A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Australia’s CPI read today and US GDP numbers tonight.

https://soundcloud.com/user-291029717/uk-votes-on-voting-aussie-cpi-today-fed-tomorrow?in=user-291029717/sets/the-morning-call

It’s been a relatively quiet night, as is typically the case just in front of a Fed meeting outcome at 2pm Washington time Wednesday – 5:00am Thursday and where the nuancing of the language surrounding what is still widely expected to be a further 25-point reduction if the Fed Funds rate target is the market’s main focus. The UK parliament has just approved a December 12th General Election. Last night RBA governor Lowe again emphasised his prior vi that negative interest rates were extremely unlikely in Australia, but steered clear of expressing any view on the likelihood of other unconventional policy actions.

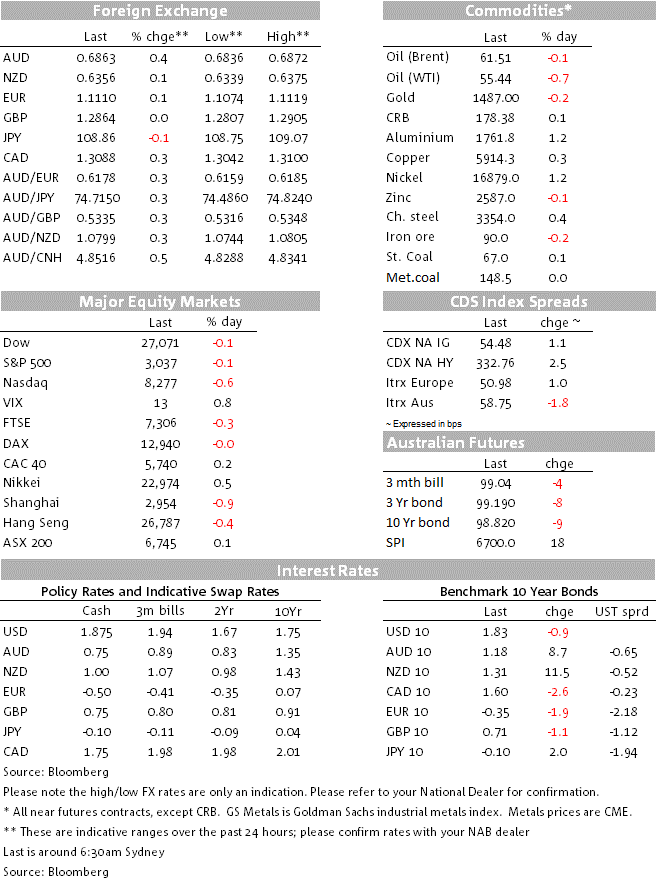

US equities have just closed with minor losses for the S&P 500 (-0.1%) and Dow (-0.09%) with the NADAQ underperforming both indices, -0.59%, dragged lower from the get-go of Tuesday’s trading by Alphabet’s earnings miss reported after Monday’s market close. Health care was the strongest sector of the S&P and only one to shows gains of more than 1%, after consensus-beating earnings reports from both Merck and Pfizer prior to the market open.

One initially negative development was on the US-China trade front, after Reuters reported that the so-called Phase-One agreement between the US and China might not be ready to be signed at the APEC meeting in Chile next month. Those headlines caused a short-lived dip in both equities and bond yields although a closer read of the article suggested that any delay would be due to timing constraints rather than a lack of commitment on either side. The article claimed good progress was still being made and the expectation is for an agreement at APEC.

US bond markets have seen the back up in Treasury yields either side of the weekend consolidate rather than extend or reverse. 2s are coming into the New York close -0.4bp at 1.64% and 10s -0.9bp at 1.833%. Earlier European bond markets closed with yields mostly 1-2bps lower.

Data releases overnight included the U.S. Conference Board’s measure of consumer confidence, which dipped to 125.0 from 126.3 (a touch weaker than expected) and US pending home sales, which rose by 1.5%, better than the 0.9% gain expected. Neither were market moving.

FX movers of note in the last 24 hours (i.e. of more than 0.1%) are confined to a strengthening in the AUD (AUD/USD +0.38% to 0.6863) and losses for the CAD (-0.26%), the latter in front of the Bank of Canada tonight and not news-driven.

