Coming in for landing in a heavy cross wind

Insight

After a fairly volatile week markets were calmer on Friday on the back of positive retail numbers from the US.

https://soundcloud.com/user-291029717/a-calm-friday-but-it-could-be-a-volatile-week?in=user-291029717/sets/the-morning-call

You got me hoping and wishing, That this could last for one more night

Let’s go high, Let’s go higher (let’s go higher) – Jordan Knight

Equity markets rebounded in Europe, the S&P 500 flatlined and the NASDAQ recorded its fourth consecutive day of decline notwithstanding solid US retail sales figures and a buoyant consumer confidence reading. Moves in FX were also subdued, GBP was volatile as PM Johnson threatened to walk away from UK-EU trade talks, but negotiators are still expected to continue talking on Monday.US House Speaker Pelosi sets a Tuesday deadline on White House stimulus negotiations, President Trump is willing to higher , but Senate Republicans remain opposed to a big package. NZD trades little changed at the open, following Labour’s majority election win.

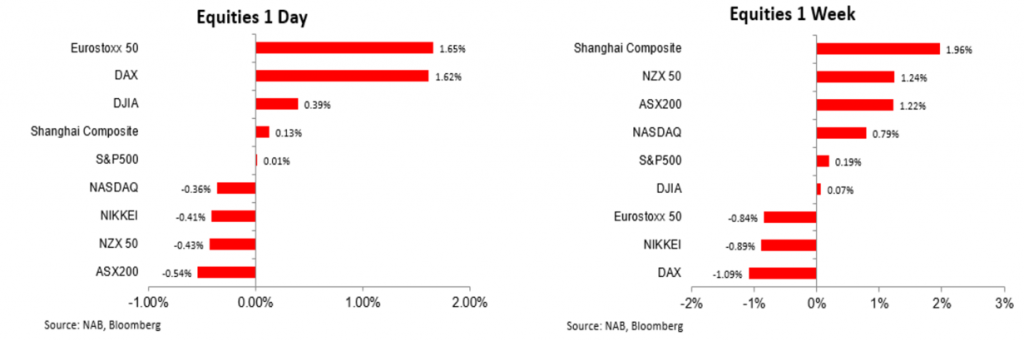

European equities were the big movers on Friday, rebounding from their sharp declines on Thursday. The Stoxx 600 Index ended 1.3% higher with company specific news driving the gains, LVMH shares jumped 7.3% amid solid demand for Louis Vuitton goods in the third quarter. Daimler AG rose 5.5% after profit beat estimates. Meanwhile the S&P 500 closed Friday almost exactly where it started the day, ending a three day losing streak. The NASDAQ was not that fortunate, recording it’s fourth consecutive day of declines, down 0.4%. Looking at the week, in spite of the improvement on Friday, European equities ended lower over the five days and main US equity indices still managed to record gains for the week. The S&P 500 and the NASDAQ continue to hover just below their respective all-time highs, supported by low interest rates and growing conviction that Biden will win decisively at the US election and the Democrats will implement a huge fiscal stimulus. Chinese equities were the big performers on the week with the Shanghai Composite up almost 2%.

Retails sales in September was a blockbuster, headline sales rose 1.9%, more than double the consensus 0.8% rise. Aside from the wild monthly gyrations in the initial months of the pandemic, this is the largest monthly rise since September 2017. The core measure was also impressive at +1.5% vs. 0.5% expected and importantly too, details of the report revealed broad based gains across categories. Economists continue to question the durability of the rebound in retail spending in the absence of more fiscal support and, in particular, enhanced unemployment benefits. US equities made their highs for the day shortly after the US retail sales release but faded in the last hour of trading. The University of Michigan measure of consumer sentiment edged up in early October, although it remains well below its long-run average and somewhat putting a damper on proceedings, Industrial production fell 0.6%, below the consensus, +0.5%

