Online retail sales growth slowed in May following a fairly strong April

Insight

The US and China will sign the phase one trade deal tonight.

https://soundcloud.com/user-291029717/big-beautiful-monster-of-a-deal-day?in=user-291029717/sets/the-morning-call

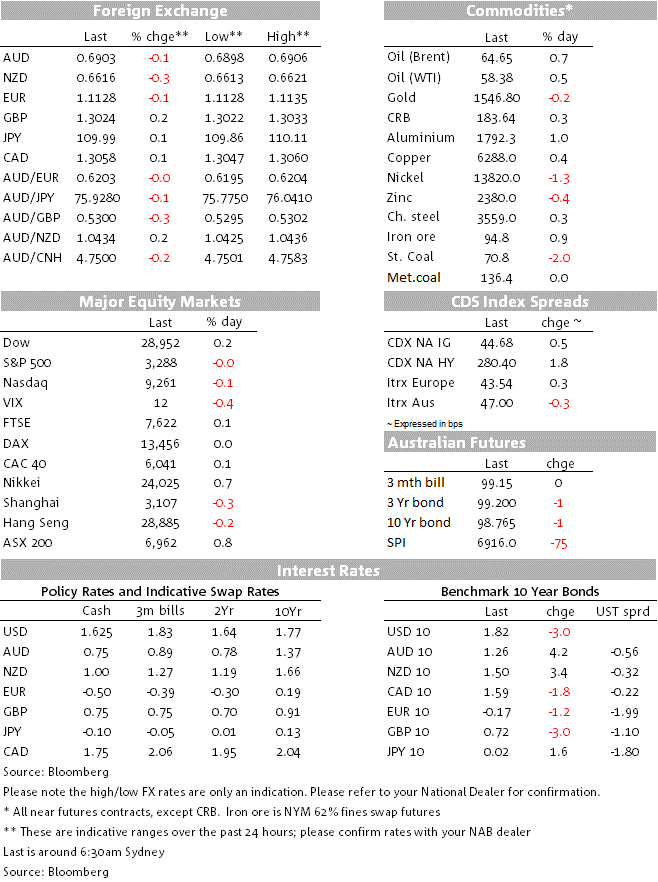

A big day today which sees the US and China signing the phase 1 trade deal. Importantly though we should not expect further tariff relief until after the November Presidential elections, suggesting that today’s agreement is probably as good as it gets for 2020. Market moves have been relatively subdued ahead of the signing. Lower-than-expected US Core CPI drove a small fall in global yields (US 10yr Treasury -3.0bps to 1.82%), and kept alive the possibility the Fed may need to cut on inflation alone despite a more optimistic 2020 (Bloomberg WIRP has around a 90% chance of a cut by Dec 2020). Equities rose (helped by strong Q4 earnings by JP Morgan and Citigroup), but reversed gains after headlines of not expecting further tariff relief until after the elections. FX was little moved with the USD (DXY) unchanged at 97.35, with EUR -0.1%, USD/Yen +0.1% and GBP +0.3%. The AUD was little moved, -0.1% to 0.6903. One notable FX mover was EUR/CHF which fell 0.5% after Switzerland was put on the US Treasury’s currency manipulator watchlist.

Details of the deal are now starting to emerge with Politico reporting that China has committed to increase imports by $200bn over two years, including $75-77bn in manufacturing, $50bn in energy and $40bn in agriculture (see Politico/SCMP for details). The deal will also include provisions for IP, forced technology transfer, the currency and market access to certain sectors of the economy. Yesterday the US Treasury also formally removed China from its list of currency manipulators. Tempering some of the positivity early this morning were headlines of not expecting further tariff relief until after the November Presidential elections, while there is also a push by the EU and Japan to have tougher WTO subsidy rules. Importantly for China though, the deal will allow it to re-focus on its domestic economy which should reduce fears of a slowing economy.

Indeed Chinese trade data yesterday added to the growing positivity on China and the global economy. The data revealed larger than expected increases in both exports (+7.6% y/y) and imports (+16.3% y/y). While favourable base effects created a flattering y/y comparison, the trade data paint a picture of a Chinese economy which as stabilising towards the end of 2019, consistent with the message from the PMIs recently.

The US CPI was the major piece of data overnight, coming in lower than expected. Core CPI was 0.1% m/m against 0.2% expected, with the annual rate in line at 2.3% y/y. While much of the weakness was driven by the volatile components of used cars (-0.8% m/m) and airfares (-1.6% y/y), the data does highlight inflation remains subdued in the US. Mapping the CPI to the Fed’s preferred PCE measure suggests Core PCE inflation has slowed to a 1.5% pace, down from 1.7% in October and 1.6% in November, and well below the Fed’s 2% inflation target. With inflation continuing to under-club, the risk remains the Fed may need to cut on the inflation outlook alone even if the growth outlook has become more positive. UBS is one bank tipping the Fed may need to cut three times in 2020. Markets currently price around a 90% chance of a rate cut by December 2020. US yields moved 2-3bps lower on the news with US 10yrs now 1.8161%.

The NFIB survey was also out overnight with sentiment falling unexpectedly to 102.7 from 104.7. Interestingly the sub-indexes showed some easing in labour market pressures with a sharp fall in “cost of labor single most important problem”, while the earlier released jobs hard to fill also fell.

Q4 earnings kicked off last night with JPMorgan and Citigroup reporting strong profits. JP Morgan’s profits rose 21% and Citigroup 15% lead by a jump in revenue in the corporate and investment bank; investors liked it with their shares up 1.5-2.1% respectively. JP Morgan CFO noted that “the U.S. consumer remains in very strong shape, both from a credit perspective and spending sentiment,” and that among corporate clients “sentiment is at least certainly better than it was six months ago. So we have a constructive outlook as we’re heading into 2020.” Despite the better earnings, equities overall were flat with Wells Fargo disappointing with its stock down 4.5% and the broader S&P500 tempering positivity after headlines of not expecting further tariff relief until after the elections.

The Swiss franc strengthened after the US Treasury added to its watchlist of those it accuses of currency manipulation. EUR/CHF fell 0.5% to its strongest since April 2017 at 1.0765. The Swiss govt countered that they are not steering the CHF for competitive gain and does not in any way engage in manipulation of its currency to prevent adjustments to the balance of payments or gain unjustified competitive advantage.

There is no data scheduled for the Australian calendar with all eyes instead on Chinese Credit figures, German Q4 GDP and UK CPI. The most market moving release could be the UK CPI given markets are pricing a 50% chance of a BoE rate cut at the upcoming January meeting. The consensus for CPI has a large left tail, implying downside risks to the consensus.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.