Online retail sales growth slowed in May following a fairly strong April

Insight

The Australian and NZ dollars reached two-year highs in the overnight session.

https://soundcloud.com/user-291029717/aussie-dollar-flying-high-us-equities-stall?in=user-291029717/sets/the-morning-call

Smittens me with hope..Possibly maybe possibly maybe

possibly maybe – Björk

A small blip on what has been a solid month for investors. Lack of news suggest month end flows probably the main factor at play. Fed Clarida keeps the hope of Yield Curve Control alive, possibly maybe in the future, but not now. USD remains on the back foot, notwithstanding equity pullback. AUD briefly trades above 74c.

With regional indices down around the globe, barring Japan’s Nikkei, which got a nice lift ( up 1.12%) from one of the goats (Greatest Of All Time, Warren Buffet on new Berkshire Hathaway bought stakes in five major trading companies ) and the NASDAQ, which ended up 0.68%. Month end rebalancing flows have probably played a role in the lacklustre end to August for what has been a very decent month for equity investors. Microsoft (-1.48%) and Walmart (-1.03%) have been among the notable underperformers as the market reassesses their ability for the companies to jointly buy TikTok. Speculation is ripe with CNBC reporting a deal could be announced tomorrow while many investors believe there is a 50% chance TikTok will have to shut down its US operations.

Although the last day of August has been a disappointment for many equity investors, looking at the month’s performance, August was a very kind month for investors. The NASDAQ gained a cool 10%, the S&P 500 wasn’t too bad either, up 7.57% while the Shanghai Composite gained a relatively modest 2.59% followed by our S&P/ASX200 at 2.24%.

Fed vice-Chair Clarida speech was the highlight. The Vice Chair reiterated the Fed’s new monetary policy framework outlined by Chair Powell last week, regarding the new “average” 2% inflation target and one-sided employment objective. Of note, however, Clarida also said that yield curve control (yield caps) “were not warranted in the current environment but should remain an option that the committee could reassess in the future if circumstances changed markedly,”.

Clarida added that the FOMC might offer “refinements” to the Summary of Economic Projections (SEP) in light of the changes to the framework, with a decision of any potential changes by the end of the year. The SEP is currently published quarterly, providing the FOMC members’ economic and rates projections. Furthermore, he didn’t want to pre-judge any decision regarding potential changes in the Fed’s rates guidance or balance sheet communication.

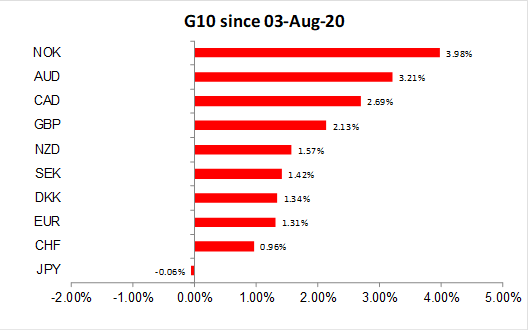

The USD has remained on the backfoot losing ground across the board with JPY the one exception in G10. Commodity linked currencies have been the past 24 hours outperformers with NOK up 1.42% and CAD up 0.48%, both up on a quiet night for oil prices ( WTI -0.41%), suggesting month end flows have probably been the biggest influence.

The AUD traded to a new year to date high of 0.7403, but it was unable to sustained the move and now trades at 0.7376, up 0.20%.

Similarly, the NZD also recorded a new year to date high of 0.6763, but now trades at 0.6733, essentially unchanged from levels this time yesterday. EUR met resistance at the same level seen mid-August, at 1.1966 and is currently up 0.3% at 1.1940. JPY has been the softest of the majors, with USD/JPY up 0.4% to 105.85, reversing some of the move seen late last week which occurred after reports of PM Abe stepping down for health reasons.

The Fed ultra-dovish stance with higher tolerance for elevated inflation is the overriding force in FX markets, the USD has ended August broadly weaker, with JPY the only G10 pair little changed.

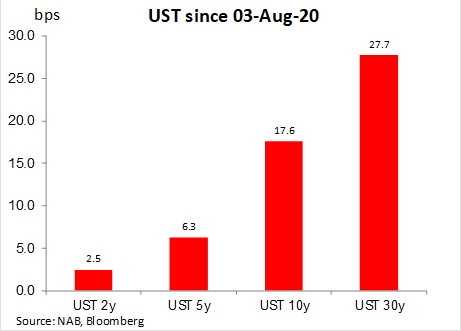

The UST curve flattened a little bit with the 10y Note down 2bps to 0.702% while the 30y Bond fell 3bps to 1.475%.

The big theme in August has been the steepening of curves with the Fed increased tolerance for inflation playing a big role ( see chart below). On this score is worth noting how the US 10-year break-even inflation rates made a fresh high, up 1.5bps to 1.79%, seeing real yields fall another 3bps.

European inflation rates were weak, with annual CPI inflation negative in August for Germany, Italy and Spain. Yesterday, China PMI data reaffirmed the economic expansion currently underway, China August manufacturing PMI came at 51.0 vs 51.2 expected and non-manufacturing gauge rose to 55.2 from July’s 54.2 , its strongest level since early 2018.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.