Our 100-word version (well 128 actually) courtesy of NAB’s Kaixin Owyong goes something like this:

Governor Lowe used his speech “Some Echoes of Melville” to elaborate on recent remarks that there is an “excess of savings” driving lower global rates. Lowe highlighted an aging population, increased risk premia and weak productivity growth were contributing to an increased demand for savings and a suppressed appetite to invest. Lowe noted “these structural factors have had a powerful influence on the setting of interest rates over recent times” and ignoring these trends would see the exchange rate appreciate. That “would be unhelpful”. On unconventional policy, Lowe’s view was that negative rates were “extraordinarily unlikely” in Australia. In Q&A he took these comments further, highlighting worries that negative rates were having a “pernicious” effect on the functioning of the financial system and the pension system in Europe.

We’d judge largely because of Dr. Lowe’s evident distaste for any appreciation in the currency,. though AUD/USD currently stands a couple of pips above the levels prevailing before the Governor started speaking.

The UK House of Commons, with cross-party support, has just voted in favour of a General Election to be held on December 12th – having earlier rejected an opposition motion to hold it on December 9th – which will be first December election in the UK since 1923

The reason Sterling has struggled to hold onto (modest) knee jerk gains on news earlier in the day that an election date was likely to be agreed today, is because the outcome of an election is highly uncertain. According to Tuesday’s UK Evening Standard, the bookies have the Tories at 10/11 to win an outright majority (so just under 50%). A Tory majority is arguably the most Sterling positive outcome, initially at least, in so far as it means the government WAB can then be passed and the UK ‘Brexits’ no later than January 31st with a transition deal lasting though end-2020. This would like prompt a bigger short covering rally in all things GBP than we have seen to date, even though there will remain a high degree of uncertainty over what a post-Brexit UK-EU trading relationship will look like come 2021 (former UK chancellor Philip Hammond, who has since lost the Tory whip, has described the WAB as a potential ‘trap door’ no-deal Brexit).

Both Labour and the Scottish National Party will campaign on a 2nd referendum platform, and the Liberal Democrats on a platform to rescind Article 50 were they to win an outright majority. They won’t, the bookies putting the odds of this at 99/1, so in reality if there were a hung parliament, LibDems would then likely side with Labour and the SNP in support of another referendum. In so far as these three parties could then muster a majority, this is also a potentially GBP positive outcome, bringing the possibility of ‘Remain’ back onto the radar. But against this is the fact that markets would be terrified at the prospect of a Labour-led coalition government run by Jeremy Corbyn. He’d first have to be replaced by a more moderate Labour leader for markets not to take fright. Incidentally, the bookies have labour at 23/1 to win an outright majority.

Q3 CPI is this morning, where NAB forecasts headline and trimmed mean inflation remained unchanged at 0.4% q/q / 1.6% y/y. Trimmed mean inflation remains the Reserve Bank’s preferred measure of core inflation and the bank’s latest forecasts imply a quarterly outcome of 0.4 to 0.5%, broadly in line with our estimate and market consensus. For headline inflation, Q3 tends to be a seasonally stronger quarter, printing in the range of 0.4 to 0.7% q/q in recent years. However, we expect a fall in fuel prices, changes to energy market pricing and ongoing weakness in housing-related costs weighed on inflation in the quarter. In contrast, the Reserve Bank forecast for headline inflation is marginally higher at 0.5% in the quarter, the same as the market.

If our forecast for core inflation proves right, the Reserve Bank would likely read the data as continuing to suggest that spare capacity remains in the economy, consistent with below-trend growth and too-high unemployment. We doubt though that even a number below consensus is going to have a material impact on the likelihood or otherwise of the RBA electing to cut rates again as early as next Tuesday.

The highlight is the first (Advance) estimate of US Q3 GDP. The consensus looks for annualised growth in GDP of 1.6% after a 2.0% increase in Q2, incorporating still-solid consumption. Watch out too for the GDP deflator, where the Fed’s preferred core PCE number is expected to rise from 1.9% in Q2 to 2.2% and up from just 1.1% in Q1. We also get ADP’s employment change estimate, ahead of Friday’s non-farm payrolls. The FOMC commences it’s two-day meeting, the outcome of which will be published at 05:00 AEDT on Thursday.

We will get German October CPI and the Bank of Canada’s latest policy decision; on the latter we expect a still-straight bat to be played, with a neutral outlook as well as unchanged policy. For one, Canada is not currently afflicted with the challenge of wages being too low to be compatible with the inflation target, unlike here.

Both Facebook and Apple report Q3 earnings after Wednesday’s NYSE close

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.

Article

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.