NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Despite extreme measures by the Fed yesterday and the return of QE, markets were far from impressed.

https://soundcloud.com/user-291029717/another-black-day-as-markets-look-for-light-at-the-end-of-the-tunnel?in=user-291029717/sets/the-morning-call

Baby, I can’t stay, you got to roll me

And call me the tumblin’ dice – Rolling Dice

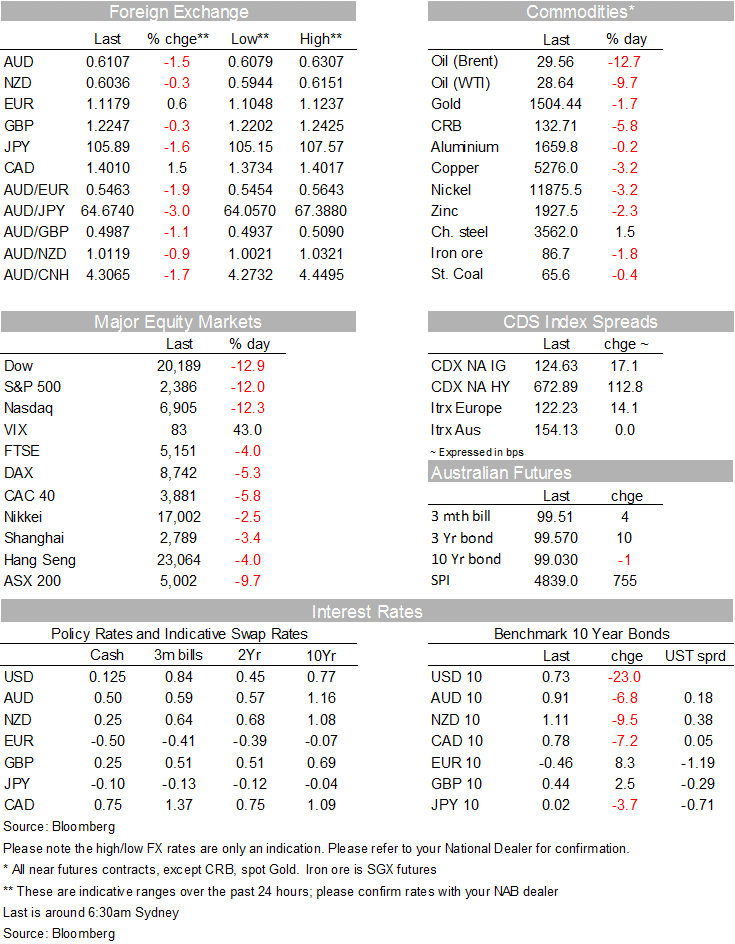

Drastic measures by the Fed and other Central Banks have failed to appease markets with investors still running towards the exit door of risk assets as governments step up their radical measures to contain the COVID-19 outbreak. The VIX equity volatility index is back above 75 as equities tumble across the globe. Brent oil trades sub $30 and even gold had a bad day falling over 4%. UST yields recover some of their post Fed losses helping the USD along the way. JPY and CHF show their safe haven attributes and AUD falls by more than NZD with the cross coming close to testing parity.

Yesterday’s drastic stimulatory measures by the Fed (100bps cut to the Funds rate to 0.25% plus QE), RBNZ ( RBNZ cutting OCR 75bps to 0.25% and hinting at QE as next step) and the BoJ increase in ETFS and REITS plus 0% loans to banks and CP/Corp QE) failed to provide a circuit breaker for the equity rout as investors increase their negative economic assessment from the COVID-19 outbreak and containment measures.

S&P500 futures hit their circuit breaker after falling close to 5%. European equity indices had another day of sharp declines with the Stoxx 600 Europe Index closing down 4.9%, after tumbling as much as 10% to its lowest since November 2012. Now as I type the S&P500 is down ~10% and the NASDAQ is close to -11%. Barring Consumer staples (-6,8%) all other 11 sectors in the S&P 500 index are down more than 10% and the VIX volatility Index is back at extreme levels seen during the GFC, above 75. The message from markets is that as much as monetary stimulus is a welcome move, lowering the price of borrowing and increasing liquidity are not enough. The required COVID-19 measures are hampering the global economy and with activity grinding to a halt, governments need to step in and provide support. Markets are crying out for more fiscal backing.

