We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Mixed US data and hawkish take on Fed Clarida shake markets. ADP is a big miss, US ISM a big hit.

https://soundcloud.com/user-291029717/jobs-boost-for-nz-whilst-us-jobs-fails-to-pick-up?in=user-291029717/sets/the-morning-call

Mixed US data releases and hawkish take on Fed Clarida’s comments were the shakermakers to a volatile overnight session. The 10y UST notes traded in a 1.1258% to 1.2136% range with the overnight low printed after a big miss by the ADP report while the overnight high came on the back of a solid ISM Services release and upbeat comments from Fed vice-chair Clarida. US stocks ended the day mixed while European equities closed at a record high for a third day in a row. The USD is slightly stronger with NZD the outperformers while in commodity land, oil prices continue to slide as US inventories rise.

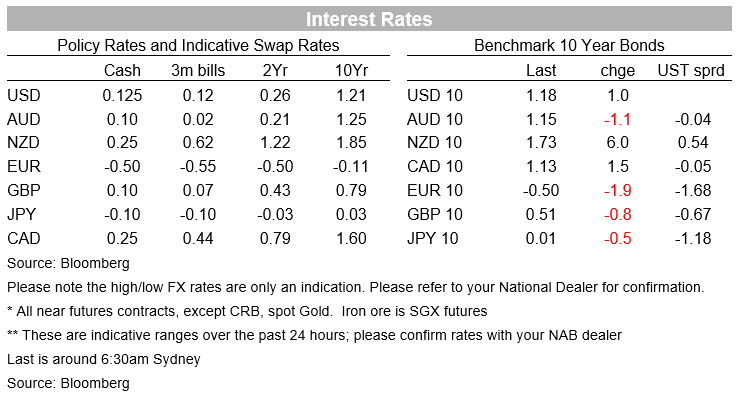

10y UST yields endured a volatile overnight session only to end the day little changed at 1.18%. Early in the overnight session the benchmark yield traded to a low of 1.1258% following a big ADP miss. ADP private payrolls rose by just 330k against expectation for a 690k rise, the smallest gain since February . While not always a reliable guide to nonfarm payrolls, the ADP report inevitably will have many questioning the consensus for a private payrolls print of 718k on Friday. Cautious remarks by ADP’s chief economist, Nela Richardson, didn’t help sentiment either, noting that the July report was a marked a “slowdown from the second quarter pace in jobs growth” with ““Bottlenecks in hiring continue to hold back stronger gains, particularly in light of new Covid-19 concerns tied to viral variants.”

The move lower in 10y UST yields didn’t last long, just under two hours later a very strong US ISM services report along with upbeat comments from Fed vice-chair Clarida combined to propel the 10y tenor by almost 10bps, reaching an overnight high of 1.2136%. The ISM services index rose to a record high of 64.1, well above expectations, with a 7-point gain in business activity and more moderate gains in new orders and employment, the latter up from 49.3 to 53.8. So, in line with the manufacturing ISM, both employment indices are now back in expansionary mode. As for the survey respondents’ themes high demand and supply chain disruptions featured prominently, as did higher costs for materials and labour.

Speaking at the same time the ISM release, Fed vice Chair Clarida said that if his baseline is right, he would support a reduction in asset purchases later this year. Similar to Fed Chair Powell, Clarida didn’t provide a specific timeline but his expectations of achieving ‘substantial further progress’ “over the coming meetings.” suggest a tapering announcement is more likely in November at the earliest rather than September (next FOMC meetings are 22 Sep, 3 Nov. and then 15 Dec). Importantly too, Fed Clarida said that based on his outlook for inflation and employment then the “necessary conditions for raising the target range for the federal funds rate will have been met by year-end 2022”, cementing in market expectations that the Fed Funds rate would likely rise from early 2023. So at least in Clarida’s mind there is a clear window of about a year between tapering commencing and the fist funds rate hike. Clarida also remarked that there are risks to any outlook, and I believe that the risks to my outlook for inflation are to the upside”.

