Online retail sales growth slowed in May following a fairly strong April

Insight

The Aussie dollar fell sharply yesterday on the back of disappointing jobs numbers, followed by weaker than anticipated activity data from China.

https://soundcloud.com/user-291029717/aussie-dollar-fall-continues-bond-yields-down-as-trade-delay-persists?in=user-291029717/sets/the-morning-call

I see a bad moon a-rising, I see trouble on the way, I see earthquakes and lightnin’, I see bad times today – Creedance Clearwater Revival

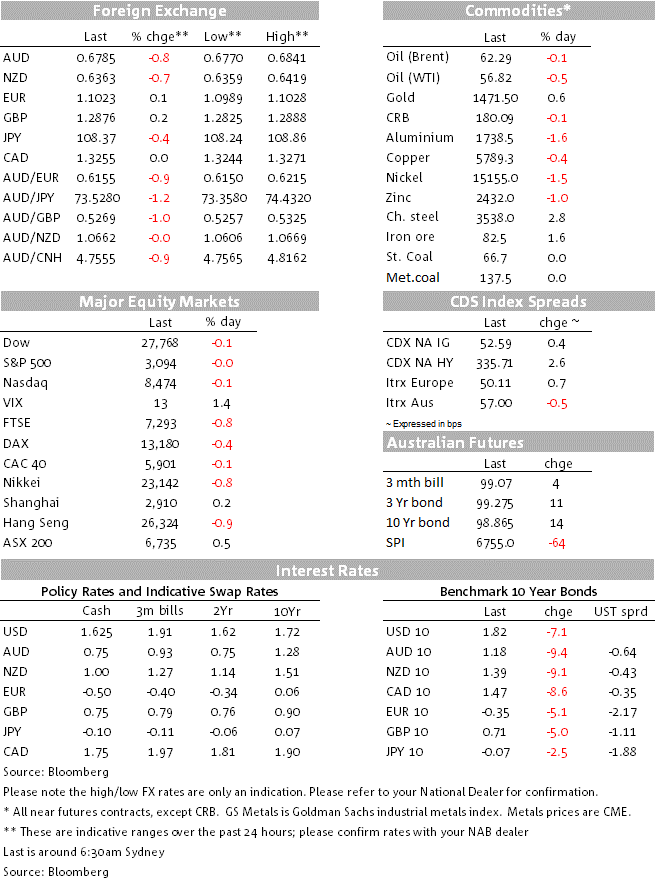

The AUD was the weakest G10 currency during the local time zone yesterday and losses have extended overnight, AUD/USD down to a low of 0.6770, the weakest level in a month. The initial hit came on news that the unemployment rate had edged back up to 5.3% (5.321% to be precise) despite a 0.1% drop in the participation rate, and that employment had fallen sharply (-19k, the first double-digit drop since 2016). As our economists noted post-release, slower – or negative – employment growth now presents an additional challenge to the RBA’s outlook for a recovery in consumer spending, where solid employment growth has been supporting household income and spending in an environment of weak wages growth.

Adding to the AUD’s misery and responsible for the dip below 0.68 yesterday was the October China activity data, in particular the further decline in the growth rate of industrial production, to 4.7% from 5.8% and against 5.4% expected, alongside which Fixed Asset Investment also missed expectations at 5.2% y/y against 5.4% prior and expected – the slowest rate of growth since 1998. Retail Sales also fell, to 7.2% from 7.8%y/y against an expected unchanged reading.

The net effect of the local and China economic news has been to push the market-implied probability of a further 0.25% cut to the RBA’s Cash Rate by February next year to above 70% from slightly less than 50%, and for a cut in December to 28% from 16% earlier in the week. NAB on Wednesday pushed out its call for the next cut to February from December .

Adding into the negative mix and following yesterday’s WSJ report that China was leery of committing to numerical targets on US agricultural purchases, the Financial Times now reports that the US and China are struggling to complete a “phase one” deal to halt their trade war, with senior officials in Washington and Beijing still jostling over intellectual property provisions, agricultural purchases and tariff rollbacks after weeks of negotiations. According to people close to the talks, Trump administration officials are frustrated that China has not offered enough concessions to justify a reduction in US tariffs on Chinese goods — a longstanding demand from Beijing that has become further entrenched in recent weeks. One person with knowledge of the discussions said that China was “absolutely” delaying the truce with its approach, jeopardising the chances that a final agreement could be reached in the coming days, the original target set by both sides.

The NZD is now matching the 0.8% 24-hour fall in the AUD, so giving back almost all of the gains that followed the unchanged RBNZ OCR decision on Wednesday. This is put down largely to contagion from the AUD move, though in comments to parliament this time yesterday, RBNZ Governor Orr said that it was “without doubt a tough decision to hold rates yesterday”, that the bank will do what it takes to meet its inflation and that rates need to stay low for a long period of time.

The JPY is the strongest G10 currency of the last 24 hours (AUD/JPY down from ¥74.40 to ¥73.40) with a relatively large fall in US Treasury yields together with a mild ‘risk-off’ tone to markets doing much of the work here.

Optimism toward Boris Johnson’s Conservative Party securing an outright majority on December 12th continuing to support, AUD/GBP falling back though 0.53 and to its lowest level in a month. This despite UK retail sales disappointing expectations, falling by 0.3% ex-auto fuel and by 0.1% in headline terms.

Germany avoided falling into a technical recession in Q3, its GDP coming in at +0.1% rather than the -0.1% expected. The news failed to cheer the EUR more than momentarily though, and indeed we might argue than in further diminishing the likelihood of significant fiscal stimulus from the Berlin government, it was not good news at all. EUR/USD has now recovered back to 1.1025 after a dip below 1.10, but largely because of general USD softness driven in part by the fall-back in US bond yields. 10 year treasuries are currently 7bp down on the day, versus a 5bp fall in equivalent German yields.

US data has been confined to weekly jobless claims, which rose to 225k from 215k but with the more pertinent 4-week average steady at 217k vs. 215k, and producer prices which at the core (ex food and energy) level remain benign at 1.6% y/y down from 2.0% in September.

US stocks are coming into the last hour of New York trading with the mainboard indices flat to very slightly lower, the S&P500 currently unchanged having been in negative territory for most of the session. The China data and lack of positive trade news looks to have been an influence, while Cisco Systems has been one stock-specific drag on the IT sector, down 8% after revising its revenue outlook after the close yesterday to now see a fall of 3-5% versus an earlier street estimate of +2.7%, citing businesses holding back from investment decision given prevailing uncertainties. The energy sector is also softer along with oil prices (WTI crude down 0.4%) after OPEC signalled that oil markets remain on course for a surplus in early 2020, despite which it said OPEC+ probably wouldn’t step up efforts to remove the excess when they meet next month.

Business NZ October manufacturing PMI (last at 48.4)

RBA deputy Governor Guy Debelle gives panel remarks at a FINSIA Signature event in titled ‘the Regulators’. His topic is Mortgage Arrears. We shouldn’t t therefore be on the lookout for any fresh insights on moentary policy, following yesterday’s poor labour market data.

There are a fair few current and former ECB officials due to pop up during the European day, where the main economic news is September Eurozone trade and final CPI (preliminary was 0.7% in headline terms, 1.1% for core).

In the United States tonight, the Empire (NY State) manufacturing survey – the first of the regional November PMIs – retail sales and industrial production.

Retail sales are seen rebounding after negative headline and ex-auto monthly changes in September, while industrial production is seen falling by 0.4% for the second month in a row, if so confirmation that the manufacturing sector is mired in recession as per the sub-50 Manufacturing ISM prints in each of the last three months.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.