Online retail sales growth slowed in May following a fairly strong April

Insight

Markets reversed a little overnight with US and European equities rising.

https://soundcloud.com/user-291029717/a-brief-respite-on-hopes-of-us-stimulus-deal?in=user-291029717/sets/the-morning-call

I feel so close to you right now, it’s a force field. I wear my heart upon my sleeve, like a big deal.

Your love pours down on me surround me like a waterfall. And there’s no stopping us right now, I feel so close to you right now – Calvin Harris

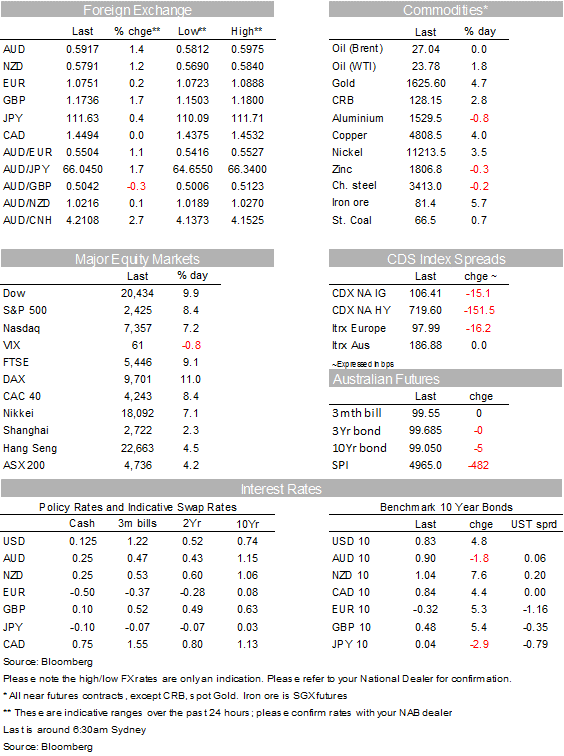

Risk assets are enjoying a nice rebound as the market digest the Fed’s broadening QE move into the corporate space while the prospect of a big US fiscal stimulus edges closer to fruition. COVID-19 cases continue to rise, but encouragingly the rate of spread across Europe is slowing. These combination of news have helped European and US equities record decent gains while the ease in financial stress sees the USD weaker across the board. AUD and NZD have retained most of yesterday’s gains.

After a fair bit of wrangling over the past few days reports over the past few hours suggest that negotiations over a huge US virus relief bill estimated to be close to $2trn are now edging towards a positive conclusion. According to officials sticky issues surrounding $500bn in industry assistance loans and expanded unemployment insurance had largely been resolved while Democrats demands for an increase in oversight on how big business use the coronavirus rescue funds have also been considered. US Treasury Secretary Steven Mnuchin, who has led the negotiations for Republicans said he expects a bipartisan deal to be reached before the end of Tuesday US time.

News on the virus front have also been encouraging, the number of COVID-19 cases has breached 400,000 but the rate of spread across Europe is slowing, following the pattern of China and Korea after their successful containment measures. Although more of the same news are needed, these are encouraging signs and suggest Europe’s containment measures are having a positive containment impact. On the other side of the Atlantic, the US has been slow with its containment measures and the number of new cases continues to accelerate. New York City is a hot spot, with the number of cases per million people now well above what we saw in Hubei Province, China’s epicentre. A decline in the rate of increase of infection in the largest world economy would be the ultimate circuit breaker to the current rout in risk assets, right now however there is a lot uncertainty on whether the current US containment measures are going to be enough to contain the virus in the US.

For now risk assets are focused on the good stimulus news coming from both the fiscal and monetary side. European equities closed with decent gains of around 8% to 10% with the DAX index outperforming closing at 10.98%. US equities are also enjoying a nice rebound with the Dow up 11.37% as I type while the S&P500 is 9.38% and the NASDAQ is 8.12%.Of note gains in equities has been broad based with many of the beaten up stocks and sectors outperforming. It is the third Tuesday in a row where stocks have rebounded strongly and the test will be whether a second consecutive rise in the market can occur tomorrow.

The improvement in risk appetite has also seen a move up in core global bond yields with shorter dated UST yields leading the move. The 2y UST Note is up 6bps to 0.375%, after trading to an overnight high of 0.405%. The US 10-year Treasury yield has traded as high as 0.89% overnight and is currently 0.83%, up 2bps for the day. Meanwhile in Europe 10y Bunds and Gilts rose 5bps to -0.322% and 0.479% respectively.

Credit markets are also in better shape, with US CDX and cash bond spreads for both high grade and high yield showing some narrowing. Corporates have been encouraged enough to tap markets, with Europe seeing its busiest day for issuance in six weeks, and US issuers lined up to take advantage of better sentiment in credit markets.

The big news is that the improvement in risk appetite alongside the ease in financial stress, evident in the credit market and courtesy of the Fed QE expansion into the corporate space have combined to arrest the upward momentum seen on the USD over the past 10 days. The BBDXY index looks set to end ist 10 day winning streak, the index is currently down 0.61% while DXY is -0.40%. The USD is not only broadly weaker against majors, it has also underperformed against EM with the EMCI index up 0.56% with ZAR leading EM FX, up 1.77%.

Yesterday the AUD was on a steady rise as the market embraced the Fed Corporate QE news with the pair trading to an intraday high of 0.5975, Overnight the AUD was range bound and it has managed to retain most of yesterday’s gains, the pair now trades at 0.5945. In a similar vein, the NZD traded to a high of 0.5840 late yesterday and now trades at 0.5835.

Key economic indicators released are starting to show the impact of the widespread lockdowns, but they have not elicited a big reaction by markets. The flash Markit PMIs that were released across the G7 showed a familiar pattern, with unprecedented falls in service sector activity – reflecting less tourism, retailing and spending at restaurants – and milder falls for manufacturing. The final March figures, which will incorporate more recent data, are likely to be even worse, while April figures will be worse again for most regions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.