Coming in for landing in a heavy cross wind

Insight

Trade talks between the US and China took a turn for the worse at the end of last week, with the Trump administration issuing a list of $50 billion worth of products that would be hit with a 25 percent tariff.

https://soundcloud.com/user-291029717/the-great-tariff-wall-of-china

Friday’s news cycle was dominated by President Trump’s’ decision to go ahead with tariffs on $50bn of Chinese goods ($34bn straight away, $16bn subject to representations by affected US firms) and China’s immediate tit-for-tat retaliatory response.

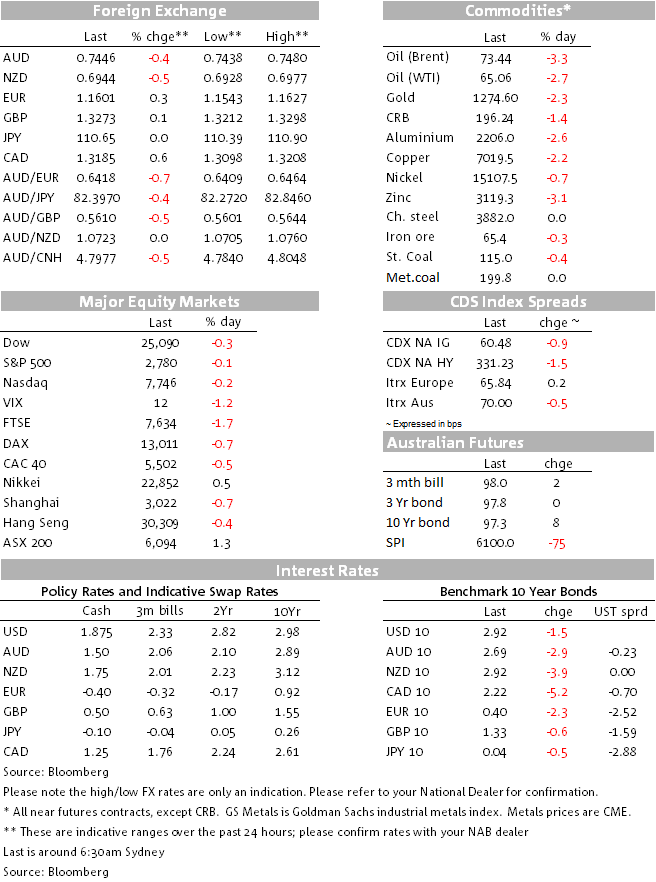

US equities held up well in the circumstances (and so VIX stayed down) with the S&P off only 0.1% (and virtually flat on the week) and other indices only a little more. Treasury yields were lower but by less than 2bps across the curve. The US dollar, which has to date consistently weakened whenever trade tensions have tightened, was 0.1% lower in narrow DXY terms but up very slightly in broader (BBDXY) terms.

In contrast, it was commodity prices, commodity currencies and Asian Emerging Market (EM) currencies which bore the brunt of the tariff news. Base metals and oil were down across the broad and NZD, AUD and CAD off by on average 0.5%. The Korean Won lost 1.5% while the currencies of China, India and Thailand were all down more than 0.5%. The moves on the week in these latter markets were even bigger (e.g. ADXY, the index of Asia EM currencies, was 0.4% lower on the day Friday but 0.9% down on the week. The AUD’s 2% weekly fall made it the worst performing G10 currency, losses eclipsing the Euro despite the latter’s crunch lower in the wake of the last Thursday’s ECB meeting.

The dye for the poor performance of EM markets and commodity currencies last week looks to have been cast on Tuesday when China reported soft creditor and money supply numbers for May, followed on Thursday by the quite significant downside surprises in the retail sales, industrial production and fixed asset investment readings.

The good US economic news kept on coming, the preliminary University of Michigan consumer sentiment reading rising to 99.3 from 98.9 (and versus March’s 101.4 cycle high). Industrial and manufacturing production numbers were both weaker than expected (latter -0.7%), but in large part due to a fire that had impacted a major parts supplier to the truck assembly sector.

Also notable on the US data front was the monthly US TICS (capital flows) data (for April). This showed net long term capital inflows of $93.9bn but mostly because US residents sold international securities and brought the money home (to the tune of $71.bn). Foreign investors were actually net sellers of US Treasuries in April, with official institutions selling a net $48.3bn and the private sector buying a net $44.6bn. A lot of this US capital repatriation may well have been out of EM.

In bond markets, Treasury yields were fairly uniformly lower on the day but not by much (1-2bps). On the week, the Treasury curve is flatter again (2s/10s by 7.5bps) with the Fed driving short end yields higher and the post-ECB fall in Bunds yields helping subdue longer dates yields. The 10yr UST-Bund spread ends unchanged on the week, still at 250bps. 10yr Italian BTP yields came in another 13bps or so Friday (15bps on the week) to see the spread 10bps tighter. The negative 10yr AU-US spread continues to widen, last week by some 5.5bps.

In FX, EUR managed to claw back a little of Thursday’s 1.9% post-ECB crunch to be the best performing G10 currency. GBP also ended slightly higher, shrugging off the news that Tory rebels led by Dominque Grieve had rejected the wording of the ‘Meaningful Say’ Brexit Bill amendment having earlier been satisfied by PM May’s verbal undertakings. The Lords’ Amendment comes back to the floor of the House of Commons this week and is a swing factor for Sterling. If will only take 14 ‘Tory rebels’ to support the amendment and side with the opposition for it to pass, which is actually a good news story for GBP in terms of an eventual ‘ soft’ Brexit, mandating parliamentary approval of whatever deal the government eventually agrees with the EU.

In commodities, it was a sea of red on the day and week. Nickel was Friday’s biggest loser while copper takes the wooden spoon on the week, down almost 5% following Friday’s 2.4% fall. Oil was down as much as 4% last week (Brent) in front of the OPEC meeting this week (Starting Friday), though expectations of an agreement to significantly increase production are in some doubt with, according to Bloomberg, Iran, Iraq and Venezuela threatening to block an agreement which, technically, requires unanimous approval.

Local news from the weekend, France’s penalty controversy aside and now Germany’s shock defeat to Mexico and Switzerland’s containment of Brazil, includes the preliminary weekend auction clearance rates. Across the combined Australian capital cities they remain below 60% (though above 50%). The 56.9% preliminary nationwide clearance rate is up from a final 53.8% last week on much improved volumes (1,991) after last weekend’s holiday-reduced auction schedule and which produced the lowest nationwide clearance rate since 2012. Sydney cleared a preliminary 55.8% (56.0% last weekend) and Melbourne 58.7% (versus 54.9%).

Trade tensions and potential further market fall-outs (in EM and with the Australia) will obviously feature this week, while central bank speak looms large with the ECB’s central bank conference in Sintra, Portugal kicking off tonight. ECB President Draghi gives opening remarks at 3:30am Tuesday AEST and a speaks at 6pm the same day. Fed chair Powell, BoJ Governor Kuroda and RBA Governor Phil Lowe are all in attendance.

It’s a light week for data; the ‘flash’ Eurozone PMI data on Friday are likely to be a highlight. OPEC meets Friday.

In Australia, The ABS measure of Q1 house prices is released on Tuesday and the NAB Cashless Retail Sales Index is published on Wednesday. The former is mostly old news, given the much more timely CoreLogic data, while the latter provides an early read on retail sales. House prices are expected to have declined -1.5% q/q, reflecting modestly weaker growth in Sydney and Melbourne. From the RBA, we receive the Minutes from its June Meeting on Tuesday and Governor Philip Lowe speaks at the Sintra Forum on Wednesday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.