NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US unemployment registrations have added another 4.4 million, European PMIs hit record lows and the EU failed to reach an agreement on how to fund a recovery package for Europe.

We’ve been broken down, to the lowest turn, bein’ on the bottom line sure ain’t no fun…

(hold on) hold on,(hold on) ooh ooh aah,the only way is up, baby, for you and me now

the only way is up, baby, for you and me now – Yazz & the Plastic Population

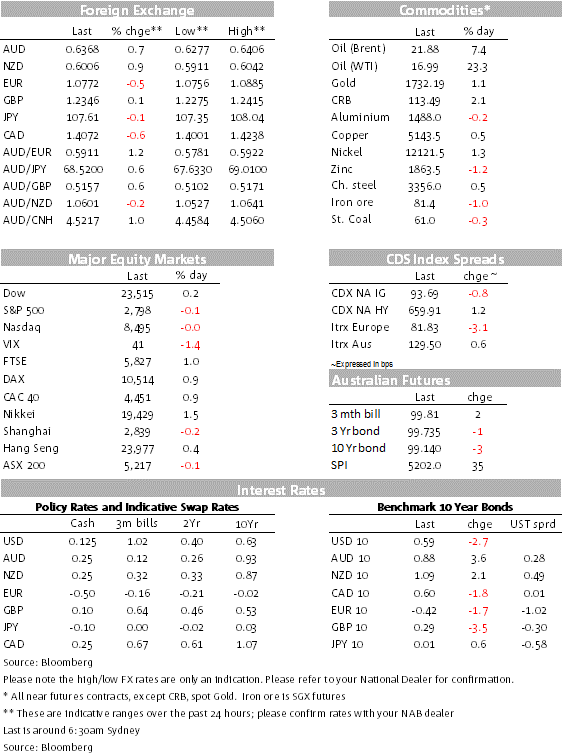

Dire economic data releases have been ignored by the market, essentially treated as old news and in a mixed night for equities, further gains in oil sees energy shares outperform on both side of the Atlantic ( for oil clearly after being broken down…the only way is up baby!). The move up in oil has also benefited commodity linked currencies while the euro underperformed. 10y Italian BTPS outperform for a second day in a row and 10y UST yields are little changed.

The Global flash PMIs for April have confirmed the shocking economic impact COVID-19 measures are having on economies around the globe. A few themes are worth highlight, the decline in the PMI readings are now exceeding the lows seen during the GFC, this time the service sector is bearing the brunt of it and importantly too, when we think about the recovery Asian economies appear to be doing better, so far printing higher lows. China is already on the way up while it remains to be seen if the April readings will define the lows in Europe and the US. The services indicators ranged between 12-16 for the UK, Germany and the euro area and came in at 27 for the US. That the figures weren’t at the theoretical limit of zero across Europe simply reflected essential services being allowed to remain open (for more details see event round up below).

The weekly jobless claims reading narrowly beat market expectations by printing at 4.4m compare to the 4.5m pencilled in by economists. But that’s pretty much where the good news ended, the COVID-19 crisis has seen jobless claims rise to 26m over the past 5 weeks, during the GFC it took 61 weeks for the cumulative claims to reach a similar number. The COVID-19 instant US recession means that April US unemployment could print close to 20% and this in unlikely to be the end of it with more job losses still expected over coming weeks.

As noted on the top the email, the equity market took the bad economic news in its stride. Regional European equity indices ended with gains around the 1% mark and after and up and down session, the S&P 500 and NASDAQ have closed marginally in the red ( -0.05% and -0.01% respectively). US equites started the overnight session on a good note gaining as much as 1.6% at one point. as much as 1.6%. The rally lost momentum after the FT reported that a Chinese trial showed that the drug remdesivir, developed by Gilead Sciences, did not improve patient’s condition or reduce the pathogen’s presence in the bloodstream. This formal trial – although terminated due to low enrolment – contradicted previously released “studies” that provided some hope that the anti-viral drug was effective in relieving symptoms ofCOVID-19.

The energy sector was a clear outperformer up over 3% in Europe and the US. The rebound in oil prices has been the clear catalyst. It is hard to attribute the gains in oil to any specific news. But after trading in negative territory, some focus appear to be given now the rapid US production decline. WTI is up 22% and Brent is +16.8% .

The USD is little changed in index terms, DXY now at 100.5 and BBDZY at 1260.9. But looking at G10 currencies commodity linked currencies have been the outperformers. NOK leading the charge up 1.21% followed by NZD and AUD up 1% and 0.75% and now trading at 0.6008 and 0.6370 respectively. Yesterday we published an update on the NZD/ AUD cross, highlighting that it faces macro tailwinds, with the more severe lockdowns in NZ than Australia causing a deeper economic hole to fill, and with RBNZ QE policy on a much more likely aggressive path than the RBA, amongst other factors. The cross trades at 1.0605 this morning.

The Nikkei reported that the BoJ will next week discuss allowing unlimited government bond purchases, while keeping the 10-year target to zero percent. For some reason this caused a temporary spike in USD/JPY, briefly taking it above 108. In practice, this policy decision would have no impact on the market at the moment, with the Bank achieving the yield target easily. However, the report noted the BoJ will also double the purchase targets for commercial paper and corporate bonds, which might keep yields on those products lower than otherwise. USD/JPY is back down to 107.60.

EUR and CHF have been the two weakest currencies overnight. The Swiss National Bank reported a record loss of CHF38.2b reflecting massive losses on its stock portfolio. The SNB has been actively intervening in the market to prevent CHF strength against EUR. EUR slipped below 1.08 overnight, possibly reflecting some disappointment that the EU has yet to agree on a longer-term rescue fund.

The EU endorsed the previously announced short-term plan worth €540 to support businesses and economies. There was also apparently agreement on the need for a long-term recovery package worth 5-10% of GDP, but disagreement on the form of funding – with Germany, Austria and the Netherlands insisting that any bailout comes in the form of loans than grants. However, there is some hope that a compromise solution can be agreed next month.

Italian 10y BTPS rallied with their yields declining 9.3 bps to 1.98%, meanwhile in the US, moves in UST yields have been relatively subdued with the curve showing a flattening bias. 10y UST yields now trade at 0.60%, little changed on the day.

US Covid -19 cases rose by 2.5%, the slowest rate this month with the virus bad news now clustering in the west as California reports the most fatalities in one 24-hour period, and Texas cases rose for a third day. Meanwhile New York hospitalisation in New York were flat, but still at an elevated level. Spain reported the greatest number of new cases and fatalities in almost a week, while Italy saw recoveries from the coronavirus overtake new infections for the first time.

GE: GfK consumer confidence, May: -23.4 vs. -1.8 exp.

GE: Manufacturing PMI, Apr: 34.4 vs. 39.0 exp.

GE: Services PMI, Apr: 15.9 vs. 28.0 exp.

EC: Manufacturing PMI, Apr: 33.6 vs. 38.0 exp.

EC: Services PMI, Apr: 11.7 vs. 22.8 exp.

UK: Manufacturing PMI, Apr: 32.9 vs. 42.0 exp.

UK: Services PMI, Apr: 12.3 vs. 27.8 exp.

US: Initial Jobless Claims (k), Apr 18: 4427 vs. 4500 exp.

US: Markit manufacturing PMI, Apr: 36.9 vs. 35.0 exp.

US: Markit services PMI, Apr: 27.0 vs. 30.0 exp.

US: New home sales (k), Mar: 627 vs. 644 exp.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.