We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

After three days debating the size and shape of the European Recovery Plan, EU leaders failed to reach an agreement.

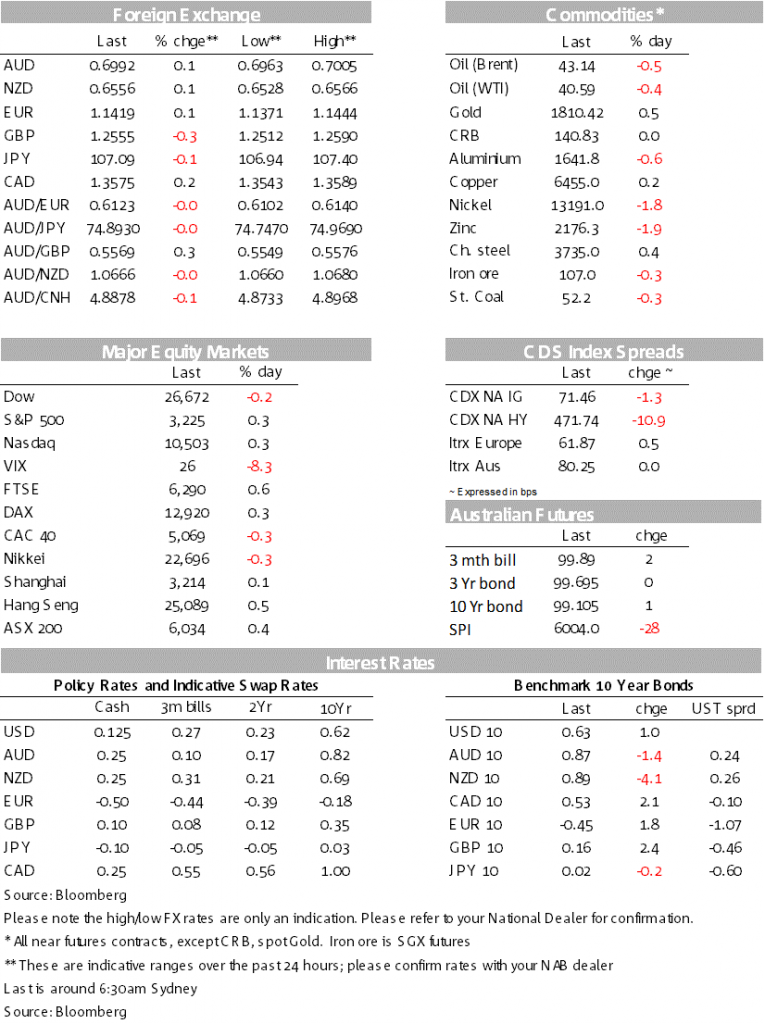

EU leaders have yet to reach consensus on the €750bn recovery fund, though market reaction at the open has been minimal with EUR -0.2% to 1.1419 (the meeting is still going as I hit send). Market moves on Friday were modest with equities nudging higher (S&P 500 +0.3%), the USD lower (-0.3%) and yields little changed (US 10yr +1.0bps to 0.63%). This week’s focus will continue to be on earnings, and on various fiscal packages with the Australian Economic Update on Thursday, the US needing to approve a package by July 31, along with the EU’s recovery fund.

“And when you can see how it’s gotta be; You’re making your mind up; And try to look as if you don’t care less; But if you want to see some more; Bending the rules of the game will let you find; The one you’re looking for”, Bucks Fizz 1980.

“Making Your Mind Up” was the 1981 Eurovision winner and helped Bucks Fizz dominate the 80s pop-rock genre. So it was over the weekend with EU leaders still yet to reach consensus on the €750bn Recovery Fund despite three days of talks. Leaders are still talking as I hit send.

The main points of contention remain on the mix between loans and grants (latest proposal is €400 in grants and €350 in loans), and the degree of oversight involved in the spending of the funds. Putting aside the obvious acrimonious headlines (Merkel and Macron walking out on Dutch PM Rutte), the commitment by EU leaders in extending talks and reports of further talks if no agreement is reached today shows the desire to have the recovery fund in some form.

Accordingly EUR has been resilient to the disappointing news, down just -0.2% to 1.1417 (EUR had reached a high of 1.1444 on Friday). The medium-term implications though are it will be a very long and winding road to any Hamiltonian moment for the EU or Eurozone.

