Online retail sales growth slowed in May following a fairly strong April

Insight

Bond yields have paved down across the world, driven by a sell-off in German bunds.

https://soundcloud.com/user-291029717/bonds-sold-off-boris-no-deal-stymied?in=user-291029717/sets/the-morning-call

The Peter Lee surveys are now taking place. If you have appreciated NAB’s Market Research support please let your company’s representative know.

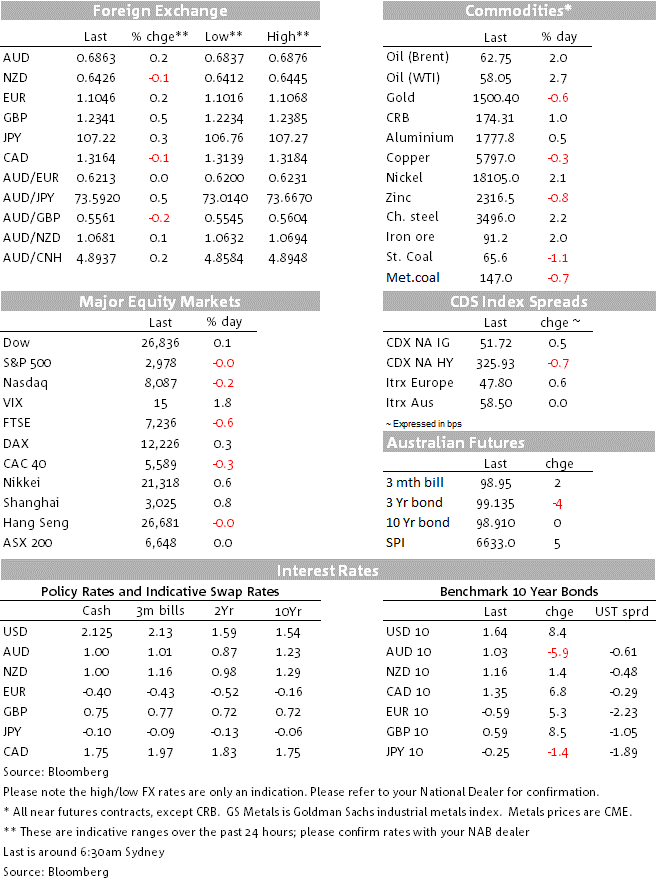

It was a quiet night overnight as markets position ahead of the ECB meeting on Thursday. Yields are meaningfully higher, led by German Bunds with German 10yr yields +5.3bps to -0.590%. Moves in Bunds largely shadowed and extended by US Treasuries with US 10yr yields +8.4bps to 1.6352%. Headlines also added at the margin with another story of possible German fiscal stimulus to be financed off-balance sheet, US Treasury Secretary Mnuchin making some positive comments on trade, while Trump is reported to have private concerns over the economy.

In FX the USD (DXY) continued its downward move seen last week, -0.1% to 98.326. The biggest G10 mover was NOK on the back of a better than expected GDP report and a higher oil price, with USD/NOK -0.6% to 8.942. GBP also continues to rally, +0.5% to 1.2344 as markets price out the risk of a no-deal Brexit and as monthly GDP figures beat expectations. Moves in other pairs were more contained with EUR +0.2% to 1.1046 and USD/JPY +0.3% to 107.24 and AUD +0.2% to 0.6863. Equities were little changed with the S&P500 -0.0% to 2,978. In the words of Elton John and Tim Rice’s famous Lion King hit, given the absence of data and volatility it was largely a case of Hakuna Matata for markets overnight.