Looking at the UST curve while the 10y tenor ended the day little changed at 1.18%, there was a distinct curve flattening theme with both the 2y and 5y up 1bp and 3bps respectively while the 30y Bond eased 0.5bps to 1.84%.

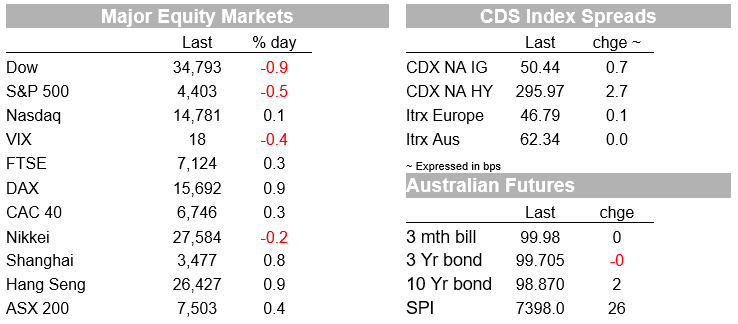

The S&P 500 futures followed a similar trading pattern to the moves in 10y UST yields , trading down to a low of 4365 on the back of the ADP report (down 0.65% with physical market closed at the time), jumping around 1.19% on the ISM release and then easing back into negative territory in the aftermath of Fed Clarida’s comment. The S&P 500 ended the day down 0.46%, the Dow was -0.92% and the NASDAQ +0.13%. Meanwhile in European equities had another decent day aided by a rebound in corporate profit, the Stoxx Europe 600 Index gains 0.6%, closing at a new record high for the third day in a row.

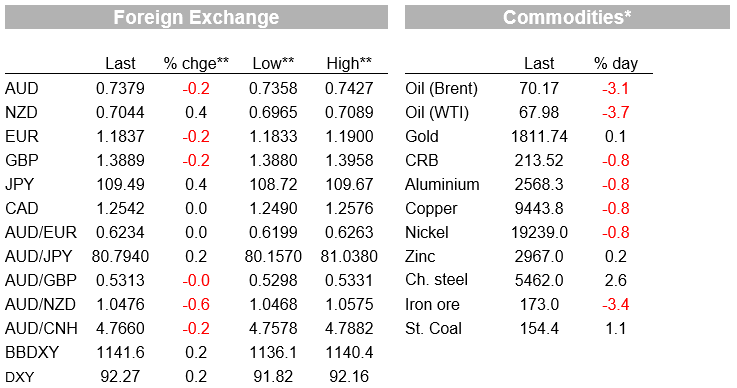

In currency markets the USD was on the soft side until the strong ISM services print and Clarida’s remarks got the market’s attention and sent it higher. Net movements have been small and the BBDXY index is up just 0.2% for the day. NZD has been the notable G10 performer , the only pair that managed to record gains against the USD over the past 24 hours, up 0.44% and currently trading at 0.7048.

Yesterday the AUD traded with a positive tone with momentum still evident in the early part of the overnight session. The pair managed to climb above the 0.7415 resistance area printing an overnight high of 0.7427 following the ADP print miss. AUD bulls were disappointed shortly after as the ISM/Clarida combo gave the USD a broad boost taking the AUD back down to 0.7380 area where it currently trades. The AUD needs a weekly closed above the 0.7415 resistance area for traders to become a bit more positive on the pair’s near term outlook. Non-farm payrolls and US employment data in general is potentially a big swing factor.

Moving onto the commodity market. Steam Coal and Iron ore managed small gains of around 1% while oil prices fell over 3% with an increase in US inventories not helping the mood. Overnight the US Energy Information Administration (EIA) said US crude oil inventories increased by 3.6 mb during the week ending July 30, this against expectations for a decline of about 4mb.

In COVID19 news overnight, Israel, which has led the world with its vaccination programme, has seen new daily cases surge to over 3000 and has reimposed some restrictions to contain the spread. These include outdoor mask use for large groups and sending half of public servants home.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.