We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

There seems to be hope of an early recovery to the impacts of the coronavirus.

https://soundcloud.com/user-291029717/caution-as-china-gets-back-to-work?in=user-291029717/sets/the-morning-call

I’m just lookin’ for a dear, dear friend of mine, I’m waiting for my man – The Velvet Underground & Nico

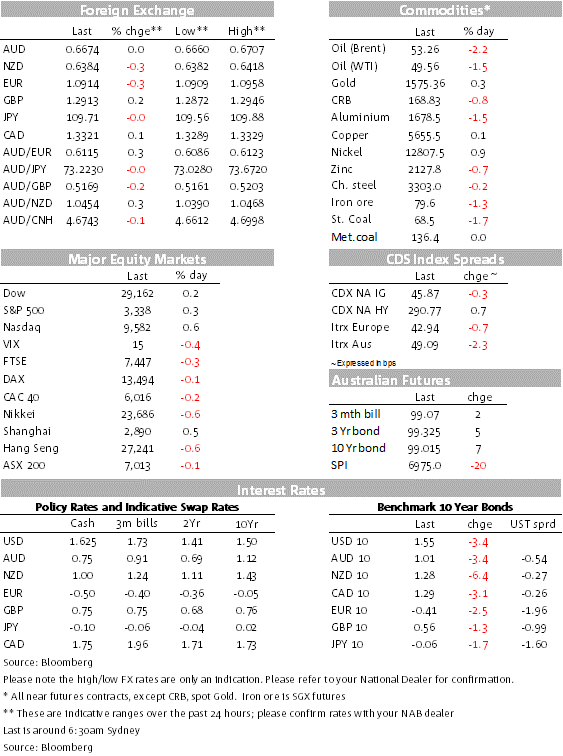

Markets are still trying to work out the impact from the Novel Coronavirus (NCoV) on the global economy, but there is a fair divergence depending on which market one looks at. US equity markets have started the week on a positive note with all major indices showing gains as we type. A higher degree of cautiousness was evident in Europe with major regional indices down on the day. Apart from virus uncertainty, disappointing data and German political instability have also played in the old continent. Core global yields are lower reflecting wariness in the air, oil prices are down again while the USD is little changed with NZD and EUR the underperformers.

Main US equity indices are up between 0.4%-0.8% as we type with US investors focusing on the resilience on the US economy aided by a solid labour market and lose financial conditions courtesy of a low Fed Funds rate and ample liquidity in money markets. The US economy is less internationally exposed and thus less likely to be affected by the NCoV outbreak with its epicentre in China.

The number of worldwide confirmed cases of the coronavirus outbreak is now over 40,500, with 99% of those cases in mainland China. The number of deaths has breached 900, with still only two of those outside of mainland China. That said, the virus is spreading, with the number of countries affected increasing. Singapore is the worst-affected country outside of China with 45 confirmed cases. The head of the World Health Organisation said that “In recent days we have seen some concerning instances of onward [coronavirus] transmission from people with no travel history to China, like the cases reported in France yesterday and the UK today. The detection of this small number of cases could be the spark that becomes a bigger fire. But for now, it’s only a spark.”

The PBoC provided additional supports to its local market by injecting 700b yuan into the banking system using 7-day reverse repurchase agreements. This support appears to be behind the performance of China’s equity markets, which notably where the only ones to record positive gains in the APAC region.

The bond market seems more concerned about the economic impact of the coronavirus, with rates biased to the downside, on the view that monetary authorities are likely to be more accommodative in their policy stances than otherwise. The US 10-year Treasury rate is down 4bps to 1.55% while 10y Bunds closed 2.5bps lower at -0.41%, trading near its low for the session. Technicians will be looking at last week’s 10y UST’s low of 1.50% as an indicator of yield support.

Moves in FX have been a little bit more subdued. The USD is little changed in index terms (DXY @ 98.40) and within G10, GBP has edged a little bit higher ( +0.20% 1.2954) while the euro and NZD have underperformed. After a pretty bad week, GBP looks to be stabilising with focus now shifting to fiscal policy as the UK Government goes into recess at the end of this week (from 13-24 Feb). The government is set to announce HS2 (the contentious high speed rail project) and other infrastructure projects and an expected Cabinet reshuffle. There’s also an expected freeports announcement today, under which there would be up to 10 free-trade zones where imported goods can be processed free of customs duties before being exported again.

Part of euro’s underperformce is probably explained by renewed German political uncertainty. Annegret Kramp-Karrenbauer (AKK), Chancellor Merkel’s designated successor, announced her plans to step down as CDU leader and she won’t be running for the German chancellorship at the next federal election. AKK’s decision comes after a CDU delegates in eastern Germany disobeyed the party’s ban on cooperating with the far right AfD party. EUR got through that news largely unscathed but lurched down several hours later for no obvious reason, reaching a low of around 1.0910. The pair now trades at 1.0913.

The AUD is flat at 0.6680, after early yesterday morning reaching a fresh post GFC low of 0.6660. Stability in CNY has probably been one factor helping the AUD. Firmer CNY with PBoC evidently intent in resisting any sustained move in USD/CNY back above 7.00 helped the slight improvement in the risk tone during our APAC session.

NZD meanwhile didn’t benefit as much from the CNY stability. NZD remains on the soft side – trading near a fresh low for the year just above 0.6380 – with the impact of the coronavirus forefront of mind and NZ’s high economic exposure to China.

The longer the economic shutdown in China extends, the greater the impact on AU and NZ’s export earnings. While near-term pressure remains to the downside, once we get harder evidence of the virus being well under control, then the scene will be set for an AUD and NZD recovery.

NCoV news are likely to remain the focus for investors ahead of Fed Chair Powell appearance before the House Committee early tomorrow morning.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.