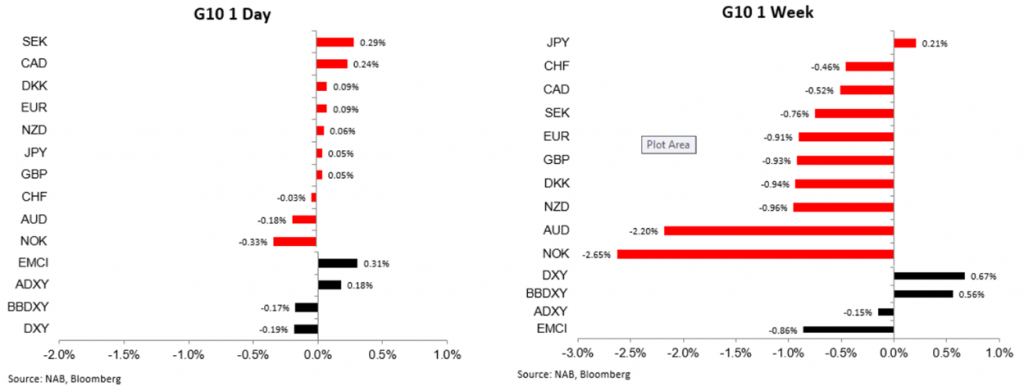

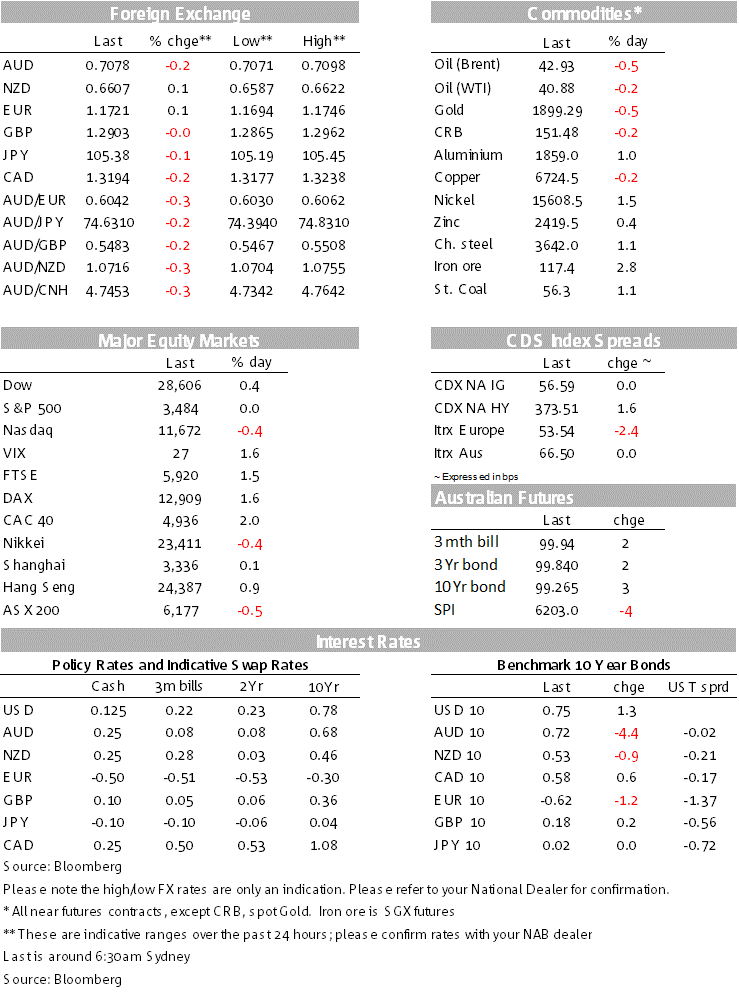

CAD and SEK made some gains against the USD up 0.24% and 0.29% respectively while AUD and NOK edged a little bit lower. Over the whole of Friday the AUD fell 0.18%, but relative to Friday’s Sydney closing levels the AUD was essentially unchanged, ending the week at 0.7077 and now it starts the new week at 0.7082. GBP had a volatile session Friday night, falling one big figure to a low of 1.2865 as UK PM Johnson threatened to walk away from UK-EU trade negotiations. Later in the session it was confirmed EU’s chief negotiator, Michel Barnier, will travel to London for talks with his counterpart, David Frost, on Monday. Michael Gove, the UK Brexit minister, said on Sunday that the UK is “increasingly well-prepared” for a no-deal Brexit and this morning Bloomberg reports the UK is prepared to water down Boris Johnson’s controversial lawbreaking Brexit legislation in a move revive negotiations with Europe. The pound now trades at 1.2903.