Market moves on Friday were modest with the S&P500 up 0.3% and in the upper end of its wide range since early June. Helping support sentiment was the recovery in Chinese markets on Friday after they fell -4.8% on Thursday with the CSI 300 +0.6%. Earnings reports so far have not phased the rally with key names to report this week including Microsoft, Amazon and Coca Cola.

FX moves were largely driven by developments in the EUR ahead of the EU leaders summit with the USD (DXY) falling -0.3% on Friday, and is up 0.1% as trade opens. Moves in other major pairs have been modest with the AUD steady as we open at 0.6992 with still a lot of resistance above 0.70.

July Consumer Confidence out of the Uni Michigan Survey missed expectations (73.2 v 79e), with likely the resurgence of COVID-19 and the re-imposition of restrictions in some states weighing. A further drop in sentiment is likely, especially if Congress fails to pass the enhanced unemployment benefits. As for Housing Starts and Permits they were close enough to expectations with housing construction remaining a bright spot in the US economy given how low rates are.

Virus news in Australia to date has had little impact on markets apart from the semi space where spreads in TCV have widened to CGS. The virus resurgence in Victoria has yet to peak which is concerning given almost 12 days of lockdown in Melbourne with stronger restrictions flagged. Premier Andrews said that from midnight on Wednesday wearing a face mask would be mandatory in Melbourne and the Mitchell Shire for anyone 12 or older. NSW is also reportedly closely watching virus developments given a recent increase in cases.

The virus resurgence also means the extension of various stimulus programs with the government set to unveil its Economic Update on Thursday. The AFR reports the re-vamped JobKeeper scheme will have rolling threshold eligibility and will tier payments (instead of a flat $1,500 per worker). There will be a JobSeeker Supplement, but the amount will be a pared, while the loan program to SMEs will be re-vamped given low take up. Originally a total $40bn had been pledged in loans, but the scheme has seen only $1.5bn issued for 15,600 loans. The re-vamped scheme will extend loan terms to five years (from three years) and the maximum amount increased to $1m from ($250,000). Further initiatives though will have to wait for the full Budget on October 6 with the AFR also reporting tax incentives to drive business investment will be postponed until October – to when we have a better gauge of whether the virus is back under control.

Another stimulus package is likely to garner focus this week is in the US where a July 31 deadline means a tight deadline to approve a package. On July 31 the $600 a week unemployment benefit bonus payment expires with around 25m Americans receiving the payments. If the scheme lapses, it will provide a big shock to incomes for those receiving unemployment benefits. While both parties appear eager to pass another stimulus bill, there are key disagreements on the size of the bonus payment (Republicans want less saying it discourages people from returning to work), while President Trump has said he wants to cut payroll tax and have liability protection for employers. Treasury Secretary Mnuchin also said on Friday that the administration wanted to extend the PPP scheme which provides support to small businesses, albeit targeted more specifically at struggling firms.

Cases in the US continue to rise – over 77,000 new cases were reported on Friday, a new daily record – and some of those affected Southern and Western states have subsequently rolled back some of their opening plans. California’s Governor said public schools wouldn’t be able to reopen in August unless the respective counties had COVID-19 under control, suggesting more than 70% of public school students will need to continue with remote learning when the new school year starts. There has also been a new outbreak in the Spanish region of Catalonia.

The resurgence in the virus means renewed focus on the extension of various fiscal stimulus programs. AstraZeneca and Oxford University are set to publish their eagerly-anticipated results from their phase one trials tonight, with reports last week suggesting they were expected to be positive.

A busy week domestically with RBA Governor Lowe speaking Tuesday, the government’s Economic Update on Thursday, while a flash-read of Retail Sales is on Wednesday. As for the Economic Update on Thursday, the government will also announce its plan for the JobKeeper wage subsidy beyond September, following a review by Treasury.

We expect the government will extend JobKeeper past September, but in a more targeted way. On the budget update, the government should confirm a FY20 deficit of around $85b (4.5% of GDP) and forecast a deficit of around $210b in FY21 (11% of GDP), the biggest deficit since WWII. Governor Lowe’s speech is to the NAB sponsored Anika Foundation luncheon (Tuesday) on COVID 19, the Labour Market and Public-sector Balance Sheets shortly after the release of the RBA minutes. Focus will also remain on the path of the virus in Victoria (we should start to see the results of recent lockdown) and whether cases pick-up in NSW.

It’s a relatively quiet week with most focus on the US and EU fiscal packages, as well as earnings reports that include Microsoft, IBM, Unilever, and Coca-Cola, amongst others.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.