“Take a chance on a rumor; Heard from a friend; That something is gonna change; It’s creepin’ up slowly; She’s taken me over; It’s turning me on”, Taxiride 2002

‘Creepin’ Up Slowly’ was the hit single by Australian rock band Taxiride with the lyrics echoing recent expectations that US inflation is set to creep up. While that may be the case on the annual y/y figures due to base effects, the Core CPI for December showed little in the way of inflationary pressure, while the Fed’s Brainard pushed back on taper talk.

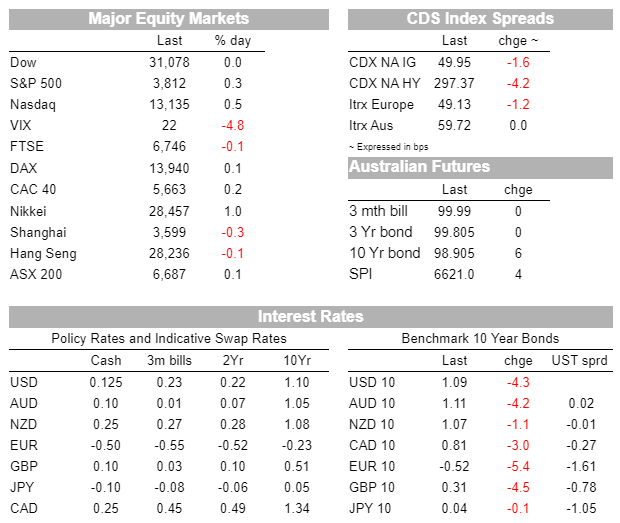

Bonds rallied in response with 10yr yields falling 4.1bps to 1.09%.

Equities were choppy, but supported by the tech sector, while FX moves were largely subdued.

Impeachment proceedings have had little impact on markets, as we await Biden’s detailed economic plan which is scheduled to be released today.

Pushback on taper talk continued overnight with the Fed’s Brainard going one step further and tying such a taper to the realised progress on inflation and maximum employment goals.

Yields fell in response to the speech with US 10yr yields reaching a low of 1.07% before paring declines.

Since yesterday

10yr yields have fallen 4.1bps to 1.09%. Brainard stated: “ Given my baseline outlook, I expect that the current pace of purchases will remain appropriate for quite some time”.

Brainard also re-iterated that the Fed’s asset purchase goals extends beyond market functioning to realised progress on inflation and maximum employment (“

The forward guidance adopted in December expands the goals of the asset purchases beyond market functioning by establishing qualitative outcome-based criteria tied to realized progress on our employment and inflation goals…. guidance clarifies that the pandemic asset purchases will continue at least at the current pace until substantial further progress is made on our employment and inflation goals. In assessing substantial further progress, I will be looking for sustained improvements in realized and expected inflation and will examine a range of indicators to assess shortfalls from maximum employment”). (see

Brainard speech for details).

An as expected US CPI print also tempered inflation talk somewhat

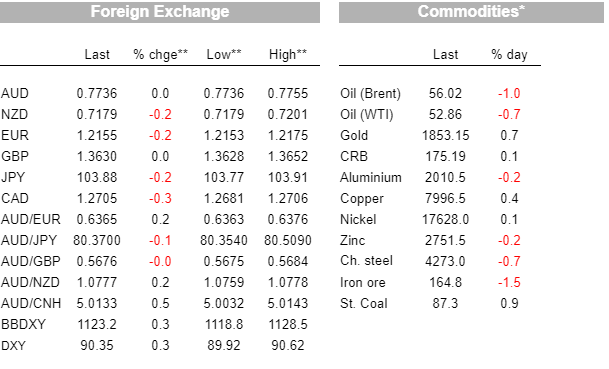

Though only had a small impact on US 10yr implied inflation breakevens which fell 1.5bps to 2.06%.

US Headline CPI for December rose 0.4% m/m with almost 60% of the rise driven by higher gasoline prices which rose 8.4% m/m. The more important Core measure was more muted at 0.1% m/m and 1.6% y/y.

Overall core inflation remains subdued, though base effects will clearly see the y/y rate lift up due to the large price falls early in the pandemic.

The Fed of course will look through such base effects (Brainard noted that the y/y for March and April may rise above 2% due to low March and April price readings from last year) and accordingly the three month and six month annualised rates will be more important to watch in the near future when assessing the true pace of inflation in the US (and elsewhere).

