Online retail sales growth slowed in May following a fairly strong April

Insight

It’s far from a quiet day in markets.

https://soundcloud.com/user-291029717/bond-yields-and-equities-dive-on-bad-economic-news-from-china-and-germany?in=user-291029717/sets/the-morning-call

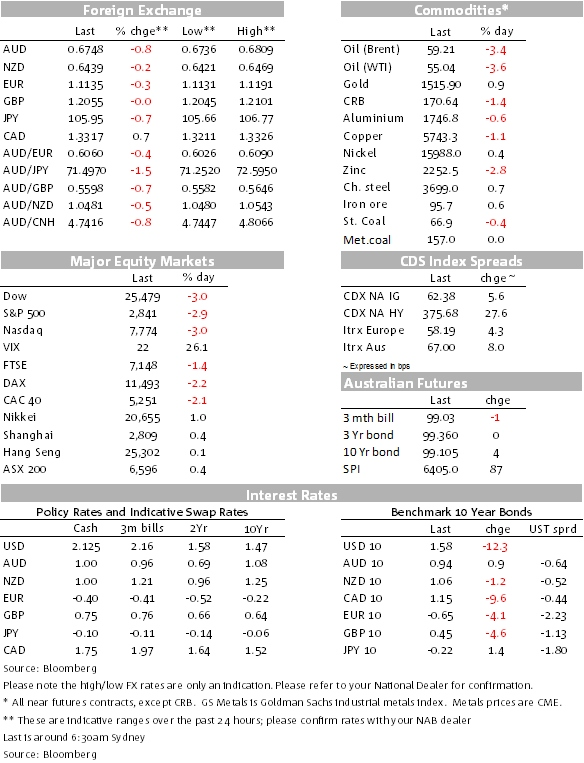

The bounce in risk sentiment and related asset and currency market moves, following Tuesday’s decision by President Trump to delay implementation of the 10% tariff rate on about half of the $300bn worth of additional Chinese imports until December 15th, has proved to be very much of the ‘dead cat’ variety. US stocks have closed down 3%, the US and UK 2yr/10yr curve spreads have briefly inverted for the first time since 2007 and the 30-year US bond yield has made a record low at 2.02%. AUD/USD has given back all of Tuesday’s Trump tariff-related rally and is vulnerable to further weakness this morning if the unemployment rate moves up to 5.3% or higher.

US (and UK) curve inversion was making headline news on the BBC World Service 5am bulletin. On the basis that whenever the weakness of the Australian dollar features on the front pages rather than business section of the newspapers here it is a sure-fire signal to buy it with your ears pinned back, now might be the rime to think that we should be doing the same in terms of either buying two-year Treasuries or selling 10-year Notes.

Not so fast. Certainly our interest rate strategists don’t think we have yet seen the lows for longer-dated US bond yields, in world where now almost 30%, or $15.8tn, of the widely followed Bloomberg-Barclays Global Aggregate bond index was negative yielding as of two days ago. And as BNZ’s Nick Smythe reminds us today, inversion in the 2/10s spread has preceded each of the last five US recessions with a lead time of between 11 and 23 months and with only one false signal, in 1990 at the time of the LTCM/Russia debt crisis.

There hasn’t been a particular catalyst for the overnight sell-off in risk-assets and safe-haven bond and currency bid. US stocks opened about 1% lower following the lead from Asia and Europe, and then leaked lower throughout the session. There’s little doubt though that the weaker than expected slate of China July activity readings set the ball rolling in the APAC session yesterday and that the -0.1% German Q2 GDP print, though as expected, contributed something to the malaise.

China’s annual industrial production growth of 4.8%, down from 6.3% in June, encompassed a mere 0.2% seasonally adjusted monthly rise, the weakest since mid-2015. The argument that the weaker the Chinese numbers the stronger will be the domestic policy stimulus is starting to wear a bit thin, especially given the soft credit numbers that preceded yesterday’s release.

US stock indices closed with the S&P 500 down 2.93%, the Dow -3.05% and the NASDAQ -3.02%. All S&P sub-sectors closed in the red, led by energy on falling oil prices (-4.1%) and financials (-3.6%) the latter a direct reflection of the further pressure on banks’ net interest margins as a result of latest curve flattening/inversion

Bonds see the US Treasury 10-year note yield -12.4bps and the 2-year -8.7bp with, as of now, both yields identical at 1.58%. Earlier Wednesday 10-year German Bund yields lost another 4.1bps to a new record low of -65bps and 10-year gilt yields -4.6bps to 0.45%.

In FX anyone trading AUD/JPY in recent days – the G10 risk sentiment weapon of choice – has either made a lot of money or may have to be contemplating a career outside currency markets. The cross is down over 1.5% in the last 24 hours, having been up over 2% on Tuesday. The AUD/USD loss of 0.76% (to ~0.6750) has been eclipsed by both NOK (-1.2%, on lower oil) and SEK (-1.0%, despite Sweden printing slightly stronger than expected CPI numbers). The JPY stands proud at the top of the G10 leader board, USD/JPY down 0.8% to ¥105.86.

Incidentally, NAB has just published a note on our updated AUD/USD and AUD cross rate forecasts with an accompanying Podcast. If you have not received it but would like to, please email either Rodrigo or myself at the addresses below

The offshore Yuan (CNH) is back at 7.05 overnight having briefly traded back below 7.00 in the wake of the ‘good’ tariff news and will doubtless be a broader currency market focal point today. .

Finally, GBP is unchanged against the USD over the 24 hours. The speaker of the House of Commons, John Bercow, whose interpretation of parliamentary procedure is seen as key to MP’s looking to thwart Boris Johnson, said he thought it was possible for MPs to stop the UK leaving without a deal at the end of October. Johnson himself claimed a “terrible collaboration” between MPs opposed to a no-deal Brexit and the EU, blaming those MPs of jeopardising his chances of getting a deal.

Betting markets have pared back the chances of a no-deal Brexit this year slightly, to a still uncomfortably high 40%. Also to note is that US House Speaker Nancy Pelosi has threatened to block any future bilateral trade agreement between the U.S. and the U.K. if Brexit puts at risk the Good Friday Agreement that brought an end to the conflict in Northern Ireland.

The July labour force survey is due at 11:30 AEDT. Our forecast is for employment to increase by 15k after a 1k rise in June. The unemployment rate is forecast to tick up to 5.3% from 5.2%. The weaker labour market is consistent with the deterioration in our labour market index, which summarises the demand for labour from business surveys, job vacancies and expectations of unemployment.

Before this, RBA Deputy Governor Guy Debelle is speaking on “Risks to the outlook” at 9am at the Risk Australia Conference in Sydney. He will cover the same ground as Governor Lowe’s parliamentary testimony and we will be most interested in his view on the risks to global growth from the worsening trade conflict between the US and China.

US retail sales for July is expected to show continued growth, while industrial production, also for July, should show a 0.4% decline in an already-bruised manufacturing sector. The first two regional readings on manufacturing for August from the Empire State and Philly Fed are also out tonight.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.