negotiators resume their talks this week. Further negative headlines would weigh heavily with little air between 1.2787 and 1.25 according to the charts. UK GDP figures for July also suggests some slowing in momentum before the new 6-person gathering rule with growth of +6.6% m/m from 8.7% in June with the 3m/3m -7.6%.

Acting as a support to the Aussie continues to be strong signs of recovery in China with iron ore futures +2.2%, while aggregate financing figures for August were strong (3.6tn v. 2.6tn expected; note financing has averaged 3.2tn in 2020 so far) and suggests ongoing funding for planned infrastructure projects (the surprise was driven by bond issuance with new yuan loans broadly in line with expectations). Australia-China trade tensions have largely been ignored by FX markets with Australia’s largest export (iron ore) unaffected to date.

Though conditions are supportive of a further drift higher over the remainder of the year given the iron ore price and the policy divergence between the RBA and RBNZ where the RBNZ is seen to take rates into negative while the RBA has said such a move in Australia is “highly unlikely” – more on what the RBA is thinking will be in Tuesday’s Minutes (see below for details).

Other data out on Friday will likely re-ignite the debate around inflation with US CPI coming in hotter than expected. August Core CPI was +0.4% m/m against 0.2% expected. The y/y figure has creeped up to 1.7%, while the 3m annualised has jumped to 2.4%.

Inflation was driven by a sharp rise in used car prices (+5.4%) with strong demand amid reluctance to use public transport, as well as the income hit meaning more activity in the used car market (as opposed to new).

There was limited market impact from the print with US Treasury yields declining slightly with the 10yr yield falling 1.1bps to 0.67%. Even though not market moving, an alternative measure of core inflation in the US, the Cleveland Fed’s 16% Trimmed Mean Measure has been relatively steady during the pandemic at 2.2-2.5% and suggests most of the moves seen in the official measures of CPI have been relative price effects which are now starting to wash out of the system. It is possible that US inflation did not fall by all that much during the pandemic.

A day after the ECB meeting, at which President Lagarde suggested that the ECB would not overreact to the appreciation in the EUR exchange rate, Chief Economist Philip Lane took a firmer line in a blog post. Lane said that the ECB’s forecasts of core inflation would have been revised up by more had it not been for the appreciation in the EUR (which “significantly muted” the upward revision), adding that “it should be abundantly clear that there is no room for complacency ”. The EUR rose following the remarks, though the comments only had a short-term effect on the currency. Germany’s 10-year bund yield fell 5bps to -0.48%, although this was mainly a catch-up move to the rally in US Treasuries after the European close on Thursday night.

A busy week domestically with the RBA Minutes on Tuesday and Employment/Unemployment on Thursday. The Minutes of the September meeting will incorporate more details around the decision to extend the term funding facility and whether the Board is mulling further policy easing as was hinted in the post-meeting Statement (“continues to consider how further monetary measures could support the recovery” see link). The RBA’s Head of domestic markets also speaks Thursday, but is unlikely to be policy focused.

Employment on Thursday should show the impact of Victoria’s lockdown with weekly payrolls data suggesting a -40k decline in employment (also the consensus). We expect the unemployment rate to rise to 7.8% from 7.5% (consensus), though with the usual caveats around the participation rate. There will also likely to be further talk around Victoria’s re-opening thresholds with business leaders again stating thresholds are too high.

New virus cases continue to trend lower with the 7-day moving average at 46 cases and the important 14-day moving average used as part of the re-opening plan set to dip below 50 by mid-week and thereby fulfilling the second-stage re-opening benchmark (note second-stage re-opening is pencilled in for September 28 if average daily cases in metro Melbourne are 30-50 over a 14 day period (see link). Note the 7-day moving average is currently halving every 11 days.

It’s a central bank focused week with the FOMC on Wednesday (4.00am Thursday AEST), and the BoJ and the BoE on Thursday.

All eyes will be on the Fed where markets will be looking for Chair Powell to elaborate on the already announced shift to average inflation targeting (“we will seek to achieve inflation that averages 2% over time. Therefore, following periods when inflation has been running below 2%, appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time…we are not tying ourselves to a particular mathematical formula that defines the average…viewed as a flexible form of average inflation targeting” seek link).

The Fed is set to be less pre-emptive in tightening policy than in the past, or as Governor Brainard recently put it “this change implies that the Committee effectively will set monetary policy to minimize the welfare costs of shortfalls of employment from its maximum and not preemptively withdraw support based on a historically steeper Phillips curve that is not currently in evidence and inflation that is correspondingly much less likely to materialize” (see link).

But possibly hint at the potential for future easing. The UK-EU stand-off over a new trade deal will also continued to be watched closely with GBP increasingly at risk as investors ponder another “no deal” possibility.

The key pieces are China’s Monthly Activity Indicators on Tuesday with focus on retail given the lacklustre bounce to date, while industrial activity should remain strong. Keeping with the retail theme, US Retail Sales on Wednesday will also be closely watched for the impact of the tapering of the unemployment benefit supplement ($600 a week supplement expired on July 31 and was replaced by Trump’s $300 a week Executive Order) with a wide consensus for the core control measure of -0.9% to +3.4% m/m. US Jobless Claims will provide another update on the pace of recovery. Also Thursday is NZ Q1 GDP with our BNZ colleagues pencilling in a 14.2% fall and there is also a pre-election fiscal update.

A quiet day domestically with little on the radar. Across the ditch NZ has its Performance of Services Index. Asia’s focus will be on the election of Japan’s new PM (done in a party room vote; similar to Australia), while Europe has Industrial Production figures. There is no data scheduled for the US:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.