Equities rose with the S&P500 +0.3% with tech again helping to drive with the IT sub-index up 0.8%. Tech sentiment was initially driven by news that Intel’s CEO was stepping down (Intel +7.6%), with other tech names also caught in the slipstream.

Key for the outlook for stocks will be how quickly the economy rebounds (tied to vaccine rollout and fiscal stimulus hopes), the chances of tax/regulation changes under a Biden Administration, and on whether inflation starts to lift and whether yields lift significantly in response.

FX moves were largely muted with mild USD strength with the USD DXY +0.2%.

The Swedish Krona underperformed with USD/SEK +1.3% in the wake of the Riksbank’s flagging that it is selling SEK 5bn a month to acquire foreign exchange reserves between February 2021 and December 2023. The announcement is not related to monetary policy, but replaces the way Sweden currently finances its foreign exchange reserves which is principally done through loans in foreign currency via the Swedish National Debt Office (see Riksbank for details). In contrast, the AUD outperformed overnight, unchanged at 0.7737 with little in the way of news to drive.

US impeachment proceedings do not appear to be having an overwhelming impact on markets with a small rally in Yen during APAC yesterday largely reversing overnight (USD/Yen -0.2% to 103.87) and being similar to the moves seen in EUR (EUR -0.2% to 1.2155).

Senate Majority Leader Mitch McConnel has rejected calls to convene an emergency session in the Senate to start impeachment trial proceedings against President Trump, meaning a Senate trial will likely have to wait until after inauguration.

Other data out was largely muted with EZ Industrial Production for November beating expectations (+2.5% m/m v. 0.2% expected), but pre-dating the recent escalation in virus restrictions.

ECB President Lagarde also spoke overnight, emphasising that March will be a key date for the ECB (“What would be a concern would be that after the end of March, those member states still need to have lockdown measures and if, for instance, vaccination programs were slowed down ”). The obvious point being that the longer the necessary lockdowns continue, the greater the impact on Eurozone economies. President Lagarde also warned against the early tightening of policy.

Finally

In Australia yesterday job vacancies rose a sharp 23.4% q/q in Q4 with the level of vacancies now 11.9% higher than pre-pandemic levels.

With Australia’s participation rate at its equal highest on record and with vacancy levels above pre-COVID levels the risk is that unemployment falls more sharply than currently forecast by the RBA and Treasury.

This would be good news for the economy and would suggest the budget deficit could improve more quickly than expected.

The next round of RBA forecasts will be contained in the RBA’s February SoMP, released on February 5. The market is also beginning to discuss when the RBA might need to give further guidance on whether to extend or taper its $100bn QE program which ends at the end of April, along with the 3yr YCC target given the RBA has tied the 3-year target to the RBA’s view on how long it is expecting to keep rates steady for.

A more rapid decline in the unemployment rate, which would be very welcome, would likely have significant implications for the future settings of these unconventional policy measures and in turn for market pricing.

An actual lift in the cash rate though is still tied to the unemployment rate returning to full employment levels and inflation sustainably returning to the 2-3% target range, where Governor Lowe has said previously unemployment may need to fall to “four point something to get the type of wage pressures that will deliver inflation outcomes consistent with” the inflation target

Coming up today

A mostly quiet day domestically with only an ABS paper on the CPI (Q4 CPI is not out until January 27th).

Offshore it is busy with China’s Trade Balance, the ECB Minutes and US Jobless Claims and Fed Speakers.

US President-elect Biden is also scheduled to release details of his economic plan, with all focus on the likely quantum of near-term stimulus and on any proposed tax and regulatory changes. Details below:

- NZ: Building Permits – Nov: unlikely to be market moving and no consensus is available.

- JN: Core Machine Orders – Nov: unlikely to be market moving with consensus at -6.5% m/m.

- CH: Trade Balance – Dec: consensus sees the trade balance at $72bn, down slightly from last month’s $75.4bn.

- EZ: ECB Minutes – Dec: the minutes for the December meeting are out.

- US: Jobless Claims: initial claims are expected to remain high at 786k, little changed from last week’s 787k

- US: Fed’s speakers: Chair Powell is talking on a webinar with other speakers also scheduled including, Rosengren, Bostic and Kaplan

- US: President-elect Biden: Biden is expected to release details of his economic plan. Key focal points for markets will be on the magnitude of a proposed fiscal package, how that is likely to be funded – does it include a reversal in Trump’s tax cuts?, and any proposed regulatory changes particularly around climate and the technology sector.