Coming in for landing in a heavy cross wind

Insight

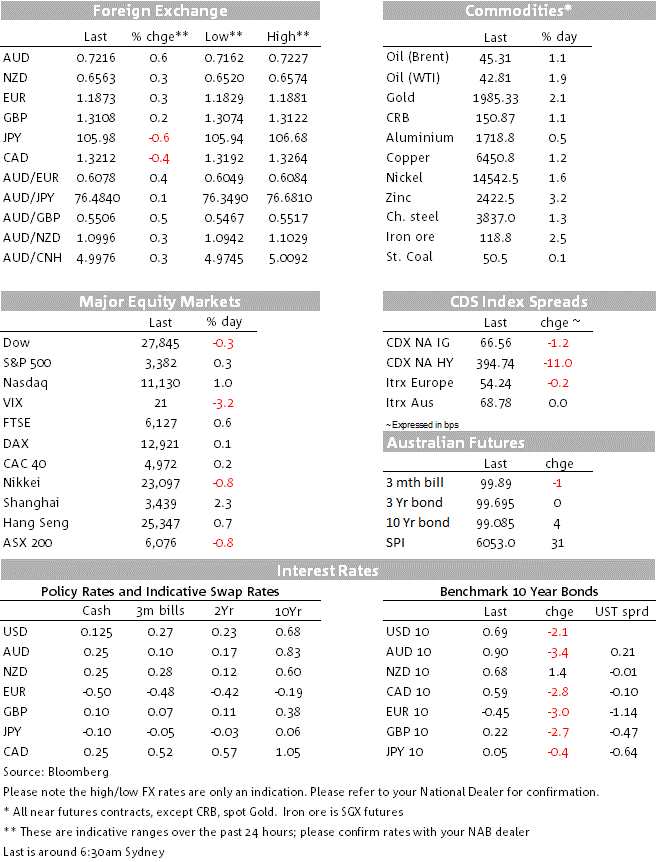

The US dollar continues to fall, pushing the Aussie dollar higher this morning.

What is happening here, something’s going on that’s not quite clear – Lionel Richie

It’s been onwards and upwards for US technology stocks at the start of the week, with consumer discretionary stocks (e.g., autos and other consumer durables) not far behind, seeing the NASDAQ close at a new record high (+1% on the day) and the S&P 500 up 0.3% to close just 4 points below its previous record closing high of 3,386 from 20 February.

Strength in technology stocks comes despite – or is it because of – the US administration’s announcement of a ban on 38 US companies in 21 jurisdictions from buying anything from Huawei (commercially available chips included) with President Trump declaring “We don’t want their equipment in the US because they spy on us”, that “We’ll end reliance on China” and “We’ll make our own drugs” (in which respect Trump claims that “We’re at a very close point” on vaccines). For the moment, the fact the phase-1 US-China trade deal remain in place, and will do while the two sides choose not to hold their six-month review that was to have taken place last weekend, is seen as overriding the building evidence of a technology cold war now underway.

Strength in consumer discretionaries comes even though there now seems little prospect of a fiscal stimulus bill before September at the very earliest and Pandemic Unemployment Assistance is now continuing at a lower weekly rate, the boost to incomes this previously provided being a key reason the consumer side of the US economy has been the strong point of the economic recovery to date. So go figure why this is Monday’s best performing sector of the S&P.

It’s the United States Postal Service (USPS) that is front and centre of the US political divide, in which respect House Democrats have set this Saturday for a vote on a bill that would prohibit operational changes to the Postal Service until well after the election and give $25 billion in additional funding to the agency. President Trump’s previous position on this was that he would only consider a USPS funding bill in conjunction with agreement on a broader fiscal support bill, which is of course nowhere in sight.

US bond yields have fallen by a few basis points (something our rates strategists noted yesterday is quite typical following a week in which yields rise significantly), 10-year Treasuries 2bps lower on the day to 0.69% and following slightly bigger falls in most European bonds yields (Germany and France both -3bp and Italy -6bps).

Lower US Treasury yields have meant that the JPY has managed to pretty much match gains for the more growth/risk sensitive currencies, the latter led by AUD which is up 0.66% on Friday’s close and back above 0.72 for the first time in ten days. Gains for AUD have been driven in part by specific demand for the AUD/NZD cross, which yesterday morning poked its head above 1.10 for the first time in two years.

The contrasting stances of the RBNZ and RBA remains the dominant factor driving NZD underperformance at present, with the economic implications of the NZ government’s evident ‘elimination’ strategy on COVID-19 providing auxiliary headwinds. Yesterday’s announcement of a delay to the NZ general election until 17 October was not a surprise and of no market consequence. The o/n high on the cross has been 1.1029 but has slipped back in late New York trade to be sitting bang on 1.10 as I type. The USD is broadly softer in conjunction with positive risk sentiment, DXY -0.3% and BBDXY -0.25%.

Economic news has been confined to the Empire (NY State) Manufacturing Survey, coming in much weaker than expected at 3.7 down from 17.2 in July (consensus was 15) and the NAHB (homebuilders) index which at 79 was above the 74 expected and 72 last time. Housing continues to shine as the brightest spot in the US economy at present, as should also be evident in tonight’s housing starts data.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.