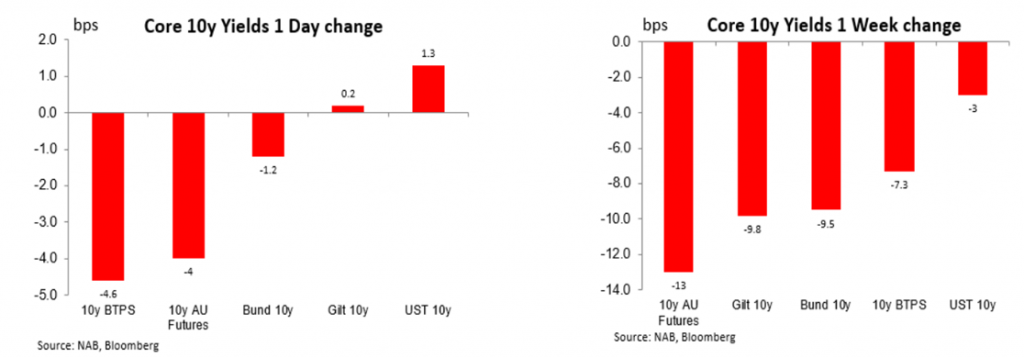

On the week the AUD along with NOK are the notable underperformers, down 2.20% and 2.65% respectively while the USD made broad gains (BBDXY up 0.56% on the week) with JPY, the only pair to outperform the USD ( up 0.21%). Prospect of further RBA easing has been the main catalysts for the AUD underperformance. The market is building-in a greater chance that the RBA will enact a volume-based bond buying programme, in the 5-10 year sector of the curve, as soon as next month. Indeed looking at 10y AU bond futures, they were the big performers on the week (down 13bps in yield terms on the week and opening the new week at 99.265 – see chart below).

The NZD was quiet on Friday, contained to a very narrow 0.6587 – 0.6619 trading range. As expected Labour won an outright majority in the NZ general election over the weekend in a landslide result. NZD has opened the new week little changed at 0.6606.

Negotiations between the White House and Democrats on a pre-election fiscal stimulus package continued over the weekend, with Democrat Pelosi putting a Tuesday deadline to get a deal agreed. Speaking over the weekend President Trump said he was prepared to go higher than the $1.8trn his team had been trying to offer Pelosi. Calling in to a Wisconsin TV station on Saturday, Trump said he could exceed the amounts floated so far and voiced confidence that he “could quickly convince” Republicans to back a “good” deal. The problem is that even if the White House reaches an agreement with the Democrats, Senate Republican remain opposed to a big package.

On Saturday the US added 57,164 new cases, the fifth consecutive day of infections over 50,000. The weekly change in new cases has reached new highs in France, Italy and the UK, among other countries, over recent days and governments in the region are implementing new restrictions. The UK and France implemented new restrictions over the weekend and now Italy is said to be considering new restrictions. Health care services are coming under increasing pressure. Governments have been reluctant to implement broad-based lockdowns, like those implemented earlier this year, but with the WHO warning that ICUs in some European cities will probably reach full capacity in the weeks ahead, the risk is that restrictions are tightened further.

Unlike what we are seeing in European equity markets, EU core global bond yields are reflecting a more cautious view on the outlook. The German 10-year yield fell 1bp on Friday and 10bps on the week to -0.62%, its lowest level since March and 10y Gilts fell by a similar amount over the week, ending at 0.182% on Friday. US Treasury yields were slightly higher on Friday and little changed on the week (US 10-year: 0.75%). Retail sales were a source of volatility on Friday, helping 10y UST trade to an overnight high of 0.7556%. The US Treasury markets continues to travel with the notion that a stimulus is coming, the big question is whether it comes this side of the elections, Pelosi’s Tuesday’s deadline could bring some fireworks this week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.