NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Markets have returned to adopting a more cautious approach to the impact of COVID-19, after Apple said it didn’t expect to meet its forward guidance.

https://soundcloud.com/user-291029717/apple-sparks-concern-over-virus-impact?in=user-291029717/sets/the-morning-call

One bad apple don’t spoil the whole bunch, girl…

Oh, give it one more try before you give up on love – The Osmonds

Admittedly when I was looking for this song I thought it was by the Jackson 5, instead this 1970 number one hit was by The Osmonds, which in their own right went onto have a lot of success in the 70’s and then again in the 80’s after they reinvented themselves as a Country band. Anyway, my defence is that this number 1 hit was a few years before I was born and if you didn’t know better you would think a young Michael Jackson is the lead singer.

The past 24 hours has seen the market shift into a decisively risk off mod and it all started with one bad apple. After yesterday’s NY close, Apple warned that it doesn’t expect to meet earlier revenue guidance for the first quarter due to NCOVID-19 impact on its China operations, the news spooked risk assets triggering an equity market reassessment on the economic impact from the virus outbreak. Barring China, equity markets sold off in Asia and the risk off mood extended into the European and US sessions. Core global bonds yields shifted lower with longer dated bonds leading the decline, the 3m-10y UST curve inverted again while in FX the USD was broadly stronger. The euro briefly traded sub 1.08 with the risk off mood also weighing on the AUD and NZD.

For some time now, the buoyancy in equity markets following their rebound at the start of the month was looking vulnerable compared to the more subdued NCOVID-19 assessment evident in the US Treasury market (10y UST yields trading close to range lows) and FX land ( USD strength alongside weakness in risk sensitive currencies such as the AUD and NZD).

The debate on whether NCOVID-19 is a transient economic shock or worryingly a more longer lasting global economic headwind appears to be shifting in favour of the latter following Apple’s admission that it does not expect to meet revenue guidance given just two-weeks ago. Notably, Apple highlighted two underlining sources of weakness: (a) “while all of [our] facilities have reopened, they are ramping up more slowly than we had anticipated” (e.g. workers are stranded in quarantine zones); and (b) “All of our stores in China and many of our partner stores have been closed. Additionally, stores that are open have been operating at reduced hours and with very low customer traffic.

The announcement caused S&P 500 futures to fall around 0.5% during the Asian session yesterday, barring China stocks, Asia ended in the red, Europe closed 0.5% to 1.0% lower and as we are about to press the send the S&P 500 is -0.20% and the NASDAQ is +0.10%. After opening sharply lower US equities are staging a mini recovery, unwinding early declines over the past couple of hours.

The number of new NCOVID-19 cases continues to decline, with China reporting 1,886 new cases on February 17th down from 2,048 on February 16th. Importantly, recoveries are picking up as well, with 1,708 new recoveries reported on February 17th, up from 1,425 the previous day.

Yesterday China’s Global Times reported that “More than 80% of the 20,000 manufacturing firms supervised by State-owned Asset Supervision and Administration Commission of State Council have resumed production, adding that operating rate of petroleum, communications and transportation surpassed 95%, and some have reached 100%. This news should have been embraced warmly by the market, however high frequency data such as pollution levels and traffic congestion gauges in Beijing do not at this stage corroborate the upbeat official message, keeping investors wary.

Germany’s ZEW survey of financial analysts fell much more than expected in February, signalling that the virus was starting to impact economic sentiment in other countries. Expectations among the ZEW’s survey respondents had risen materially towards the end of last year, but the virus appears to have put an abrupt halt to that recovery. The ZEW President observed that export-oriented sectors had deteriorated “particularly sharply” as a result of COVID-19.

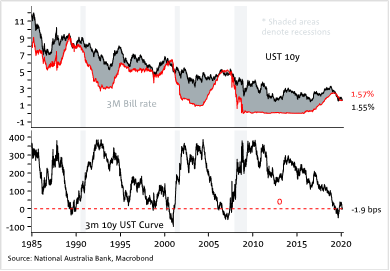

Core global yields drifted lower overnight with longer dated bonds leading the decline. The 10 year Treasury yield fell 4bps during Asian trading yesterday, to 1.54%, after Apple’s announcement. There was a brief spike higher in yields overnight after a much stronger-than-expected Empire manufacturing survey (of firms in the New York region), which rebounded to its highest level since September 2017. But the moves weren’t sustained, and yields were quick to reverse back towards the day’s lows. The 10y note now trades at 1.55% and notably too, the UST 3m-10y curve, a recession leading indicator, has rolled over into negative territory again (see chart below), while Fed rate cut pricing has pushed put to 1.6x by end 2020 vs 1.4x late last week.

