Uncertainty remains high ahead of July reciprocal tariffs

Insight

The Morning Call is back, and the new year has kicked off pretty much where we left off.

https://soundcloud.com/user-291029717/a-blue-wave-into-2021?in=user-291029717/sets/the-morning-call

‘Rise above 1’ is the lead single from the Bono and The Edge penned Broadway show Spider-Man: Turn Off the Dark, performed by Reeve Carney, who stars in the musical as Peter Parker/Spider-Man.

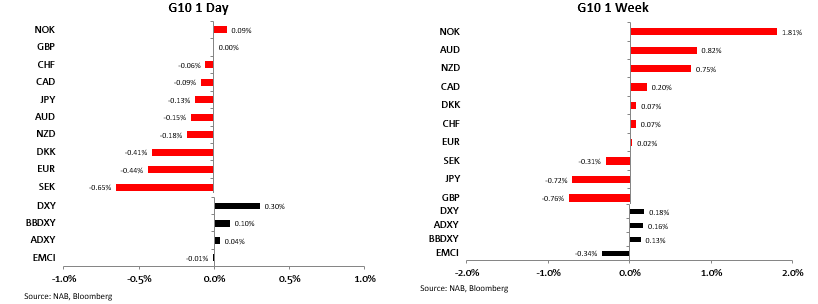

For those returning today from an extended break, the biggest market news, which followed the success of both Democrat candidates in the Georgia Senate election run-offs, has been the sharp rise in 10-year Treasury yields, to above 1% last Wednesday in the immediate aftermath of the results and extending their rise to 1.115% on Friday. The was after the 140,000 reported decline in US non-farm payrolls amplified existing expectations for additional fiscal stimulus in the early days of the new US administration, hopes further fuelled by comments from President-elect Joe Biden on Friday saying he will lay out new proposals on Thursday with a price tag in the ‘trillions’. This ~20bps rise in 10-year yields since the start of year in turn has some currency observers questioning the bearish USD narrative, in which respect the BBDXY and DXY USD indices both ended Friday about 1% above their intra-week lows. AUD ended the week at 0.7760 after making a new cycle high of 0.7820 last Wednesday, when the USD was at its weakest.

Post the 140,000 reported drop in non-farm payrolls, said that this coming Thursday he will lay out proposals for new fiscal support, including boosting stimulus cheques to $2,000, saying “the price tag will be high…it will be in the trillions of dollars”. The 50-50 partisan split in the Senate promises to make such an ambitious proposal challenging to pass, in which respect moderate (or ‘conservative) Democrat Senator Joe Manchin, who promises to have much influence over the ability of Democrats to pass legislation without the need for support from Republican Senators, said Friday that if there is to be another round of direct payments to individuals, it “should be targeted to those who need it.” An earlier report said he flat-out opposed boosting stimulus checks from the $600 approved in a December Covid-19 relief package, prompting an intra-day reversal in stock prices, before recovering after Bloomberg News reported that Manchin planned to review Biden’s proposals and extended gains following Biden’s comments. These fluctuations exemplify investor sensitivity to news about the next fiscal initiative which will undoubtedly be a dominant early-year market theme.

We have witnessed quite a contrast with the way they performed in the days leading up to the 3 November US election when the ‘blue wave’ was looking like the singularly most likely outcome and market were fretting about the implications of this with regard to higher corporate and other taxes and well as tighter regulation impacting a swathe of equity sectors. Now the potential positives of stronger fiscal support for the economy are dominating, in part on the view that the priority of the incoming US administration on getting the pandemic under control and stabilising the economy will be taking priory over these other issue for some time to come. One reason to be caution here is that, under the so called Byrd Rule that clients will have received a note on last week, higher taxes may be one price to be paid for higher government spending in order to side step the ability of Republican Senator to filibuster Democrat-instigated sending plans.

What was also evident in the stock market last week was the extraordinary and ugly scene in Washington and now the suggestion that a second impeachment of President Trump is in prospect, made scant impression. Latest here is that while impeachment proceedings could be initiated as early as Monday or Tuesday, House majority whip James Clayburn has been out suggesting that this could wait until after President -elect Joe Biden’s inauguration, and possibly not before his first 100 days in office (Biden himself on Friday inferred that impeachment was not a live issue for him).

