NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

It’s all good news as far as the markets are concerned, pushing the Aussie dollar even higher.

https://soundcloud.com/user-291029717/aussie-rises-further-what-could-possibly-go-wrong?in=user-291029717/sets/the-morning-call

I’m a shooting star, leaping through the sky, Like a tiger defying the laws of gravity

I’m a racing car, passing by like Lady Godiva, I’m gonna go, go, go

There’s no stopping me – Queen

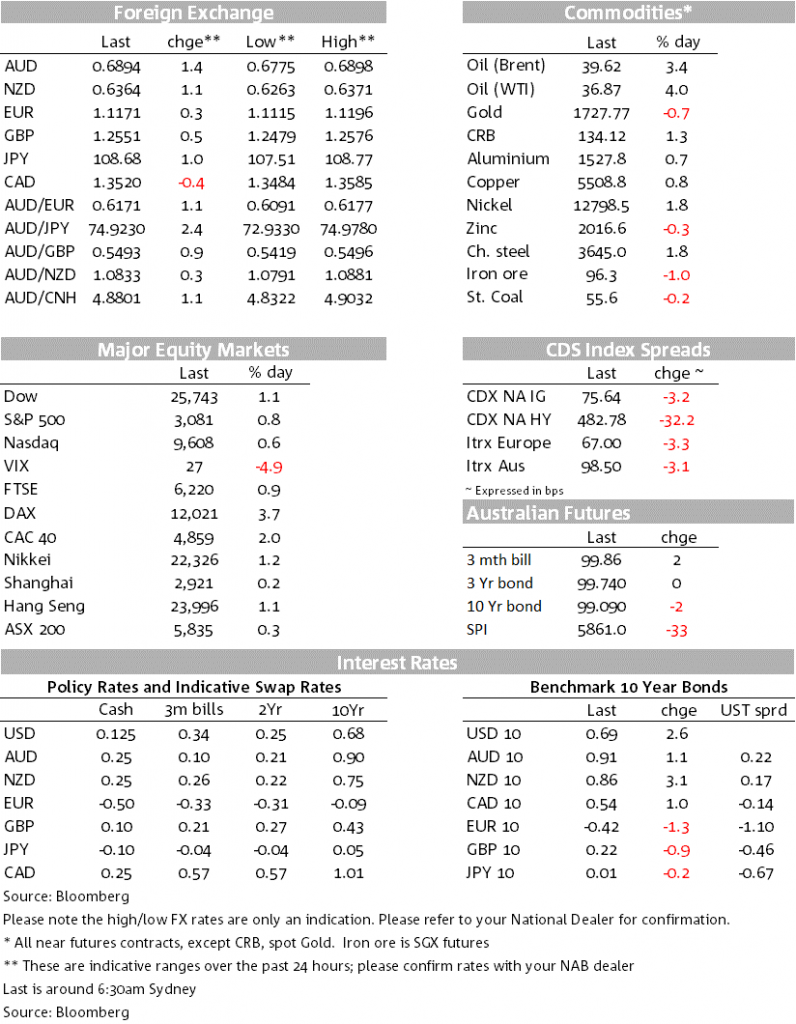

While main news outlets are running stories over the concerning civil unrest in the US, equity markets have continued their rebound propelled by fiscal and monetary stimulus and the hopes of economies reopening. The USD has lost more ground overnight with the AUD and NZD leading the charge while safe-haven currencies underperform. Rates markets remain moribund suppressed by central banks actions.

The equity index table is green across the board with major indices from APAC, Europe and the US all showing gains for the day. Gains in equity markets have been led by the a 3.75% gain in Germany’s DAX index –the market buoyed by the prospect of more fiscal stimulus as German Chancellor Merkel is trying to broker a second stimulus package for the economy worth as much as €100bn to help support the recovery. In the US, the rally is being led by cyclically-sensitive sectors, while small cap stocks continue to outperform, a classic sign of an improved macro outlook driving markets.

Investors remain on an optimistic mood, squarely focused on the prospect of economies reopening supported by COVID-19 stats that broadly speaking continue to suggest reopening plans remain on track. As an a example of the latter, NY Governor Cuomo warned that mass protests against police violence could accelerate the spread of C-19, but at the same time he confirmed he still plans to begin reopening New York City on Monday. The underlying trend of Europe is also falling, again supporting the notion that European cities should continue with their reopening plans.

The good virus news are more than outweighing the bad news. That said, given risk assets optimism, we think is important to keep an eye on negative trends that may have the potential to derail the buoyancy in risk assets. On this score is worth noting that Southern US states are still showing a steady increase in infections, Hong Kong extended virus-prevention measures after a new cluster of cases and Tokyo’s infections have also spiked. If these trends continue we could see the re-introduction of more severe restrictions.

History tells us that markets don’t tend to react negatively to these events. Markets are forward looking and inclined to focus on underlying macro themes and today’s theme is all about the COVID-19 recovery. US social unrest don’t tend to be longer lasting, so if history repeats itself, the current market assessment will be correct. That may well be the case, but only time will tell.

The other potential groove buster is of course the US-China tensions theme, but after President Trump’s statement on Hong Kong failed to reveal any drastic measures against China, the market is now leaning towards the idea that if the President Trump wants to win the November election, he can’t afford to rock the equity market or the economy with a further ramp-up in import tariffs or sanction against China.

Commodity linked currencies have continued to perform with the AUD and NZD leading the charge. The overnight chart for both antipodean currencies shows a nice steady upward slope with the AUD now essentially trading at its overnight high of 0.6897, I better hurry otherwise 69c will print before I finish! NZD now trades at 0.6371, also inline with it overnight high.

Yesterday the RBA left the cash rate and 3-year ACGB target unchanged at 0.25%.There were no surprises in the statement on asset purchases or liquidity operations and no changes to wording on policy. The Board promised that this“ accommodative approach will be maintained as long as it is required”, with the cash rate on hold until “progress is being made towards full employment and [the Board] is confident that inflation will be sustainably within the 2-3% target band”. Adding to the positive vibes and in line with Governor Lowe’s recent testimony, the policy press release noted the economy is better than had been feared, but the shape and speed of the recovery is highly uncertain. Accordingly, it was critical to restore household and business confidence about the health situation and their finances.

After a nearly 3% fall in the DXY index over recent weeks, the USD remains some 18% above our long-term PPP fair value estimate. With currency markets the weapon of choice to convey a macro view at present, JPY has been the weakest of the majors overnight, seeing USD/JPY up over 1% to Y108.68.

EUR and GBP gains have been more modest, in the order of 0.25-0.35% for the day. GBP saw a lift after The Times reported that “Britain is expected to signal compromise on fisheries and “level playing field” trade rules if the European Union backs off from its “maximalist” demands on regulatory alignment and fishing access, according to senior Brussels sources”. A final round of negotiations has kicked off before a summit later this month which will decide whether a free trade agreement can be in place instead of WTO rules from next year.

The rates market remains fairly dull, with the lack of movement during the risk-on backdrop no doubt influenced by central bank backstops, with their various QE programmes. The US 10-year Treasury rate is currently up 2bps to 0.68%, while European rates generally nudged down a little. NZ government rates were up 1-3bps across the curve yesterday, while the movement in swap rates was even less than that

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.