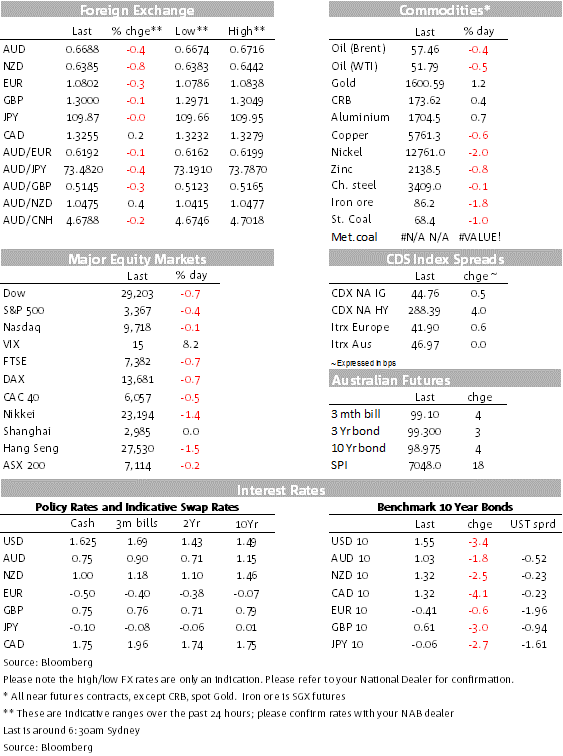

The USD remains the FX king, not only supported by its safe haven qualities, but also by its carry advantage in G10 (only surpassed by Canada’s higher cash yielding bonds) and by US growth relative to potential. The USD is 0.40% higher measured against majors (BBDXY) and 0.25% stronger compared to EM (EMCI) and ASIA FX ( ADXY).

The recent strong performance of the USD follows divergent data trends in the US and Europe (illustrated overnight by the rebound in the Empire survey set against the weakness in the ZEW). Citi’s US data surprise index is near its highest level since April-2018 while the European equivalent has fallen away sharply this month. Overnight the euro traded to a low of 1.0786 and as we type the pair remains below 1.08. Technically the euro does not have a lot of support with a 1.07 handle and the pair looks vulnerable. Related to this EU Fin Mins met in Brussels overnight and agreed to adopt a recommendation for a fiscal boost in the event of a downturn, “If downside risks materialise, fiscal responses should be differentiated, aiming for a more supportive stance at the aggregate level, while ensuring full respect of the Stability and Growth Pact”, according to a statement by EZ fin mins. We suspect that phrase ‘in line with Stability and Growth Pact’ won’t enamour investors. One to watch but markets will likely need convincing.

The risk-off backdrop has also benefited the USD against commodity and growth-sensitive currencies. The AUD came under pressure yesterday afternoon after the release of the RBA minutes to its February meeting. The minutes noted there was a case for further cuts, primarily because lower rates could “speed progress towards the Bank’s goals and make it more assured in the face of the current uncertainties.” The RBA weighed faster progress towards its economic goals against concerns that household debt could rise given the upswing in the housing market. The minutes also flagged concerns that the COVID-19 coronavirus outbreak presented a large downside risk for the outlook, especially given China is much more integrated into the global economy than compared to the 2003 SARS outbreak. The AUD is trading 0.4% lower than 24 hours ago, at around 0.6690.

The NZD is down around 0.8% since this time yesterday, amidst the broad-based strengthening in the USD, risk-off backdrop and weakness in the AUD after the release of the RBA minutes yesterday. The NZD is currently trading at around 0.6386, just above its lows for the year at 0.6378. Dairy prices fell another 2.9% at the fortnightly Global Dairy Trade auction overnight (-2.6% for whole milk powder), following on from the 4.7% fall at the previous auction. The decline overnight was broadly in-line with pre-auction indications and there wasn’t any NZD market reaction. The fall in dairy prices could trigger a round of downward revisions to analysts’ dairy payout forecasts, with the bottom of Fonterra’s current $7.00 to $7.60 range in their sights. We currently project $7.40, but subject to downward reassessment.

The JPY has outperformed (unchanged on the day) amidst the risk-off market moves and decline in US Treasury yields. The GBP has held-in well amidst a reasonably positive labour market report. UK employment rose by a larger-than-expected 180k, while the unemployment rate remained at 3.8%, equalling its lowest level since the mid-1970s. Wage data were slightly below expectations. The GBP is hovering around 1.30 at present, unchanged on the day against the USD (but well off the intraday highs).

Flattening of 3m- 10y UST curve flashing a warning sign again

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.