We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

US 10 year Treasury yields hit a 14 month high overnight, as the US dollar rose higher.

https://soundcloud.com/user-291029717/biden-the-builder?in=user-291029717/sets/the-morning-call

Easy money, Rain it down on the wife and the kids, Rain it down on the house where we live, Rain it down until you got nothing left to give, And rain that ever-loving stuff down on me” – Nick Cave & The Bad Seeds

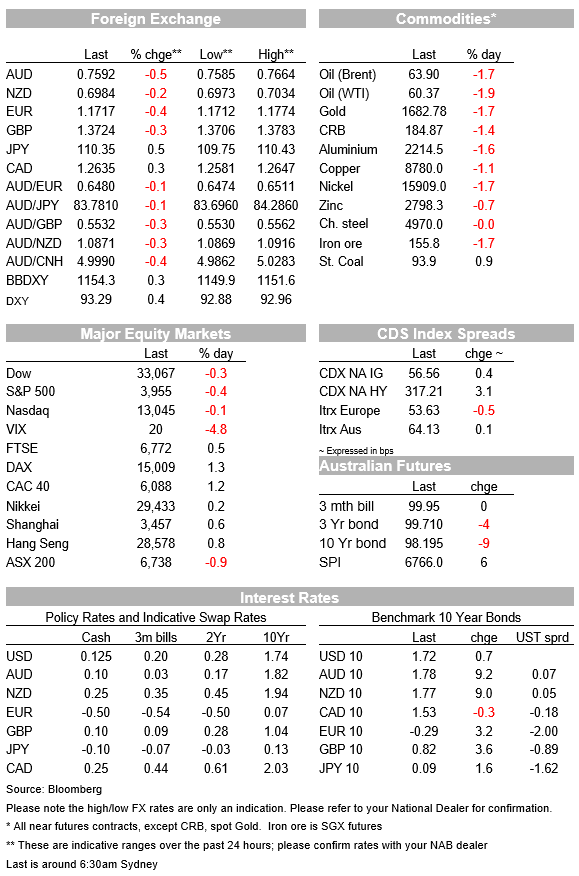

US bond yields were smartly higher in Asia yesterday and rose further in offshore markets, but yields have since peeled back to be below where we left them yesterday, lifting US equities off their lows but not quite into the green. The USD has also pared a little of its gains, after the BBDXY index had earlier risen by 0.4% to above its prior year to date highs. Immediate market focus is on the detail of President Biden’s infrastructure and other spending ambitions – and their proposed funding – when he speaks in Pittsburgh later today.

Its tempting to attribute the latest rise in US Treasury yields, to new post-pandemic highs of 1.775%, to the eye-popping jump in the US Conference Board’s Consumer Confidence reading, to 109.7 from 91.3 and 96.7 expected – testament to the power of more free money about to rain down on US households and reportedly the biggest monthly leap since the fall of Baghdad which ended the 2003 Gulf War – though the fact is the highs for yields were in place several hours before the release. Yields did pop a little higher on the data but soon resumed their fall-back off their early-day highs.

We wonder whether month/quarter end factors have come into play here, whereby so called balanced funds, who have seen their equity share of assets rise in value this quarter and their bond portfolios shrinking, are a factor behind the recovery in bond prices, though other than those seeing the flow, no-one can say for sure. It does though appear that the latest back up in bond yields – from 1.6% less than a week ago to now comfortably above 1.7% and which has been met without a murmur of concern from Fed officials – has been responsible for equity slippage, together perhaps with lingering concerns regarding the fall-out from the Archegos Capital debacle. Thankfully there have been no new horror stories on this front regarding bank losses overnight, save for Mitsubishi UFJ admitting it may have taken a hit in the order of $300mn.

As well as the rise in US consumer confidence in the US, we also saw industrial and economic confidence lift in the Eurozone according to the latest European Commission surveys (Industrial Confidence to 2.0 from -3.3 and Economic Confidence to 101.0 from 93.4, though Consumer Confidence was unchanged at -10.8). The virus-related news flow from the Eurozone has not been great, with Germany announcing it is suspending the routine use of the Oxford Astra Zeneca Covid-19 vaccine for people under 60 because of the risk of rare blood clots.

Currencies are in a sea of red against the USD, save for a marginal gain in the NOK despite weaker oil prices (latter following the re-opening of the Suez Canal and against the stronger USD backdrop). AUD is at the bottom of the G10 pack after staging a decent rally during our day yesterday (to back above 0.7650). Its o/n low has been 0.7585, so still little above the February 2 and March 25 lows of 0.7564. USD/CNH, which rose above 6.58 on Monday evening, has been relatively steady in an effective 6.57-6.58 range in the last 24 hours. A mixed performance from Emerging Market currencies elsewhere, with the Brazilian Real up 0.4% and Mexican Peso +0.25% while the Indian Rupiah and Turkish Lire and both off by more than a percent since Monday’s close.

Finally In Fed speak, and in front of tonight’s ADP employment report and Friday’s all-important non-farm payrolls, Atlanta Fed President Raphael Bostic says “We could see a burst of activity and performance coming into the summer which could lead us to see even more robust recovery,” and that, “A million jobs a month could become the standard through the summer.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.