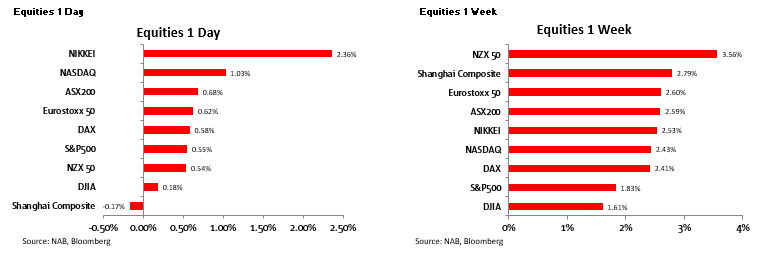

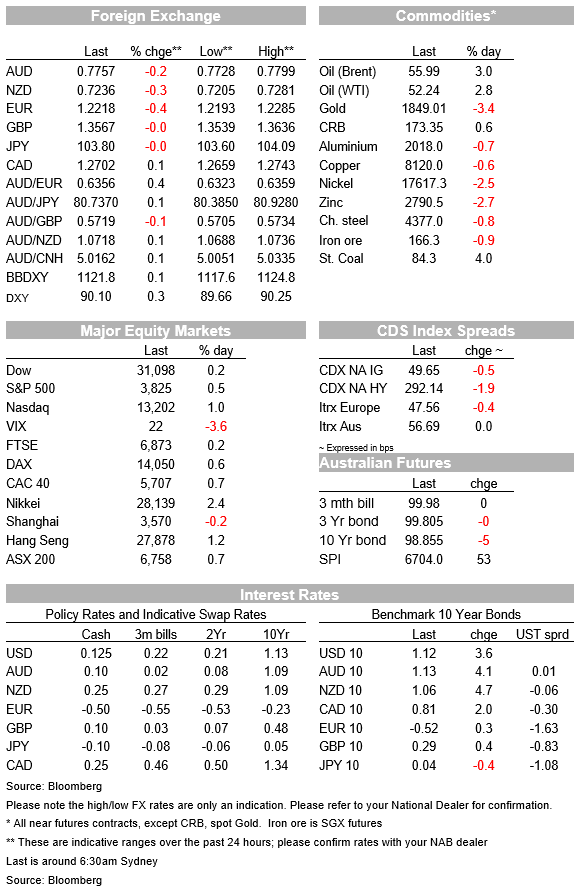

Currency markets have seen less volatility than in bonds (see below) but where the first week of the year has proved to a proverbial game of two halves. The USD continued to slide in the first half of the week and ahead of the Georgia Senator elections, picking up from here it left off at the end of 2020 and making new cycle lows on Wednesday, before staging a recovery on Thursday and Friday that resulted in both the narrow DXY and broader BBDXY indices rising about 1% off their mid-week lows. This included the AUD dropping back from a new post April 2018 high of 0.7820 to around 0.7760 as of Fridays New York close. This still leave it about 0.8% up YTD, having ended 2020 almost bang on 0.7700. The virus news over the Xmas New Year period, including the scare regarding the single new variant outbreak in Brisbane resulting in a three day lockdown of the Greater Brisbane area – representing almost 10% of the Australian economy – has made scant impression on markets. Commodity prices have continued to be a tailwind for AUD, e.g. the LMEX index of industrial (non-Ferrous) metals is up nearly 4% so far this year, and WTI crude some 7.5% or $3.70 (this after Saudi Arabia last week agreed a 1 million barrels per day unilateral supply cut for February and March).

USD/JPY has been a major beneficiary of the rise in US yields thus far in 2021, while GBP has been an under-performer on a combination of a ‘sell the news’ (so far) response to the post-Brexit trade deal and the acceleration of the spread of COVID in the UK where daily new cases are running consistently above 50,000.

Of the 20bps rise in 10-year Treasuries last week, about half of the rise is accounted for by a rise in market-based inflation expectations (10-year break-evens up from just under 2% to about 2.08%). Most of the rise in nominals only came from Thursday onwards our time, once the Georgia Senate election result was known and markets then started ping in stronger fiscal stimulus and its supply implications, with more confidence. 10-year Australian equivalent yields rose by about 10bps, so too UK gilts, while benchmark German Bunds lifted by only about 5bps.

The main central bank comment on Friday and relevant to bond markets was from Fed Federal Reserve Vice Chairman Richard Clarida who said his economic outlook is consistent with The Fed keeping the current pace of purchases throughout the rest of this year, adding that he sees no reason now to revisit how the Fed is going about those purchases (i.e. not supportive of lengthening the maturity of purchase, in which resect last week’s FOMC minutes showed only a couple of members expressing support for this). As an aside Clarida also notes that the USD was currently not much below its average of the past years – no once about USD weakness there.

US non-farm payrolls fell by 140,—, well below the 50k rise expected, the decline led by a 498k loss of jobs in leisure and hospitality. The unemployment rate help at 6.7% against an expected rise to 6.8% amid an unchanged 61.8% participation rate. Average hourly earnings jumped by 0.8% for a 5.1% annual rise up from 4.5% in November, but this is not mix-adjusted and reflects the fact job loses re concentrated among lower paid workers

Employment in Canada fell by a larger than expected 62.6k (37.5k expected) with unemployment up to 8.6% from 8.5%. German November exports and industrial production, and French manufacturing production, all came in stronger than expected indicating the industrial side of the Eurozone economy holding up into December but since when more stringent lock-downs have come into effect.

It’s not a big week ahead on the data front and in any event ‘last year’s data will be on limited interest to markets. Events in Washington should dominate and where Joe Biden is to outline his fiscal ambitions on Thursday. More real time indicators of the impact COVID related restrictions in various countries – and the sped of roll-out of vaccines – will likely be of more interest than official and so more backward looking indicators. Today sees final Australian November retail sales, that jumped 7% in the preliminary read after Melbourne’s lockdown ended on October 28. China CPI and PPI will rate a mention, where CPI is seen returning to zero from -0.5% in November, and PPI to a less negative 0.8% from -1.5%.

Highlights such as they are of official statistics during the course of the week include US CPI on Wednesday, China trade on Thursday and US retail sales, industrial production and consumer sentiment on Friday. The US Q4 earning season kicks off on Friday with some of the big banks reporting.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Uncertainty remains high ahead of July reciprocal tariffs

Insight

Australian carbon project developers see a maturing of institutional financing as key to scaling the market and taking it on a similar trajectory as renewable energy.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.