NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The market continues to respond to the Dovish Fed statement yesterday with a rally in US equities, falls in Treasury yields and a fall in the US dollar.

https://soundcloud.com/user-291029717/after-the-fed-bond-yields-down-dollar-down-equities-up?in=user-291029717/sets/the-morning-call

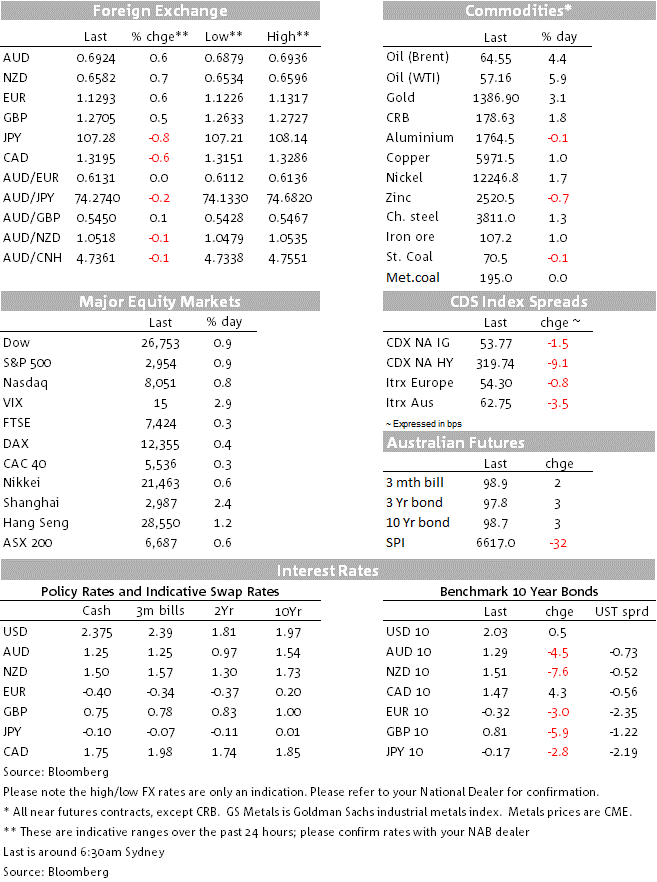

Risk markets are still basking in the afterglow of the Fed’s latest messaging on rates and the spectacle of 10-year Treasury bonds yields trading below 2% for the first time since October 2016 – a month before the Fed embarked on its tightening cycle and when the Fed Funds Rate was down at 0.25-0.5%. The US dollar continues to leak lower in these circumstances, down about 0.5% in index terms and the reason the AUD is back on a 0.69 handle this morning for the first time this week.

US equities have just closed with the S&P at a new record closing high (for the first time since April), up just shy of 1%, with similar sized gains for the Dow and NASDAQ. Admittedly gains have been supported by the 2%+ boost to energy stocks from the near $3 jump in crude prices after yesterday’s news of a US drone being shot down in the Strait of Hormuz. But every S&P sub-sector is up by at least 0.5% and key growth sub-sectors – IT, Industrials and Materials – are all up by over 1%. Also helping defray a ‘risk-off’ response to the geopolitical news was US President Trump opining that he suspected the downing of the US drone was likely a ‘mistake’ by a ‘general or someone’ and that it would have been a much bigger deal has it been piloted.

US Treasury yields have given back a little back of the sharp falls we saw both in the immediate aftermath of the FOMC decision and during yesterday’s Tokyo session (where most Treasury bond trading originates in the APAC region) and which took 10-year Treasuries down to a low of 1.975% and the 2-year note to 1.694%. We’re currently back at 2.02% and 1.763% – a very meagre correction given the scale of yesterday’s moves – and best seen in the context of a rise of about 5bp in ‘break-evens’ – the inflation expectations component of bond yields – directly off the back of the oil price news.

