A private sector improvement to support growth

Insight

Australia’s GDP numbers yesterday surprised many.

https://soundcloud.com/user-291029717/australia-joins-the-downturn-williams-on-the-new-normal-ecb-considers-its-options

This is our last dance, This is ourselves, Under pressure, Under pressure – Queen

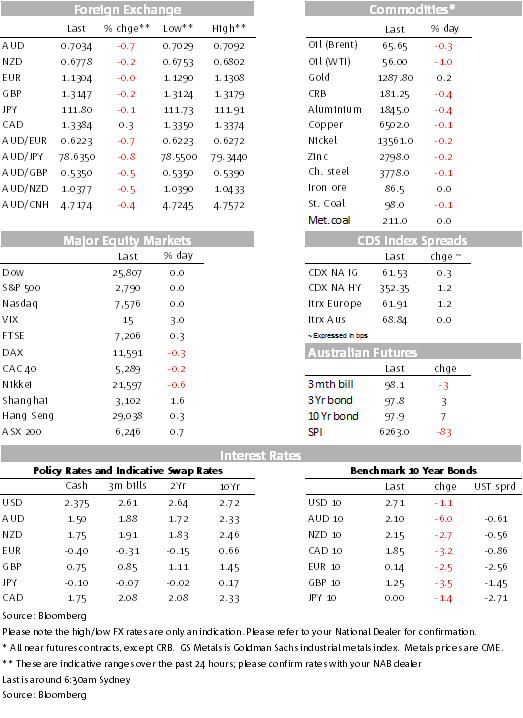

The cautious mood evident since the start of the new month continued overnight not helped by softer US data releases. US equities look set to close lower for a third consecutive day while UST yields are lower across the curve with the 10y tenor back below 2.70%. The USD is little changed and remains close to the top of its year to date range. AUD and CAD weakness following yesterday’s soft Australian GDP and a less hawkish Bank of Canada overnight have been partly offset by a stronger JPY with the latter benefiting from the cautious mood in US equity markets.

US equities are on course to end a third consecutive of negative returns as the market takes back some of the exuberant gains recorded since early January. Lack of new news on US-China trade negotiations has been one factor for the current cautiousness while softer US data releases pointing to downward revision to Q4 GDP and a soft US payrolls outcome (ADP 183k vs 190k exp.) on Friday have not help the cause either.

The US trade deficit hit a 10 year high in December, printing a bigger than expected negative number ($59.8bn vs 57.9bn exp.) and up by almost $10bn relative to November. The record print has done little favours to President Trump with the data suggesting his trade policy has been one factor contributing to the increase in the deficit. The President would of course argue that this is part of pain needed in order to achieve the gains of a better and more even trade relationship with China. That said, softness in the US equity market and a record trade deficit adds to the pressure on the US to seal a deal with China.

NY Fed President Williams, in a speech just given, reiterated the party line that the Fed can afford to be flexible and wait for the data to guide its approach. He added that the current Fed Funds rate of 2.4% “puts us right at neutral”. We note previous indications from the Fed suggested that the current rate was at the lower end of the range of neutral. If estimates of the neutral rate have fallen again, then there is less reason to expect the Fed to hike rates again this cycle.

So against a cautious equity backdrop, softer US data releases and a Fed that is more than happy to sit on the sidelines, UST yields have continued their steady downtrend evident since the start of the week with the 2y and 10y rate down another 3bps over the past 24 hours. Of note after closing last week at 2.76%, overnight 10y UST yields have moved below the 2.70% mark and now trade at 2.6897%.

In spite of the move lower in UST yields, the USD has remained buoyant in index terms with both DXY and BBDXY indices trading close to their year to date highs. From a relative basis the move lower in UST yields has been more than matched by larger declines in other core benchmark yields (10y UK Gilts -6 bps to 1.22% and 10y Bunds down 4bps to 0.1124%). Softer commodity currencies have also helped the USD while risk aversion in the air and lower UST yields have played into a stronger JPY. USD/JPY now trades at ¥111.80.

The AUD is at the bottom of the G10 scoreboard, down 0.85% over the past 24 hours and currently trading at 0.7028%. Much of the AUD decline came after yesterday’s softer than expected Q4 GDP print and after breaking through key support around 0.7050, the pair now has found some stability just above 0.7020. Yesterday’s Australia’s Q4 GDP growth printed at 0.2% vs. 0.3% pre-release downward revised consensus, details in the report were not that encouraging either with private consumption coming in at a subdued 0.4% (0.2 ppts GDP contribution). Earlier speech from Governor Lowe failed to move the dial on either RBA pricing or the currency. The Governor stuck to the view that the outlook has a balance of upside and downside scenarios even though much of their analytical work (a presented in Lowe’s speech) seems to have been devoted to downside risks, notably housing and consumption. Looking ahead much will depend on the consumer outlook with January’s retail sales today (market looking for a rebound from the negative December print) an important indicator while next week’s NAB survey along with its sub employment indices are also going to be important for RBA pricing expectations and near term fortunes for the currency.

The Bank of Canada left its policy rate unchanged and softened its tightening bias. The previous language of seeing the need for rates to rise over time was replaced by a comment that borrowing costs will remain below neutral for now and there is increased uncertainty about the timing of future rate increases. A softening in the tightening bias was expected by the market but CAD still weakened after the announcement, with USD/CAD up 0.64% to 1.3425. AUDCAD is little changed at 0.9434.

Bloomberg reported that the ECB, at its policy update tonight, is poised to cut its economic forecasts by enough to justify another round of concessionary loans to banks, according to unnamed sources – although a full announcement on new loans may not come until a later meeting. Inflation and GDP forecasts will be extensively cut for 2019, while the inflation outlook will be cut through 2021. The report aligns with market expectations ( and our own) but caused a spike down in EUR to as low as 1.1286, before bouncing back. EUR now trades at 1.1310.

Commodities were led lower by oil after a bigger-than-expected rise in US crude stockpiles. The American Petroleum Institute reported US inventories increased by 7.29m/b last week.

– AU: GDP (q/q%), Q4: 0.2 vs. 0.3 exp.

– US: ADP employment change (k), Feb: 183 vs. 190 exp.

– US: Trade balance ($b), Dec: -59.8 vs. -57.9 exp.

– CA: Bank of Canada rate (%), Mar: 1.75 vs. 1.75 exp.

– AU AiG Perf of Construction Index (Feb), Trade Balance (Jan) and Retail Sales (Jan)

– NZ Wholesale Trade (4Q)

– CH Foreign Reserves (Feb)

– JN Leading Index CI (Jan P)

– UK Halifax House Prices (Feb), BOE’s Tenreyro Speaks in Glasgow

– EC Employment and GDP (4Q F), ECB Policy Meeting, ECB’s Draghi press conference

Re ECB we think forecast downgrades are in the offing and although forward guidance is likely to be unchanged, we think there is a risk Draghi will deliver a dovish interpretation at the Press Conference. We also expect an acknowledgement of TLTROs discussion, but we don’t anticipate an official announcement at this meeting.

– US Jobless Claims, Fed’s Brainard Speaks on Economy and Monetary Policy Outlook

– CA Building Permits (Jan), BoC’s Lynn Patterson speaks

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.