The Fed announcement triggered a big rally in UST at the Tokyo open. The 2y note traded to a low of 0.2617% and the 10y Note fell to 0.62%, these moves however proved short lived with yields climbing higher over the course of the night. The 2 year trades now at 0.37% while the 10y tenor is at 0.7387%. European bond yields also traded higher, 10y Bunds climbed 4bps to -0.55% and vulnerable peripheral bonds were smashed (Italy 10y +38bps). Meanwhile, breakeven inflation rates, derived from inflation-linked bonds have plummeted, the US 10-year breakeven rate fell another 20bps overnight to just 0.7% while the equivalent measure in Australia fell to below 0.6%.

The move higher in UST yields helped the USD recover all of its post Fed decline with the increase of USD also helping as investors look for the exit door and the safety of USD cash. Investment Fund are also facing an increase in demand for redemptions, so cash is king in this instance.

JPY and CHF have shown their safe haven attributes, outperforming the USD ( USD/JPY now at @105.33 +2.18%, CHF @ 0.9443 +0.78%). Meanwhile commodity linked currencies have underperformed not helped by broad declines in the commodity space with oil prices leading the move lower ( Brent -10.78%, WTI -9.32%). The AUD is down 1.39% to 0.6117 while the NZD is at 0.6024.

Yesterday’s BNZ 75bps cut to the OCR pushed the NZD briefly below 60c, but the pair has managed to outperform the AUD with the AUD/NZD cross coming to testing parity trading to an overnight low of 1.0021. The cross now trades at 1.011. In addition to the RBNZ move, yesterday, a factor weighing on the cross could be the RBA announcement that it is prepared to buy ACGBs, but we will have to wait till Thursday to see whether Cash Rate will be cut again and any formal QE/YCC pronouncement. The market is also focused on the NZ government potentially announcing very big fiscal stimulus today ( midday AEDT).

Countries are taking further drastic measures to limit the spread of COVID-19. New York City is closing bars, restaurants and gyms, similar measures to those announced a short while ago by Germany. There are widespread school closures in the US. The EU is reportedly considering banning all non-essential travel for 30 days. UK Prime Minister Boris Johnson asked the public to avoid all non-essential contact and travelling. On a more positive note, the Lombardy governor – the region in Italy which has the highest concentration of cases – said the growth in new cases in the region was no longer exponential.

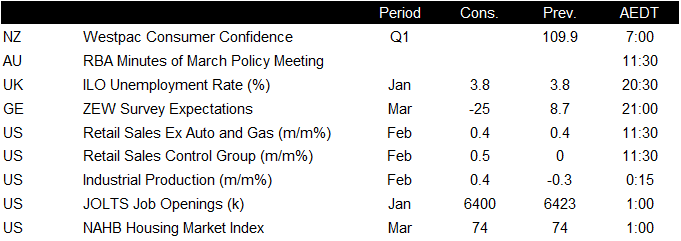

Economic data is starting to filter through, showing the dramatic impact of the virus, and associated containment measures, on economic activity. The Empire manufacturing index, based on firms in the New York region, experienced its biggest monthly fall on record, to levels last seen during the GFC. In China, where the outbreak originated, there were larger-than-expected falls across all activity indicators (retail sales -20.5%, industrial production -13.5%), as foreshadowed by the PMIs earlier in the month. But higher frequency Chinese data suggests activity is picking back up.

The RBA Minutes have been overtaken by recent events. RBA now says it is prepared to buy government bonds, but we will have to wait until Thursday to see whether Cash Rate will be cut again and any formal QE with or without Yield Curve Control pronouncement.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.