10-year bond yields in other parts of the world fell by 3bp in Germany to -0.32%, so maintaining Wednesday’s post-Draghi speech rally – and in the UK by almost 6bps after the Bank of England offered a downbeat assessment on the economy, keeping rates steady and noting rising risks to growth, including trade tensions and the risk of a no-deal Brexit. Guidance for future rate hikes remains contingent on a smooth Brexit path while the minutes acknowledge that financial markets are pricing in an alternative scenario. In Japan, 10-year JGBS fell to -0.2%, pulled down by developments in bond markets elsewhere in the world and after the BoJ left policy unchanged yesterday and continued to offer a positive assessment of the outlook, albeit listing a bunch of (mostly global) downside risk factors to this view.

In FX it’s mostly either oil linked currencies (NOK especially) or the ultra-low/negative yielders that have gained the most in the last 24 hours. NOK is up a cool 1.75% on this time yesterday, following a rate hike by the Norges Bank that, together with Sweden (SEK +0.8%) marks out these countries’ central banks as the only two in the developed world with a tightening bias. CHF is up 1.24% which has pulled EUR/CHF down to below 1.11 and its lowest levels since mid-2017. So no signs of a ‘line in the sand’ here that the SNB is willing to defend.

CAD has also benefited from the price surge (+0.6%) while the EUR, GBP and AUD are all up ‘only’ about 0.5% (NZD by a bigger 0.7%, with some ex-USD support drawn from the failure of yesterday’s Q! GDP print to disappoint, coming in on expectations at 0.6%). GBP was not fazed – on Thursday at least – by confirmation that Boris Johnson and Jeremy Hunt the incumbent Foreign Secretary) will be the two contenders fighting for the party leadership and so prime ministership when put to the party membership on July 23rd.

The AUD/USD move back above 0.69 is the headline grabber for our market but must be seen in the context of USD slippage. Under the hood we’d do well to note that the AUD is weaker on most of the crosses (AUD/GBP an exception) with losses most pronounced in AUD/JPY (down almost 3% month to date) and AUD/CAD, also down 3% so far in June and to its lowest levels since last October. AUD/NZD has traded clear below 1.05 for the first time since early April but is currently just back above at 1.0511.

The RBA’s latest guidance courtesy of Governor Lowe speaking in Adelaide yesterday is part of the story behind cross-rate weakness. Dr.Lowe’s key remark was that, “It would, however, be unrealistic to expect that lowering interest rates by ¼ of a percentage point will materially shift the path we look to be on. The most recent data – including the GDP and labour market data – do not suggest we are making any inroads into the economy’s spare capacity. Given this, the possibility of lower interest rates remains on the table”. This was enough to convince us, and some other banks, to bring forward our expectation for the timing of the next RBA cut to July from August. Money markets currently have a 0.75% cash rate fully priced by the end of the year (also NAB’s forecast).

Commodities other than oil are generally going better, gold up $34 since the FOMC, so breaking clear above its 2016, 2017 and 2018 highs. Iron ore looks have benefited from news that Rio was experiencing mine operational challenges, particularly in the Greater Brockman hub in the Pilbara and as a result, has lowered its full year (CY2019) iron ore guidance by some 4%. We did have news that production was set to resume at Vale’s Brucutu mine in Brazil, but his is a relative small operation. Iron ore futures were up another 1% Thursday.

Finally US data was confined to the Philadelphia Fed Business Outlook, weak at 0.3, down from 16.6 and versus 10.4 expected but afflicted by the same Mexico tariff-threat news in early June that downed the earlier-reported Empire manufacturing survey. US weekly jobless claims remained very low, falling to 216k from 223k previously.

After the excitement of the ECB, Fed and RBA this week, it looks like a central bank free Friday

Locally/APAC time-zone we have only the CBA PMIs and Japan May nationwide CPI

Offshore early this evening the ‘flash’ French, German and pan-Eurozone PMIs get star billing (covering manufacturing, services and the composite measure). Consensus is for minor rises in France and falls in Germany, with the pan-Eurozone Composite reading expected at 52.0 from 51.8.

The US also has the Markit version of its PMIs and also Existing Home Sales

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.