Total spending grew 0.9% in June.

The FOMC minutes released highlight the divisions in the Fed at their last meeting.

https://soundcloud.com/user-291029717/a-divided-fed-a-failed-bond-auction-and-a-blistering-brexit?in=user-291029717/sets/the-morning-call

I’m goin’ to Jackson, I’m gonna mess around,Yeah, I’m goin’ to Jackson,Look out Jackson town – Johnny Cash

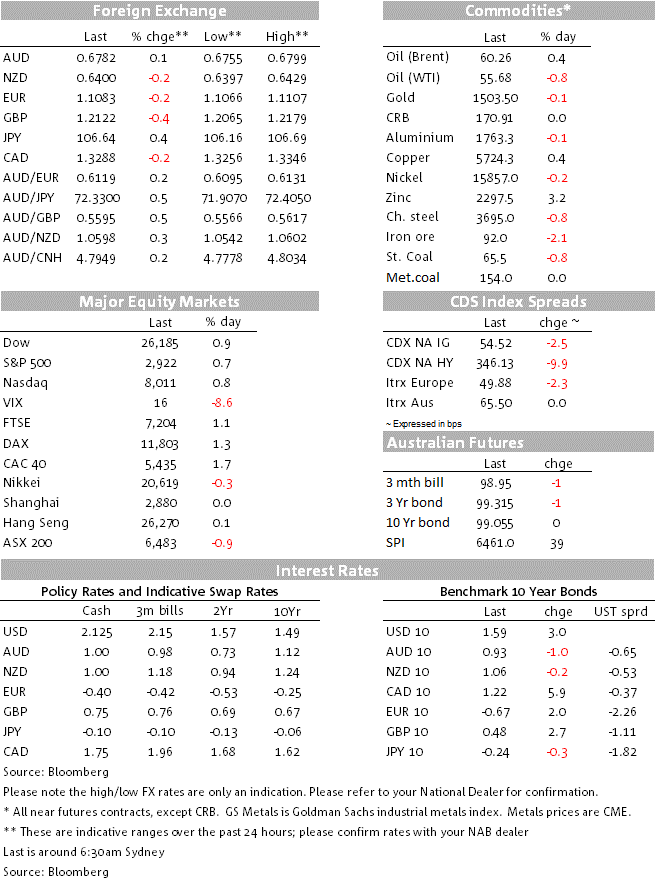

The hot and cold vibes in the equity markets continue with gains in the overnight session effectively reversing the losses recorded the previous day. The somewhat dated July FOMC minutes released this morning only elicited a small market reaction with the move higher in UST yields boosting the USD across the board. Key message from the Minutes was that the July rate cut decision was a just a mid-cycle adjustment, but given uncertainties, particularly in terms of trade policy developments, the Minutes also stressed the need to be flexible. Post the Minutes the AUD lost a bit of ground to end the day unchanged at 0.6780 while the NZD has continued to drift lower, briefly trading sub 0.64.

The Fed decision to lower the funds rate by 25bps on July 31st predate the increase in US-China trade tensions following President Trump late tweet on August 1st announcing his intentions to impose a 10% tariffs on the $300bn worth of currently un-tariffed China imports . Thus the Fed minutes do not reflect the change in market sentiment which has resulted in a volatile environment in equity markets and sharp decline in core global yields with 10y UST yields declining 43bps over the period to be currently at 1.59%bps.

So bearing that in mind the key message from the Fed Minutes is that the 25bps cut in July was just a calibration, a mid cycle adjustment and not the start of a new easing cycle, thus consistent with the message delivered by Fed Chair Powell at his post meeting press conference. More interestingly, the Minutes showed an acknowledgment from officials that the US administration trade policy was likely to be more of a longer lasting rather than transitory uncertainty, resulting in a “persistent headwind” for the US economic outlook. Therefore and notwithstanding the emphasis in the message that the 25bps funds rate cut was just a small calibration, the Minutes also stressed the need to be flexible given “the nature of the risks weighing on the economy “and “the absence of clarity regarding when those risks might be resolved”. A couple of officials had favoured a 50bps cut while several wanted to keep rates on hold. As for the outlook on inflation, the majority of officials (so not all) believed that recent inflation data prints suggested that lower readings earlier this year were likely to prove transitory, thus one could conclude that, on its own, the Fed outlook on inflation did not warrant an imminent adjustment ( lower) to the funds rate.

Late in July the consensus view within the Fed was that “that the real economy continued to be in a good place,” and based on the improvement in US data releases since the July meeting, as evident by the move higher in the US economic surprise index since then, it would seem fair to suggest that the Fed positive view on the US economy remains unchanged today. This probably helps explain the post Minutes move higher in UST yields which has been led by the front end of the curve. Both 2y and 10y UST yields climbed 4bps and are currently trade at 1.57% and 1.589% respectively.

UST yields remain close to recent lows, but looking into mid to longer themes, is worth noting the news from the Congressional Budget Office, an independent arm of the government. The Office noted that that the US fiscal outlook was “challenging” with debt on an “unsustainable course”. It projected that the US budget deficit was set to rise to $960bn this year (4.5 % of GDP), on the back of lower-than-expected tax revenues, and warned that over the next decade the deficit would be $809bn larger than previously forecast, following the bipartisan deal on spending last month.

Before moving on to currencies, the other “bond news“, overnight was the tepid demand encountered by the first sell a 30y zero coupon bond with negative yield. The German 30y 0% bond failed to meet a €2bn target, selling €824m bonds at an average yield of -0.11% . It may be early days, but the soft auction could be signalling appetite for negative yields may be waning.

The move higher in UST yields helped the USD make some broad gains within G10 and EM with the BBDXY and DXY index closing the day 0.11% bps higher. Meanwhile after almost trading with a 68 handle (overnight high of 0.6799),the AUD now trades at 0.6781 and it is essentially unchanged over the past 24 hours. An empty domestic calendar suggest the AUD is likely to remain at the mercy of offshore events and headlines with focus today on PMI releases, ECB Minutes and the start of the Fed Jacksons Hole (see more below).

NZD also had a similar range trading pattern, although relative to the AUD the kiwi’s downtrend remains more pronounced. Overnight the Kiwi briefly traded sub 0.64 and the AUD/NZD has continued trade higher, briefly trading with a 1.06 handle.

GBP has been on the soft side and is down 0.4% to 1.2120. UK PM Johnson met German Chancellor Merkel, and Merkel set Johnson the challenge of resolving the Irish Border issue in 30 days by putting forward concrete alternatives. Good luck with that. The French government said that it expects the UK to leave the EU without a withdrawal agreement which will mean the immediate imposition of controls on the EU’s borders with the UK. Indeed, the risk of a no-deal Brexit seems to be rising by the week. JPY is also on the soft side, with USD/JPY up 0.3% to 106.60, while EUR is flat a just below 1.11

CAD is slightly stronger. Canada CPI data showed the average of the three core measures remaining at 2.0%, making it the only major central bank meeting its inflation target. The data tempered the view of any urgency for the BoC to cut rates alongside other central banks and, despite inflation being on target, the market continues to almost fully price a chance of a 25bps cut by the December meeting.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.