Total spending grew 0.9% in June.

Since Monday the markets have dived, then climbed back again.

Like the sun, we will live to rise, Like the sun, we will live and die

And then ignite again – Soundgarden

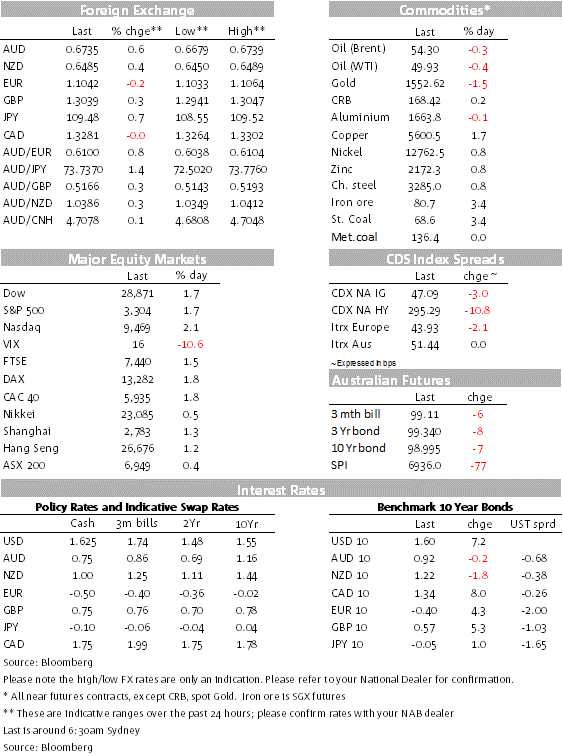

The hot and then cold and then hot again pattern in markets remains in place. After a very cold end to last week and a negative post-holiday catch up move by China’s equity market on Monday, markets have now embarked on a new rebound, spurred by China’s efforts to support its economy alongside an apparent decline in concerns over the Coronavirus impact on the global economy. US and EU equity markets have surged higher overnight, core global yields are up while some commodities have also joined the party. The USD is a little bit stronger in index terms, growth and risk sensitive currencies have outperformed while safe haven pairs have lagged behind. The AUD has been one of the outperformers, supported by an unchanged RBA cash rate decision and optimistic outlook by the Bank.

EU and US equity markets embraced the positive lead from Asia which was primarily driven by a big jump in China’s equity market (China’s CSI 300 index ended the day up 2.64%). There has been no positive news about the spreading coronavirus, with the number of confirmed cases and deaths continuing to rise at a steady rate – reaching over 20,500 and 425 respectively in China. However, the lack of an apparent acceleration in the number of new infections has been seen as an encouraging sign that measures to contain the virus outbreak are probing to be effective. At the same time, the market has also cheered China’s efforts to support its economy ( i.e PBoC cuts to select interest rates and liquidity injections). The Euro Stoxx 600 index closed 1.6% higher and as we type the S&P500 is up 1.72% while the Nasdaq index is +2.12%. The latter looks set to close at a new record high.

The risk-on session sees US Treasury yields much higher, with the 2 and 10-year rates up 6-8bps. The 10-year rate has moved upward at a steady pace and has pierced 1.60%. Some commodity markets have also joined the party, LMEX index is +1.04%, copper is +1.56% and iron ore is +4.21%. Bucking the trend however, oil prices have not been able to fully sustained their Asia gains , Brent crude is +0.2% and WTI is flat.

Safe havens CHF and JPY have underperformed. USD/JPY is up 0.66% to ¥109.510 while NOK and AUD are at the top of the G10 leader board with the latter supported by the RBA decision to stand pat and an optimistic outlook by the Bank.

Yesterday the RBA kept the cash rate unchanged at 0.75%, having last cut rates in October. Notwithstanding the bushfires and Coronavirus outbreak (too soon to know the latter’s impact) the Bank retained an overly-optimistic forecast with an unchanged outlook that sees GDP around 2¾ % this year and 3% next year with a slow improvement in the unemployment rate and underlying inflation gradually rising to the bottom of the 2-3% target band. The RBA thinks the cash is at a very low level already and again argued for patience, given the long and variable lags of the transmission of monetary policy. That said, the Board retained an easing bias, adding that it would “continue to monitor developments carefully, including in the labour market”.

The economy will significantly underperform the RBA’s outlook, especially given our underlying concern that private demand remains weak, with ongoing pressure on consumer spending from weak incomes. This leads us to expect the RBA will need to ease again in April. Governor Lowe speaks in Sydney today, the title of his speech is “The year ahead”, so we should get a better sense on the Bank’s rationale and risks.

The stronger AUD spilled over into the NZD, the kiwi is up 0.37% and currently trades at 0.6484. Overnight, the GDT dairy auction price index fell by 4.7, close to the 5% fall expected by our BNZ resident cow-whisperer Doug Steel. The NZX milk futures market had forewarned of reduced pricing, alongside the hit dealt to other commodities as traders look to weaker Chinese demand due to the coronavirus.

We are still waiting for the outcome of the Iowa vote, the first of the Democrats’ party vote to elect a candidate to run off against President Trump. Counting the votes has become a shambles with a breakdown in the technology that can surely only add to the chances of a Trump victory later in the year. Both Bernie Sanders and Pete Buttigieg declared victory based on their own analysis of the voting but the official result is expected to be declared later this morning.

Early days, but if Sanders wins today and as expected also gets New Hampshire (Feb 11th), then he will have some serious momentum behind him ahead of Nevada (Feb 22nd). If so the market will begin to seriously consider Sanders chances of winning the democrat presidential candidacy before super Tuesday on March 3rd (primaries on more than a dozen states). In his campaign Sanders has targeted healthcare, big tech and Financials sectors. He is in favour of “Medicare for All” and higher taxes, so not the most market friendly policies.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.