Coming in for landing in a heavy cross wind

Insight

The US was on holiday Monday so it’s been a quiet session all round.

https://soundcloud.com/user-291029717/all-quiet-until-trump-talks?in=user-291029717/sets/the-morning-call

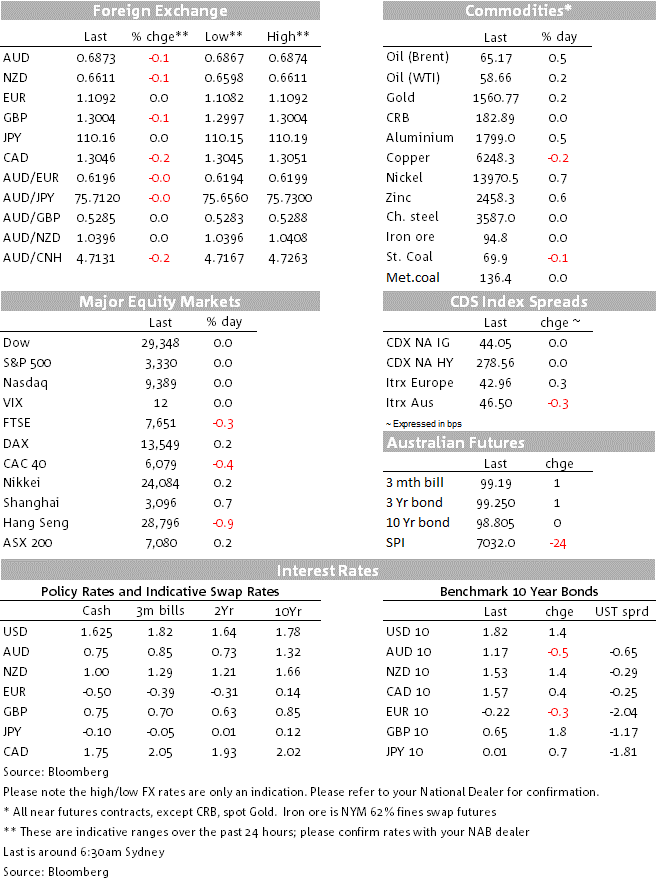

Sweet Dreams (Are Made of This) by the Eurythmics pretty much sums up overnight developments with the Martin Luther King holiday in the US making it a quiet night for markets. There has also been little news of significance, with only the IMF trimming global growth forecasts (though still forecasting 2020 to be better than 2019) and some further easing in trade rhetoric with Trump and Macron agreeing to a trade/tax truce in reaction to France’s digital tax. Markets are little moved with G10 FX mostly +0.2% with EUR +0.0% to 1.1092, GBP -0.1% to 1.3003 and USD/YEN +0.0% to 110.16. The USD (DXY) correspondingly is unchanged at 97.63 with the AUD also little moved -0.1% to 0.6873. Global yields are also little changed with German 10yr Bunds -0.3bps to -0.22%, while US Treasury Futures are steady. The oil price was one exception with Brent +0.5%, though initial gains of circa 2% in reaction to Sundays developments in Libya were pared with expectations of the supply disruption not lasting long with negotiations underway.

As global leaders gather in Davos this week, the IMF trimmed its growth forecasts with 2020 growth shaved by a tenth to 3.3% from 3.4% and 2021 growth shaved two-tenths to 3.4% from 3.6%. Importantly though, growth is still forecast to be stronger than the 2.9% recorded in 2019 with risks less skewed to the downside given preliminary signs the slump in manufacturing and global trade is starting to bottom. Interestingly the Fund’s analysis finds that without the looser monetary policy during 2019 (there were 71 interest rate cuts by 49 central banks in 2019), global growth could have been 0.5%points lower. There is also expected to be a pivot of growth to emerging/developing markets with growth expected to pick-up to 4.4% in 2020 from 3.7% in 2019. In contrast growth is expected to slow in advanced economies to 1.6% in 2020 from 1.7%. (see IMF for further details).

Late in the session there was a further easing in trade rhetoric with President Trump and President Macron set to avoid a tariff escalation on French products that was in reaction to France’s digital tax. President Macron said “we will work together on a good agreement to avoid tariff escalation” and work on a global framework on taxing tech companies. The US had threatened to levy tariffs as high as 100% on $2.4bn of French goods and the truce will see France suspend the collection of tax until the end of the year. The EUR lifted 0.1% on the news. Further development on President Trump’s trade policy with Europe is likely today with Trump giving the opening address at Davos later today – note his 2018 address foreshadowed the US’ more unilateral approach to policy.

It has been very quiet in markets with little other news of significance. Headlines of Wuhan Fever in China is starting to emerge with so far 3 deaths reported and 218 people with symptoms. Worryingly there is some evidence of human-to-human transmission with 14 medical staff contracting the virus from one carrier (see SCMP for details). President Xi has said the virus must be “resolutely contained” and there are fears the fever could spread with hundreds of millions travelling for the Chinese New Year.

The oil price was the only mover of significance, though initial gains of around 2% have been pared with negotiations underway after Libya’s General Khalifa Haftar kept oil fields shut on Sunday. Diplomats though report limited progress in negotiations.

Finally as I am about to hit send, in NZ ANZ no longer expects the RBNZ to cut rates in May, expecting the RBNZ to keep the cash rate unchanged at 1% throughout 2020. Note the change brings ANZ inline our BNZ colleagues who moved to this view last year.

Another quiet day domestically with only usually second-tier weekly consumer confidence. International focus is likely to be on the UK given pricing for a January rate cut with employment data due. The World Economic Forum also kicks off with President Trump giving the opening address. Finally, US earnings season continues with Netflix the first FAANG to report.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.