NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There’s still an outside chance that in January the Democrats could take control of the Senate.

https://soundcloud.com/user-291029717/a-blue-wave-is-still-possible-but-two-months-of-no?in=user-291029717/sets/the-morning-call

Overview: We have a winner

Biden gaining 290 electoral college votes to Trump’s 214 (270 needed for victory). This result was largely expected by markets who had been trading with the view of a Biden Presidency and a Republican Senate late last week. This combination of course likely means a Biden Presidency’s ambitions will be curtailed in a grid-locked political scene with very few landmark legislative changes being enacted by Congress. Nevertheless, that also means less likelihood of regulatory changes (particularly favourable for tech) and tax changes which can be bullish for stocks – equities clearly heard that message last week with the S&P500 up 7.3% and the best gains in an election week since 1932! A fiscal stimulus plan in that environment can still be achieved, but ambitions of a further fiscal ramp are less likely which puts the focus back on the US Fed to bolster the economy.

Two run-offs in Georgia still gives the Democrats a very narrow path to a workable majority with Harris as VP. The Senate count is currently 48 v 48 with four left. Of those, Georgia’s two Senate races will go to runoff on January 5 since neither contender has achieved 50% of the vote. Betting markets are so far are discounting the possibility of the Democrats winning these races (PredictIT gives it 25c v. 75c for Republicans). That discounting coming as Republican candidates got more votes than Democrats in the two races so far: Perdue-Ossoff ( Republican Perdue got 49.8% v. Democratic Ossoff at 47.9%); Warnock-Loeffler (Democrat Warnock 32.9%, Republican Loeffler 25.9%, but total Democratic candidates received 41.8% v. Republican candidates of 49.3%). Nevertheless, Georgia has a whole looks like it voted for Biden (Biden 49.5% v. Trump 49.3%) so it is still within the realms of possibility that the Democrats could win both Senate races and gain a workable Senate majority.

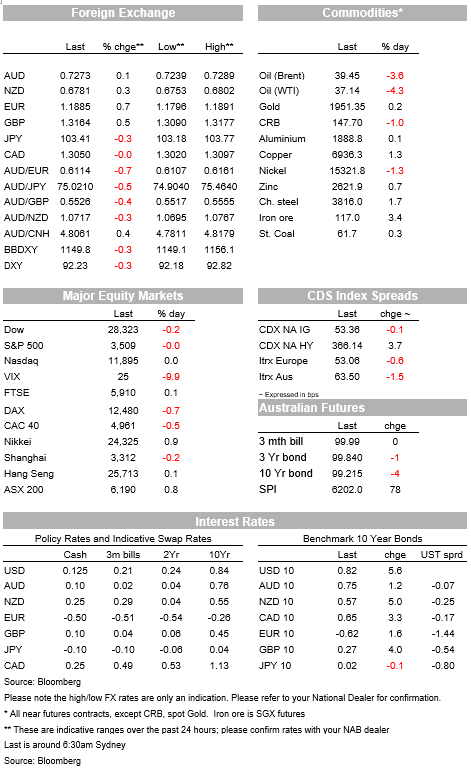

USD continues to weaken in this environment with BBDY down -0.3% on Friday to be around the weakest levels since May 2018. Global growth proxies continue to outperform, a Biden Presidency likely less confrontational on trade and more likely to use multilateral institutions and approaches to deal with trade issues. The AUD is up some 3.3% on the week, likewise the NZD is up 2.4%. The prospect of a less hostile Biden administration with China saw the CNH rise 1.6% on the week, adding further support to the NZD and AUD.

GBP and EUR are likely to be under focus this week with UK-EU trade negotiations coming to ahead with the EU Summit on November 15. Weekend press report UK PM Johnson and EU Commission President von der Leyen spoke by phone with both sides highlighting that there were still large differences to overcome on the thorny issues of state aid and fishing rights. To date GBP hasn’t been affected much by the coming deadline as yet, with markets still sensing a deal…eventually.

It was all about US Payrolls on Friday. Payrolls beat expectations, sending yield higher, but also reducing the likelihood of a fiscal package in the lame duck session. Headline Payrolls were strong at 638k v. 580k expected and at a similar pace to last month’s 672k. Unemployment also fell a full percentage point to 6.9% from 7.9%, albeit with the caveat that the household survey tends to be more volatile than the payrolls survey. A good set of numbers for sure, but with two important implications: (1) better numbers makes an agreement on a fiscal package less likely during the lame duck session– White House economics adviser Kudlow was out saying the Trump administration now opposes a $2trn package in the wake of the numbers; and (2) the numbers are likely to be dated given the resurgence in virus numbers and higher frequency data showing consumers are self-isolating even where restrictions have not been tightened greatly.

Yields nonetheless rose after the payrolls report, with the 10-year yield up 5.6bps to 0.82 %. Over the past week 10yr yields reached a peak of 0.94% on heightened expectations of Democrats gaining a Senate majority, only to completely unwind with yields down by around 5bps on the week as expectations of a fiscal ramp unwound. The unwinding of those expectations largely came on the back of reversing curve steeper positions, which put downward pressure on US longer-term yield (US 30yr peaked at 1.75% and is now 1.60%). The near-term upside in yields is likely capped unless the Democrats were to gain a workable Senate majority on January 5 (see above for details).

The RBA’s SoMP on Friday again pushed back on negative rates (“The Board is not contemplating a further reduction in interest rates”; “view a negative policy rate as extraordinary unlikely”). As such the focus for policy will be the RBA’s QE program and “the Board is prepared to do more and undertake additional purchases [if circumstance require] ”. Further stimulus may well be needed with forecast core trimmed mean inflation still well below target at 1½% by the end of 2022. Worryingly on the risks to inflation, the RBA’s Business Liaison notes that around 25% of surveyed firms intend to implement wage freezes in the year ahead, while 30% already have wage freezes in place. There is an obvious risk that the widespread imposition of wage freezes and continued labour market slack (as forecast) could embed “a norm for wage increases that is below 2%”.

Finally, Chinese trade numbers beat expectations which should set up the week with a positive tone. Exports rose 11.4% y/y v. 9.2% expected with the headline trade balance lifting to $58.4bn v. $46.3bn. Imports though underwhelmed at 4.7% y/y against 8.6% expected.

Domestically a quiet week with only the NAB Business Survey and two measures of consumer confidence of note. Across the Ditch the RBNZ meets on Wednesday where consensus is for on hold ahead of negative rates negative rates in 2021. Instead the RBNZ is likely to unveil details of its planned Funding for Lending Program, which will allow banks to fund from the RBNZ at rates near the cash rate.

In Europe the heads of heads of the ECB, BoE and US Fed speak at an online ECB Forum on Thursday, titled “Central Banks in a Shifting World”. UK-EU trade negotiations are also set to come to their crux with the next EU Summit on the 19th. Elsewhere it is relatively quiet outside of Europe with only Chinese Aggregate Financing figures (due anytime in the week) and the US CPI on Thursday of note.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.