Coming in for landing in a heavy cross wind

Insight

The main news overnight is the US decision to release 1m barrels a day for 6 months from their strategic petroleum reserve

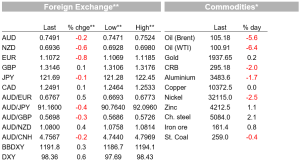

It was a fairly quiet night overnight outside energy markets, topping off what was a much more eventful quarter. The main news of note is the US decision to release 1m barrels a day for 6 months from their strategic petroleum reserve. That helped Brent oil down 5.6% to US$105.18/bbl. Earlier, Chinese official PMIs came in on the softer side, setting a modest risk off tone.

Equities were lower, the S&P500 down 1.4%, much of that in the last hour or so, to end the quarter with its first quarterly loss in 2 years. Financials led declines in the session, while some tech stocks were also under pressure. AMD, HP and Dell each down more than 5%. Despite a rally in the second half of March, the S&P 500 ends the quarter down around 4.7%, with the Nasdaq 9.1% lower. European bourses were also lower yesterday. The DAX off 1.3% and Euro Stoxx 50 losing 1.4%.

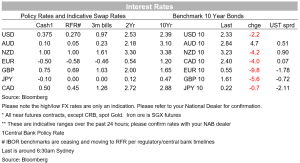

In currency markets, the modest risk-off tone was evident. The DXY was up 0.6% to 98.36. The yen holding against the stronger dollar, USD/JPY losing 0.1% to 121.69. AUD continued to oscillate around 75c. The aussie 0.2% lower to sit at 0.7491, having slid as low as 0.7471 following the weaker Chinese PMIs. The euro fell 0.8% to 1.1072 as European yields fell. Yields were generally lower. The US 10yr yield was off 2bps to 2.33%. The 2s10s spread was still flirting with inversion. The 2yr yield was also down slightly to 2.29%. Over the quarter, according to the Bloomberg treasury total return index, treasuries are on track for their worst quarter since the index began in 1974.

The ECB’s Lane spoke in Paris overnight. He sounded less at ease about the inflation outlook saying that “We should ensure that our policy settings are adjusted if de-anchored inflation expectations, an intensification in catch up wage dynamics or a persistent deterioration in supply capacity threaten to keep inflation above target in the medium term. ” But highlighted the risk is two way, pointing to the risk of a deterioration in macroeconomic prospects to medium-term inflation. European inflation overnight out of France and Italy didn’t deliver the same upside surprise as the Spanish and German numbers yesterday. The Eurozone number prints tonight.

Reports that the US would release 1 million barrels per day of oil began during Asia yesterday, and were later confirmed overnight by US President Biden. The release of up to 180m barrels is set to begin in May. A US official said that “These barrels will be a wartime bridge to additional U.S. production. ” The release would leave U.S. government reserves at their lowest level since 1984. As of last week they sat at 568 million barrels, down from a peak of roughly 700 million, according to the EIA. Biden also indicated that he wants oil producers to pay penalties for unused federal leases to promote US production. Meanwhile, OPEC+ decided to stick to its plan for gradual output increases for May. That’s in a meeting that lasted just 12 minutes. WTI was back towards U$100/bbl, down 6.4%. Brent fell 5.6%.

Natural gas was volatile amid uncertainty about the impact of new payment terms from Russia. French officials said Thursday the new mechanism doesn’t change payments as mandated in supply deals, which will continue as before, but Russia has indicated that new terms that require payment in roubles via accounts in Gazprombank would be in force from Friday.

On the data front, US PCE core deflator came in in line with expectations at 0.4% m/m, the y/y rate at 5.3% y/y (vs 5.4% expected). Personal spending disappointed, up just 0.2% m/m and -0.4% in real terms, but that’s from an upwardly revised January number. Initial jobless claims came in at 202k against 196k expected.

Chinese PMIs yesterday disappointed, driven by a sharp fall in the services PMI amid the latest virus surge. The Services Index dove to 46.7 from 50.5 (a lift in the construction PMI offset some of that weakness in the non-manufacturing PMI). Manufacturing was a bit more resilient, but still fell to a 5-month low of 49.5 from 50.2, weighed by supply chain pressure and quarantine requirements. Japan’s February industrial production numbers also disappointed, rising just 0.1% m/m against 0.5% expected.

In contrast, domestic data yesterday was strong. Job Vacancies rose 6.9% in the 3 months to February to 423.5k. Vacancies are now 86% higher than pre-pandemic levels. We continue to expect the unemployment rate to fall below 4% as soon as the March data released on 14 April, comfortably outpacing the RBA’s February forecasts for the unemployment rate to drift below 4% in the third quarter. Residential building approvals recovered their January decline, up 43.5% m/m in February. The flow of new approvals remains above pre-pandemic levels at a time when capacity constraints are binding, construction pipelines are full, and homebuilding costs are supporting inflation.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.