A private sector improvement to support growth

Insight

The US Senate is seemingly preoccupied with pushing through Amy Coney Barrett as Supreme Court nominee, casting aside any bandwidth for fiscal stimulus talks.

https://soundcloud.com/user-291029717/barrett-trumps-stimulus-on-columbus-day?in=user-291029717/sets/the-morning-call

I’m on fire, I’m on fire, I’m on fire, I’m on fire – Van Halen

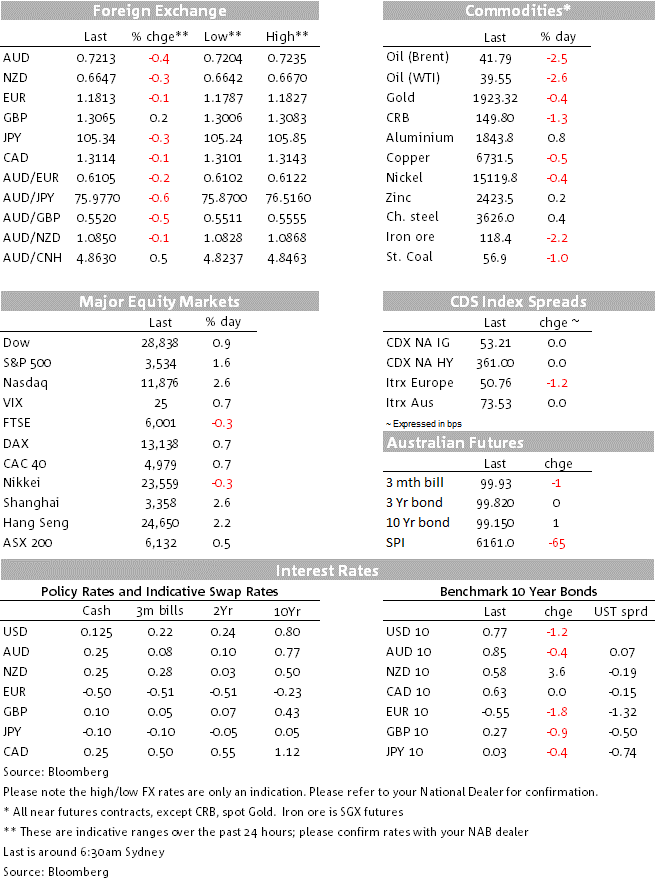

US bond markets have been shut overnight due to the Columbus Day holiday but not the stock market, where the NASDAQ, already up 1% in futures markets during the APAC session, raced to a 3% gain before pulling back into the close (NADDAQ ending +2.6%, the S&P +1.6% and Russell 2000 +1.5%).

The curiosity here, for this scribe at least, is that if the proximate cause of the rally is growing market confidence in an uncontested Biden election victory on November 3rd and the promise of big fiscal stimulus, as appears to be the case, then we might reasonably have expected that the recent outperformance of the Russell 2000 would be continuing. This on the basis that fiscal stimulus would disproportionately benefit small cap, domestically focused, companies, while Big Tech is likely to come into the cross-hairs both on the regulatory front and as the primary target of currently mothballed pans for a global digital tax regime.

Yesterday, the FT reported that the EU is drawing up plans to impose more stringent regulatory requirements on big internet companies with dominant market shares, specifically aimed at protecting and encouraging the development of competitors, yet the news was summarily ignored (shares of Apple are up 6%, Facebook 5% and Google 4%). Go figure, but for now it seems, the reduced uncertainty over the election and the promise of large scale fiscal stimulus is evidently overriding concerns about higher corporate taxes and more regulation. ‘We can worry about that later, if ever” seems to be the current investor market mindset.

As for the (fast diminishing prospects) for fiscal support this side of the US election, the start of nomination hearings in the Senate for Amy Coney Barrett speaks volumes about current Senate priorities, where is any event a bunch of Republican Senators made clear over the weekend they have no enthusiasm for endorsing the White House’s revised offer of a $1.8tn stimulus but which House speaker Nancy Pelosi has also rejected as insufficient and lacking specifics on how all the money would be spent. For now, lack of progress here may be one factor driving Biden’s poll standings higher in so far as Republican Party intransigence is seeming viewed for the most part as the main obstacle to a deal.

The other curiosity given the strength of US stock markets is that AUD (-0.4%) and NZD (-0.3%) sit squarely at the bottom of the G10 FX table. Here, the ready explanation is the impact of the weekend PBoC announcement that the 20% reserve requirements on FX forward transactions has been scrapped, a move seen making it less expensive to short the RMB as well as sending a fairly strong signals that the pace and magnitude of recent RMB appreciation, particularly in CNH over the recent Chinese holiday period, has made the PBoC uncomfortable and that the market had perhaps become too one-way. We still believe that more RMB appreciation lies ahead in the context of structural forces (e.g. market liberalisation and flows resulting from, among other things, inclusion of RMB bonds in global indices) as well as cyclical pressured from expected further US dollar weakness. For now though, the PBoC’s signalling has weakened the link between risk sentiment and the (procyclical) AUD and NZD.

The weekend brought news that coal buyers in China had been advised to cease buying Australian coal for the time being (both thermal and metallurgical) something our commodities expert regards as at least in part politically motivated. In this regard, Bloomberg has just run a story titled ‘Beijing-Canberra ties are running out of steam’, noting “China has suspended purchases of Australian coal, people familiar said, as it continues to tightly control imports of the fuel amid soured political relations with Canberra. Power stations and steel mills have been verbally told to immediately stop using Australian coal, and ports ordered not to offload it. The ban will have a greater impact on Chinese steelmakers than on electricity generation”.

On a day when the US bond market was shut and equities soaring, though of some note here the Nikkei failed to turn up to the global equity party (ending down a quarter of a percent). GBP is the other G10 outperformer, where one excuse being offered is that the new social distancing restrictions being enforced across large parts of England aren’t as draconian as feared, while hopes apparently still abound that a UK-EU trade deal can still be struck in time. A letter from the Bank of England to UK CEOs asking for information on the technical implications of negative interest rates, with responses required by November 12, doesn’t look to have moved the dial as far as the likelihood of this becoming reality anytime soon.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.