Long-term signal vs. Short-term noise

Insight

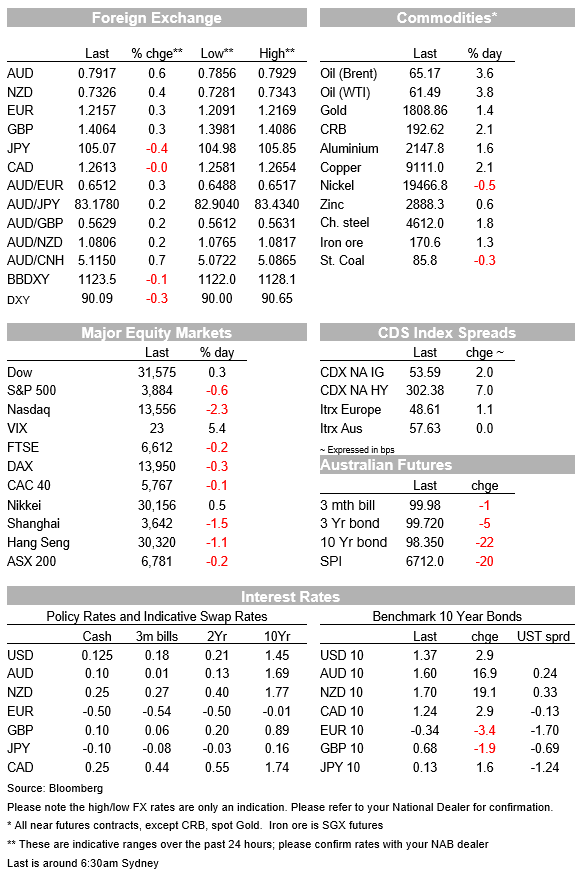

Australian 10 year bond yields have nudged 1.65 percent for the first time since May 2019.

https://soundcloud.com/user-291029717/bond-yields-go-crazy-aussie-dollar-hits-another-multi-year-high?in=user-291029717/sets/the-morning-call

Somehow you have to give in, you know

That’s how we see it, surrender

We’re out of control (Out of control) – Chemical Brothers

Tech share are under pressure as the rotation trade remains alive and kicking. The NASDAQ is down more than 2% while the Russel 2000 is up 0.3%. EU bond yields close lower after ECB Lagarde says the central bank is closely monitoring the move up in yields.10y UST yields are rising again after trading to an overnight low of 1.3245% while the implied yield in AU 10y futures is up another 4bps to 1.64%. USD is broadly weaker with AUD, NZD and GBP leading the charge, recording new highs in the process. Oil leads gains in commodities with Gold joining the party.

US equities are trading cautiously, with the S&P500 opening lower and staying in negative territory, currently down 0.56%. Further sector rotation is evident, with both the Dow Jones and Russell 2000 index showing modest gains, while underperformance of the tech sector sees the Nasdaq index currently down 2.17%.

Meanwhile the bond sell-off enjoyed a small reprieve overnight after ECB President Christine Lagarde said the Bank was “closely monitoring the evolution of longer-term nominal bond yields”. A strong signal suggesting the Bank is becoming uncomfortable with the current bond sell-off and it is prepared to intervene. Lagarde’s comments helped core European bond yields closed lower overnight with 10y Bunds ending the day at 0.341%, following an overnight high of -0.28%.

After trading to a high of 1.3925% during our afternoon session, Lagarde’s comments saw 10y UST yields trade to an overnight low of 1.3245%, but in the past few hours the benchmark yield is on the rise again and is currently trading at 1.3670%.

Yesterday, the AU bond market stole the show with a sharp sell-off across the curve. The ACGB April 2024 bond, the RBA YCC target, had been slowly creeping up from 0.102% on February 9 and closed last week at 0.1225%. The expectation was for the RBA to step in this week, buy the bond with some gusto and push the yield back down to its 0.1% target. In the end, the RBA announced it would buy $1bn of the bond, a half-hearted effort bearing in mind that in its last foray in December it bought $2bn. The market was not impressed, triggering a big sell that now sees the April 2024 with a yield of 0.2150%. The 10y part of the curve also came under pressure, the 10y yield closed at 1.602% ( up 17bps) and overnight the sell-off in AU bond futures has continued, with the futures trading at 98.35, implying a yield of 1.65%.

Central Banks certainly have the ammunition to fight the move up yields, technically all they need to do is print more money, but their resolve is clearly been tested as investor position for a rise in inflation fuelled by vaccination programs around the globe and speculation over a new commodity cycle.

On the latter, price action overnight has done nothing to dissuade the notion that the global economic recovery will be a boom for commodities . Oil prices have led the gains up ~3%, Brent oil climbed above $64 a barrel as Goldman Sachs analysts predicted prices could advance into the $70s in coming months. Copper rose above $9,000 a metric ton for the first time in nine years (1.64%), and even gold join the party recording its best daily gain in 35 trading days, up 1.7% to $1806.

The NZD and AUD head the leader board, although the theme for the day has been broad USD weakness, so crosses are barely higher. The AUD blasted up through 0.79 a few hours ago and is currently trading near 0.7920 with the commodity backdrop suggesting a move above 80c looks imminent, although given the AUD is a risk sensitive currency equity’s tolerance for higher yields is a risk to watch. The NZD reached its highest level in nearly three years, touching 0.7338 mid-afternoon yesterday and now trades at 0.7325.

UK PM Johnson outlined what looked like a fairly cautious roadmap for reopening the economy, beginning with schools on 8 March, limited outdoor gatherings from 29 March, non-essential shops, outdoor attractions and indoor gyms and pools from 12 April, indoor hospitality from 17 May and a final lifting of all restrictions from 21 June. In between lifting the restrictions a series of tests would need to be met before progressing with further easing.

GBP took the news in its stride, showing no sign of disappointment, the pair currently trades at 1.4066, close to it overnight high. Euro and JPY are also stronger against the USD, now trading at 1.2158 and 105.66 respectively.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.