Online retail sales growth slowed in May following a fairly strong April

Insight

What did the RBA’s Guy Debelle say yesterday to spur the Aussie dollar on so much?

https://soundcloud.com/user-291029717/black-hole-brighter-than-mays-future

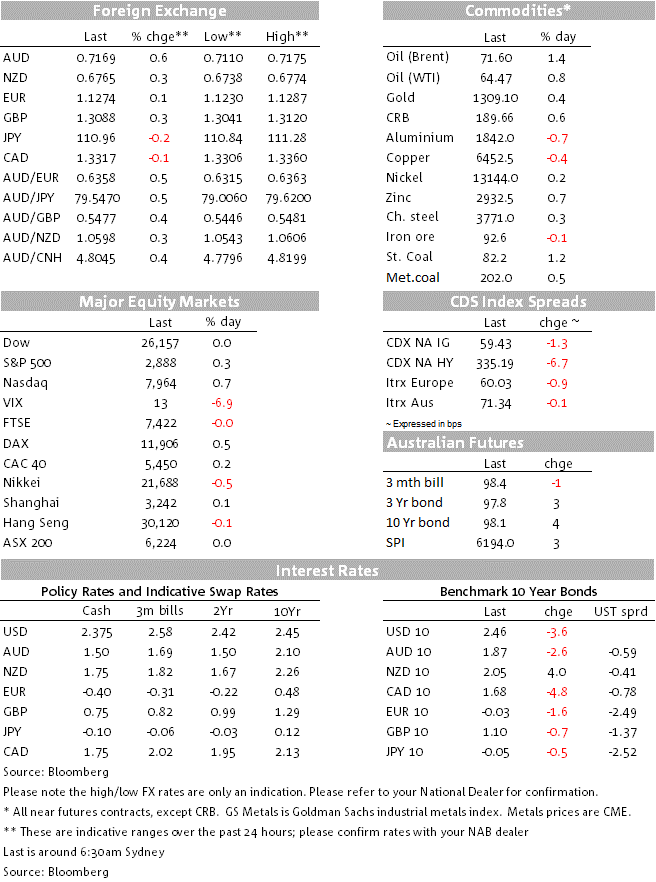

For all the event risk that lay ahead when the Australian market left for home yesterday, the standout feature of markets since then is the relative strength of the AUD, finally managing to sustain a break above important technical resistance around 0.7150, pushing on to a high 0.7175 and so threatening to move onto a ‘72 handle’ as early as today. The current levels bring AUD almost exactly into line with our own short term fair value estimate, AUD/USD having been trading consistently below since early February.

Potentially capping gains near term could be decent interest from Australian importers if we do creep onto that 0.72 level. We are also on guard for some potential weakness linked to the forthcoming federal election, which The Australian newspaper is telling us will be called by PM Scott Morrison today to take place on May 18th.

As for the underlying source of AUD gains in the last 18 hours or so, RBA Governor Guy Debelle takes most of the credit, having put the market further off the already fairly weak scent of an RBA rate cut as early as the next (May) meeting. Debelle made clear (in his post speech Q&A) that the tweaks to the last paragraph of the post-April RBA Board meeting statement was to buy time to get a better handle on where the economy was really at given, and as he stressed in the speech, the ongoing tension between GDP related data (weak) labour market indicators (strong) and business survey indicators that appeared to lie somewhere in between. Market pricing for a May rate cut came out to about 12% post Debelle, from about 24% heading in to his speech.

NAB hasn’t changed its RBA view post-Debelle, still expecting two rates cuts in the second half of 2019 with a first one currently pencilled in for July. The March labour market report on April 18th and Q1 CPI on the 24th are the next big RBA-relevant domestic data points.

Elsewhere in FX, not too much as happened on net despite some volatility surrounding the ECB, US CPI and FOMC Minutes. The EUR slipped a little after ECB President Draghi re-iterated the more downbeat assessment of the Eurozone economy, with the forward guidance on rates – on hold “at least through the end of 2019” kept unchanged in what was an interim rather than policy setting meeting.

Draghi said that the Governing Council would evaluate measures to mitigate the effects of negative interest rates at the June meeting, but without creating a presumption they would act (e.g. by ‘tiering’ the Deposit rate). In fact, Draghi suggested that there were bigger structural issued to be dealt with in the banking system, in particular the need for consolidation and scale that would enable a bigger embrace of technological advancement in the sector. The detail of the promised new TLTROs would come in a future meeting, Draghi said (they are not scheduled to begin before September).

As for the impact of US events, the otherwise negative US dollar impact of weaker than expected core-US CPI print at just 0.1% was more than offset by the drop in the Euro as soon as Mr Draghi started speaking – at exactly the same time as CPI. The clean read of CPI therefore only came through in the rates market where 10-year Treasury yields fell from 2.51% to around 2.47%.

The 0.1% core CPI print (though a ‘high’ 0.1%, being 0.148% unrounded) was due to particular weakness in clothing prices, down 1.9%, but which was reportedly due at least in part to new sampling methodology (increased reliance on one large – unnamed – department store apparently). Used car pieces also showed a big fall, as did airfares, the latter probably linked to the timing of Easter. In contrast ‘owner equivalent rents’ – the biggest CPI contributor – was relatively strong. As such, the overall core reading hasn’t been taken completely at face value.

FOMC Minutes have come and gone without a great deal of fanfare, this being from the March meeting where the median ‘dots’ were lowered to show no change in rates this year. That said, there was a consensus view that the evident weakness in early-year growth was not expected to persist and that there were considerable uncertainties surrounding the outlook (implying therefore that patience wouldn’t last indefinitely). US yields initially ticked up by a basis point or so but have since retraced, while the USD sits marginally higher than pre-Minutes levels.

As for Sterling, the EU Summit is ongoing, where UK PM’s May’s request for an Article 50 extension to no later than June 30th looks to have fallen on deaf ears, the Council reportedly debating whether to offer an extension for 9 months (through end -2019) or through March 2020, replete with conditionality about the UK promising to be a good EU citizen and not opposing majority views on EU business. GBP/USD is up by about ¼% just below $1.31 in anticipation of a 9-12 month extension being granted. UK output related economic data meanwhile was relatively strong, though inventory building in front of a potential no-deal Brexit looks to be part of the reason and so less relevant as a result.

US equities have closed with gains ranging from just 0.03% for the Dow to 0.35% for the S&P500 and 0.69% for the NASDAQ. IT and real estate are the best performing sub-sectors in the S&P.

In commodities, oil can continue to do no wrong despite a reported 7.03 million barrel rise in crude inventories last week as reported by the EIA, seemingly thanks to a corresponding draw in gasoline stocks of 7.71 million barrels. WTI crude is up another 49 cents to $64.47 and Brent by 99 cents to $71.60 – its highest close since 7th November last year.

UK: GDP (3m/3m%), Feb: 0.3 vs. 0.2 exp.

EC: ECB deposit facility rate, Apr: -0.4 vs. -0.4 exp.

US: CPI (y/y%), Mar: 1.9 vs. 1.8 exp.

US: CPI ex food and energy (y/y%), Mar: 2.0 vs. 2.1 exp.

EU Brexit-related Summit outcome expected anytime

Scott Morrison to announce an election for May18th, media suggests

China CPI (expected 2.3% from 1.5%), PPI (expected 0.4% y/y from 0.1%)

RBA Deputy Governor Guy Debelle speaks again today, but on `Progress on Benchmark Reform’ at the ISDA 34th Annual General Meeting in Hong Kong (appearance via video conference from Sydney).

France and Germany have final march CPI, US has PPI and weekly jobless claims

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.