We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Shares have reverted to a focus on tech in the US with a sharp rise in tech stocks.

Ah, might as well jump (jump), Might as well jump, Go ahead an’ jump (jump), Go ahead and jump – Van Halen

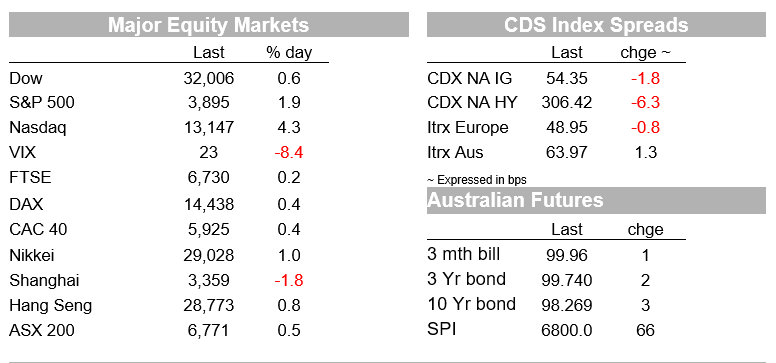

US equities are coming into the last hour of trade with the S&P up 2% and the NASDAQ +4.1%, with the sector breakdown of the S&P showing it is the IT sector (+3.9%) and consumer discretionary stocks (+4.2%) leading the charge higher. A tale of two drivers here, with ‘long duration’ tech. stocks seeming liking the move back lower in US Treasury yields (10s currently -5.5bps on the day to 1.54%) while the consumer discretionary sector the obvious beneficiary from appreciation of just how much cash is going to be sloshing around in US households’ bank accounts in the weeks ahead following passage of the $1.9tn Biden administration covid relief bill. This is on top of what they have already have, given the US savings rate currently stands at about 26%.

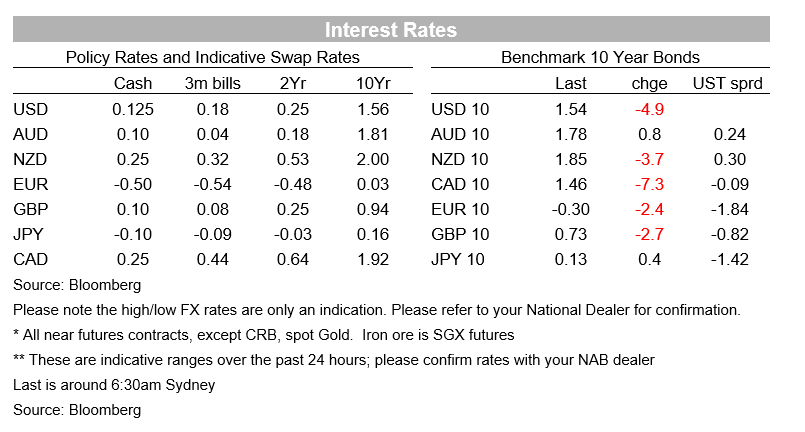

As for the fall-back in bond yields, the US Treasury’s sale of 3, 10 and 30 year notes and bonds got off to a good start with a well received 3-year ale last night, but the real test comes tonight and tomorrow, when the Treasury will auction $38bn and $24bn of 10 year notes and 30 year bonds respectively (remembering that it was the poorly received 7 year note auction at the end of last month that was one of catalysts for the subsequent broader Treasury market sell-off).

Tailwinds for stocks are arguably blowing too from yesterday’s reports of State-backed investment funds entering into the Chinese stock market, eliciting at one point a full recovery from the early morning 3% drop in the Shanghai Composite index (albeit two third of the rally failed to hold by the close).

Also to note is the sharp upward revision to the OECD’s global growth forecasts. While normally seen a lagging indicator of what private sector economist have long-ago concluded, the scale of the revisions is sufficiently striking that they do appear to have resonated. The OECD now pegs global growth in 2021 5.6% up from 4.2% previously, and in 2022 4.0% up from 3.7%. The revision to the US growth outlook is far and away the biggest, the OECD doubling its estimate to 6.5% from 3.2% previously (remember back in December when the OECD last published, we hadn’t even had the $900bn covid relief bill) with 2022 now put at 4.0% from 3.5%. But we also see Eurozone growth revised to 3.9% this year from 3.6% and from 3.3% to 3.8% next year, and in the UK to 5.1% this year (4.2%) and 4.7% next (4.2%).

For Australia, the lift is to 4.5% from 3.2% (bringing it roughly into line with NAB’s existing 4.4% forecast) while for 2022 The OECD is unchanged at 3.1%. Yesterday, NAB’s Business Survey showed Business Conditions and Confidence soar in February. Conditions rose to +15 from 9 (long-run average 5) along with Confidence to +16 from +12 (long-run average also 5). The rise was led by NSW and VIC. Capacity utilisation, which correlates with a lower unemployment rate, also rose 81.8% from 81.1 and is at its highest level since August 2019 when the unemployment rate was back at 5.2%. An undeniably strong survey.

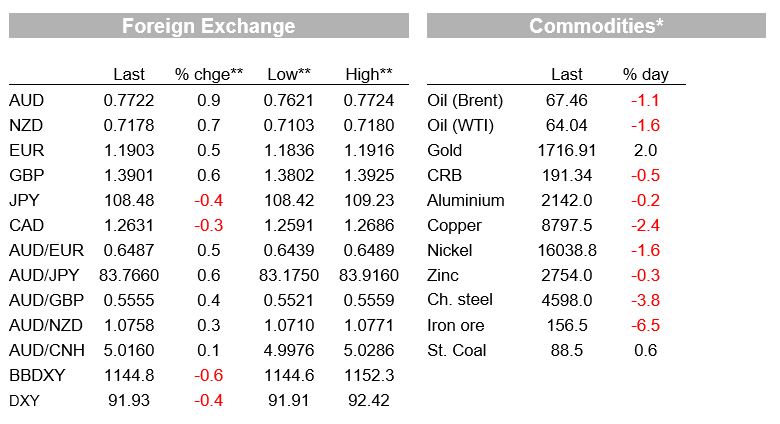

Consistent with the reversal in the bond and equity market, the USD has also reversed course (in the case of AUD, extending a bounce that was already underway following the aforementioned bounce in China stocks – even though gains in the latter didn’t hold – and pull back in USD/CNY after the move to almost 6.55 earlier in the Beijing day (to 6.5067 by the close). AUD/USD has recovered a full cent from its intraday low of 0.7621, to be 0.7724 as I type. The BBDXY index is currently down 0.6%, losses led by a 1% gain for the SEK and 0.9% gains for AUD, NOK nd CHF (CHF likely benefiting from an unwound of some of the recent carry trade activity, for which Swissie has of late been the funding currency of choice, Switzerland having the most negative rates in the worlds).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.