Online retail sales growth slowed in May following a fairly strong April

Insight

The Aussie dollar has fallen below the post GFC low.

https://soundcloud.com/user-291029717/aussies-new-low-and-us-helicopter-money?in=user-291029717/sets/the-morning-call

“There’s always a way, Yes, there’s always a way, To end this isolation, One step away from everyone” – Crowded House

US stock indices have recouped about half of Monday’s post-1987 crash record daily losses, the S&P currently +6.0% (but after having been up some 7% earlier in the session). The VIX still stands at an extremely elevated 75 (after hitting a high of 85 on Monday). New fiscal policy support measures being rolled out almost on the fly by various governments looks to be having positive impact on sentiment, albeit it comes alongside announcements of ever more draconian edicts aimed at enforcing social distancing regarding border crossing, gatherings (of ever-fewer people) and lock-downs being announced yesterday in parts of Asia (e.g. Malaysia from March 18-March 31). There are more reports of firms shutting factories and stores closing, with VW shutting down production in Spain, Portugal, Italy and Slovakia. However, VW’s CEO said most Chinese factories have now resumed operations.

Bond markets meanwhile look to be reacting (negatively) to the prospect of huge increases in government bond supply, with fiscal support measures being announced almost on the fly in various countries and currently amounting to as much (at this stage) as 4% of GDP or more (New Zealand yesterday, Hong Kong last week and now the United States). In the UK new Chancellor Sunak has just outlined a plan to guarantee up to £330b of business loans. The guarantees might not end up being needed, but that number represents an eye-popping 15% or so of GDP. In France, President Macron has said that no French company would be allowed to collapse, raising the spectre of widespread nationalisation (this, on a global scale, is one obvious caveat to investor enthusiasm to the ‘buy the big dip’ in terms of much more attractive equity valuations now presenting themselves in some sectors).

The ‘H’ word (helicopter) is now being bandied about, with respect to reports the US administration is looking at make cash handouts of $1000 or so to citizens within a matter of weeks. Note here that helicopter money (as originally termed by Milton Friedman but now referenced under the umbrella of ‘Modern Monetary Theory’ (MMT) amounts to central banks printing cash and handing it to the government to spend. Governments issuing debt to fund cash handouts, even if the central bank then buys that debt in the secondary market as is the case with the quantitative easing programmes of all central banks who have – or are – practising them, is not strictly MMT. The government debt still has – theoretically at least – to be repaid – even if some would regard this as largely semantics.

The Fed has announced it is restarting its Commercial Paper (CP) funding programme, buying CP at 200bps over the OIS rate, helping to provide a backstop to this important short-term funding market. The Bank of England also announced it would buy CP out to one year. Yesterday the Bank of Korea announced it was considering reactivating it US Swap line facility (which lapsed in 2010, as did the RBA’s and RBNZ’s) while the Bank of Japan yesterday supplied over $30bn to the local money market through 3-month and two-week repos. Additional measures from the RBA are awaited tomorrow.

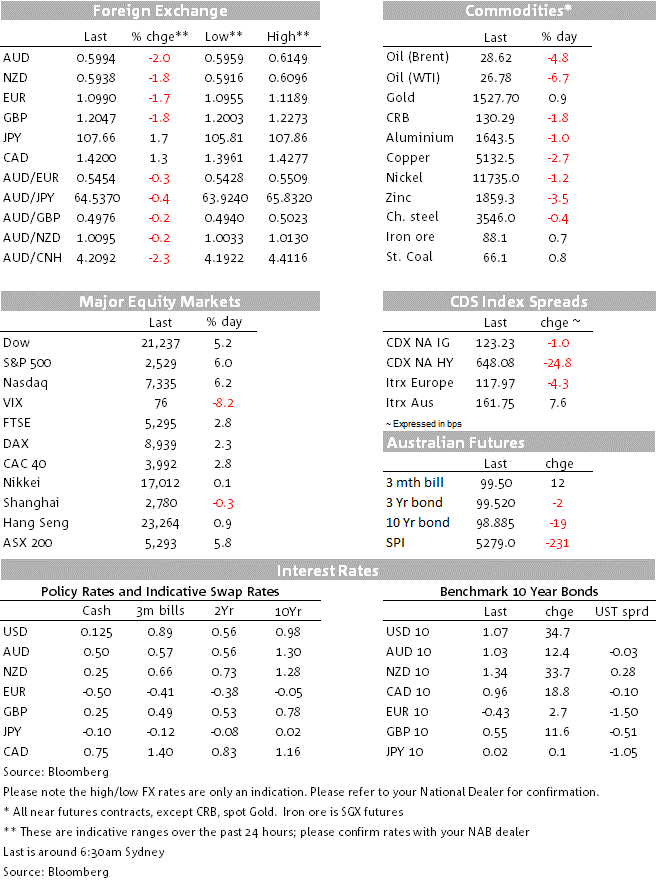

The AUD and NZD have both now cracked the 0.60 level, AUD/USD (low of 0.5959) for the first time since 11 April 2003 – so exceeding its post GFC low of 0.6009 – and NZD/USD for the first time since 19 May 2019. In the context of the highly elevated levels of risk aversion and depths to which commodity prices have fallen so far – oil in particular in the case of the AUD given the negative terms of trade shock this represents – we said last week that both antipodean currencies were on borrowed time above 0.60. The AUD/USD parity party champagne remains ion ice but it is not yet time to pop the corks (low of 1.0033 so far). Oil prices are off a further $1.50-2.0 and the LMEX index of base metals off 3%. Latest AUD and NZD weakness also has to be seen in the context of broad based USD strength (ex JPY an CHF) with the DXY dollar index back perilously close to its 99.91 February high (high of 99.83 overnight).

Economic data remains a second-order concern for markets and there wasn’t much reaction to a softer-than-expected US retail sales release, stronger than expected US industrial production, improvement in JOLTS job openings or the German ZEW survey plummeting in March, to its lowest levels since the European sovereign crisis.

NZ Current account, RBA’s Luci Ellis speaks in Sydney (10:00 AEDT) and the US tonight has housing starts and building permits

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.