Online retail sales growth slowed in May following a fairly strong April

Insight

Bond yields were already on the rise before Fed chairman Jerome Powell talked down the likelihood of any easing in bond purchases this year.

https://soundcloud.com/user-291029717/bond-yields-rise-further-as-powell-puts-paid-to-tapering?in=user-291029717/sets/the-morning-call

I’m just lookin’ for a dear, dear friend of mine

I’m waiting for my man – The Velvet Underground

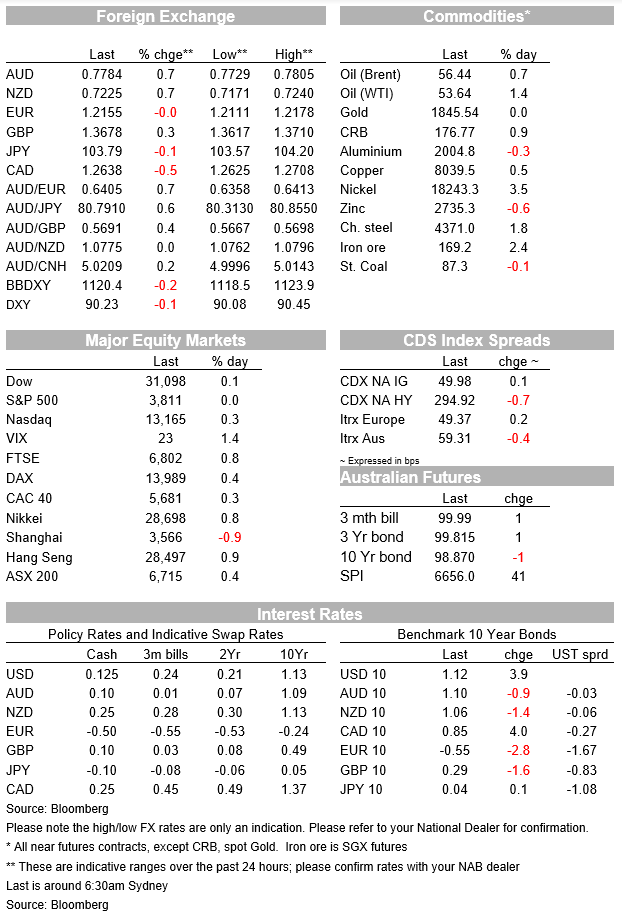

US equities have traded in and out positive territory as investors await Joe Biden’s fiscal stimulus speech. Expectations of a big spending plan in the region of $2trn is buoying risk sentiment notwithstanding underwhelming US economic data (Jobless Claims print biggest rise since March). Fed Chair Powell is more worried about the labour market than inflation and emphasises that now is not the time to talk about exit strategy. UST 10y little changed, USD broadly weaker. AUD briefly trades above 78c.

European equities closed in positive territory with the Stoxx Europe 600 Index climbing 0.7%. Italian shares where the exception, down 0.47% amid concerns over PM Conte’s coalition stability following former PM Renzi’s party withdrawal from the coalition, leaving Conte without a majority in parliament. Conte may seek a confidence vote in parliament next week.

Meanwhile on the other side of the Atlantic, after trading in and out of positive territory, main US equity indices are currently showing small losses for the day (S&P 500 -0.22%, NASDAQ -0.22%). Expectations over a big spending plan from President elect Biden is helping sentiment notwithstanding underwhelming US labour market data. Initial jobless claims rose by 181k to 965k in the week ending January 9 (on an unadjusted basis, the figure jumped to 1.15m). The move up in claims surprised market economists with the consensus looking for an unchanged print. The third COVID wave is doing some damage to the labour market and this new uptick in claims needs to be watch as it could signal the beginning of a new uptrend.

Biden’s speech on his spending plans is scheduled to start at 1915 ET from Wilmington, Delaware (that’s 11:15 Sydney time). It is unclear how much detail we will get, but media reports over the past 24 hours have been highlighting the potential for a ~$2trn pandemic fighting spending plan . Aligned to Biden’s idea of dealing with COVID first the key elements of the pandemic relief plan ($2k direct payments to US citizens, supplementary and extended unemployment insurance benefits, cash for state and local govts, funding for vaccine distribution and tax credits for families with children) will initially be attempted to be pushed through in a bipartisan way – with Congressional support.

Key to the above is a) how much of the “trillions” Biden plans to spend will be rolled out imminently, for instance, expectations are for an increase in direct payments to most Americans to $2,000 from the $600 enacted in December and how much will come over time, for instance infrastructure spending which could be over many years…and b) how this spending will be funded. Simply by borrowing more or partly funded by a reversal of Trump’s corporate tax plus an increase in income tax for the wealthy (latter options not seen as market friendly). The funding dynamic will be important, because if a change in tax is involved, that will take a fair bit of time to get it approved by Congress.

10y UST yields are now trading at 1.12% about 1bps higher to where they were when Sydney called it a day yesterday. Fed Chair Powell participated in a Q&A session a couple of hours ago, downplaying concerns over inflation and emphasising that the fed is more concerns over the outlook for the labour market. “We are a long way from maximum employment,” and indication that the Fed’s current ultra-easy policy setting will remain in place for the foreseeable future.

The Fed Chair noted that Inflation dynamics don’t change “on a dime,” adding that there’s a lot of slack in the labour market that’s going to depress inflation, thus the biggest concern is that inflation stays too low. The Fed Chair notes that many economists are anticipating an acceleration in inflation in coming months, with base-effects coming from higher oil prices a key dynamic, but he dismissed these concerns arguing that the Fed needs to focus on sustained inflation rather than a one-off hits. On this score, Powell reiterates that Core PCE, is the Fed’s preferred inflation metric.

Powell also emphasised that under the Fed’s new framework for interest rate policy, launched last year, the central bank won’t raise interest rates to prevent unemployment from falling unless it sees a serious risk of excessive inflation. Finally in terms of QE tapering, Powell insisted that before any discussion takes place, there would need to be “clear evidence” about making “substantial further progress” toward the Fed’s goals adding that tapering will be signal well in advance.

Moving onto currencies the USD is trading a little softer with DXY and BBDXY indices down around 0.15 The AUD has edged a little bit higher and now trades at 0.7783, after briefly trading above 78c.NZD has also done well, up 0.65 and now trading at 0.7226.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.