First to the move in yields. There was no single driver for the move in yields, but it does seem like it was initially driven by positioning ahead of the ECB meeting on Thursday with investors nervous given the divisions within the ECB. The consensus looks for the ECB to cut to the Deposit Rate by 10bps to -0.5%, tiering of the deposit rate and resuming QE at €30bn a month. Given those high expectations of easing, we have been pointing out for some time the risk that the ECB underwhelms markets with officials divided on the need for resuming QE. Also adding to moves were two articles on the possibility of German fiscal stimulus ahead of Finance Minister Scholz’s presentation of spending plans to parliament today. A Reuters article quoted three officials stating the government was flirting with the idea of off-balance sheet financing via setting up independent public entities to fund investment in infrastructure and climate protection (see Reuters for details). This headline also initially drove the EUR up to 1.1059 before reversing. A subsequent Bloomberg article also noted the Germany’s Finance Deputy who said that plans to run balanced budgets through to 2023 could be reviewed if economic conditions changed. German 10yr Bund yields closed +5.3bps to -0.59%.

UK Gilt yields also move sharply, +8.5bps to 0.585% as investors further price out the risks of a hard-Brexit and as UK economic data beat expectations. Monthly GDP for July beat expectations at +0.3% m/m against 0.1% expected and reducing fears of a pre-Brexit recession after the economy contracted slightly in Q2. The more positive vibe was also supported by beats in Industrial Production (+0.1% m/m against -0.3% expected) and the Trade Balance (-219m against -1.5bn, albeit the sharp decline was driven by lower imports of erratic items such as gold). Risk of a no-deal hard Brexit have also receded with the bill delaying Brexit until 31 January 2020 (unless a deal is approved by MPs by 19 October) becoming law today after it was given royal assent. Parliament is also now expected to be prorogued today until 14 October – meaning MPs will not get another chance to vote for an early election until after this date. Temporarily weighing on GBP was speaker Bercow’s announcement that he will step down at the next election, or on 31 October – though given the speaker is elected by Parliament in another hung Parliament it is likely a candidate similar to Bercow who has allowed Parliament to have their say on Brexit will continue.

US Treasuries extended moves, with US 10yr yields +8.4bps to 1.6438%. There was little in the way of data to drive moves. On trade, Treasury Secretary Mnuchin said the US and China have a “conceptual” agreement on enforcement concerns on trade and that he takes it “as a sign of good faith that they want to continue to negotiate, and we’re prepared to negotiate”. Despite those tones, markets do not expect a near-term deal. Chinese press in contrast suggest that while China has agreed to 80% of demands for a trade deal, the final portion of the US’ demands are an infringement on Chinese sovereignty – the final 20% includes demands to abandon the Made in China 2025 strategy as well as reducing the role of the state in the overall economy. Accordingly Chinese press suggests for a deal to be made, the US will have to give up on its demands as well as reversing recent tariffs.

In FX moves, NOK was the biggest G10 mover with USD/NOK -0.6% to 8.942 with monthly GDP at +1.0% m/m against 0.3% expected. A higher oil price also supported with WTI oil +2.7% to $58.05. Oil was supported on news that Saudi Arabia’s new energy minister has signalled that OPEC and its allied would continue with output cuts. Note OPEC meets on Thursday.

The NZD bucked the trend of USD weakness with NZD -0.1% to 0.6426. Worse than expected manufacturing data weighed with Manufacturing Sales volumes down 2.7% q/q where a flat result was largely expected. My BNZ colleagues note that while production may not be as negative, it will still likely be drag on Q2 GDP (out on 19 September) and have lowered their expectation to 0.3% q/q from 0.4% q/q, and suggests some downside risks to the RBNZ’s 0.5% expectation.

Finally in Australia, Housing Finance figures for July beat expectations with owner-occupier loans +4.7% m/m and investor loans +5.3% m/m. The data overall suggests that recent rate cuts and the relaxation of mortgage serviceability requirements are boosting activity in the housing market. This is a positive for consumers given housing is their biggest asset, although we do not expect this to translate into construction given building approvals have shown fresh weakness and developers/builders are still facing tight financing conditions.

Domestic focus will be on the NAB Business Survey and then to the Chinese CPI/PPI. It is relatively quiet otherwise with little data of note out of the US.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.